Last Update 08 Jun 26

Fair value Increased 42%RKLB: National Security Space Backlog Will Drive Future Earnings Power

Rocket Lab's analyst price target has shifted from $105.00 to about $149.03 as analysts point to industry launch under supply, an expanding backlog, infrastructure advantages, and a core business that is closer to profitability.

Analyst Commentary

Bullish analysts have been steadily lifting their fair value estimates for Rocket Lab, pointing to a mix of execution in the launch business, an expanding backlog, and progress toward a more profitable core operation.

Recent research has also framed Rocket Lab as a key player in the broader space economy, with some analysts highlighting its role as a scaled Western launch and space infrastructure platform alongside larger peers.

New coverage initiations and upgrades, combined with higher price targets, signal growing confidence in the company’s positioning and its ability to convert its pipeline into revenue and, over time, improved earnings quality.

Bullish Takeaways

- Bullish analysts see industry wide launch under supply as a supportive backdrop for Rocket Lab, with the company’s existing infrastructure viewed as a key asset in capturing mission demand and supporting backlog.

- Several firms have raised their Rocket Lab price targets, including moves to about US$129 and beyond. They tie these targets to expectations around execution on launches, a growing order book, and a core business that is described as closer to profitability.

- New coverage has framed Rocket Lab as the only scaled Western launch and space platform outside of SpaceX. Bullish analysts argue that current valuation reflects less than 1% participation in the space economy, which they see as leaving room for a re-rating if the company delivers on growth plans.

- Upgrades from neutral or more cautious stances to more constructive views, combined with higher targets from multiple research houses, reflect a cluster of positive sentiment that centers on operational progress and the potential for better long term growth and margin performance.

What’s in the News

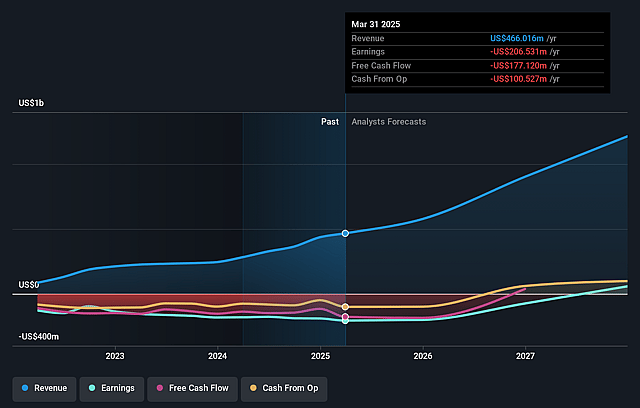

- Rocket Lab reported record Q1 2026 revenue of US$200.3 million, with a backlog above US$2.2 billion. Results were driven by 31 Electron/HASTE launches and five Neutron agreements, and the company highlighted higher gross margins, improving adjusted EBITDA, and contributions from recent acquisitions such as Mynaric AG and the planned Motiv Space Systems deal (source: Q1 2026 earnings reports).

- The company announced an at-the-market equity offering program of up to US$3 billion, giving it flexibility to issue common stock over time to fund projects such as Neutron, potential acquisitions, and general corporate purposes. This program has raised investor questions about dilution (source: equity offering filings).

- Rocket Lab secured more than US$1.3 billion in contracts tied to the Space Development Agency’s Tracking Layer Tranche 3 constellation and related programs. These include a US$816 million award, a US$90 million U.S. Space Force satellite contract, and a US$190 million hypersonic test flights deal, reinforcing its position in U.S. defense and national security space projects (source: SDA and contract announcements).

- The company signed a definitive agreement to acquire Motiv Space Systems for up to US$60 million in cash and stock, adding Mars rover heritage robotics, 50 engineers, and in-house production of mechanisms such as solar array drive assemblies to its space systems capabilities (source: Motiv acquisition announcement).

- Rocket Lab won a US$90 million multi-year U.S. Space Force contract to design, build, and operate two geostationary satellites using its Lightning bus and Heimdall optical payload. This marks its first satellite production program in geostationary orbit and extends its vertically integrated model into higher orbits (source: U.S. Space Force contract announcement).

Valuation Changes

- Fair Value: The analyst fair value estimate has risen meaningfully from $105.00 to about $149.03.

- Discount Rate: The discount rate has moved slightly higher from 7.58% to about 7.92%.

- Revenue Growth: The revenue growth assumption has been reduced from about 54.93% to about 38.81%.

- Net Profit Margin: The net profit margin assumption has increased from about 14.37% to about 19.72%.

- Future P/E: The future P/E multiple has risen from about 282.5x to about 370.0x.

Key Takeaways

- Rocket Lab's vertical integration and unique end-to-end offerings position it to secure premium pricing, superior margins, and major defense and constellation contracts ahead of peers.

- The company is set to capture significant market share with reusable launches and international expansion, transforming backlogs into stable, high-margin recurring revenue streams.

- High cash burn, regulatory risk, government contract dependence, competitive pressures, and execution risks threaten Rocket Lab's path to profitability and sustainable revenue growth.

Catalysts

About Rocket Lab- A space company, provides launch services and space systems solutions in the United States, Canada, Japan, and internationally.

- Analyst consensus sees Neutron as a medium-class rocket capitalizing on constellation launches, but this fundamentally understates the scale of pent-up demand for Falcon 9 alternatives-in reality, Neutron is positioned to capture an outsized market share as the only operational US-based reusable competitor, potentially driving a rapid, nonlinear acceleration in backlog and revenue as soon as it achieves orbit and demonstrating operating leverage much sooner than expected.

- Analysts broadly agree that vertical integration and expansion in Space Systems will lead to margin improvements; however, by fully controlling payloads, critical components, bus manufacturing, and launch, Rocket Lab is uniquely positioned as the only Western supplier able to deliver fixed-price, end-to-end solutions for defense and constellation customers-unlocking premium pricing, higher recurring revenues, and structurally superior gross and net margins ahead of industry peers.

- The looming multi-hundred-billion-dollar Golden Dome Defense Initiative and Mars communication programs represent generational secular mega-trends; Rocket Lab is currently the only agile, vertically integrated player with rapid execution capability and a real track record, making it a frontrunner for contract wins that could multiply revenue and secure extremely long-duration cash flows absent from analyst models.

- The company's international expansion, exemplified by direct ESA contracts and aggressive moves into the European national security sector, opens up new, underappreciated total addressable markets and revenue streams; combined with unique in-house technology from recent acquisitions, Rocket Lab is positioned to force-multiply both market share and contract value versus competitors tied to slower or less integrated supply chains.

- With reusable vehicle cadence, rapid infrastructure buildout, and automated composite manufacturing coming online, Rocket Lab stands to achieve launch rates-particularly for government, hypersonic, and constellation contracts-orders of magnitude higher than current expectations, turning what are perceived as "lumpy" backlogs into a pipeline of predictable, high-margin, and cash-generative business.

Rocket Lab Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on Rocket Lab compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Rocket Lab's revenue will grow by 38.8% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from -26.9% today to 19.7% in 3 years time.

- The bullish analysts expect earnings to reach $358.5 million (and earnings per share of $0.57) by about June 2029, up from -$182.6 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $14.3 million.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 370.5x on those 2029 earnings, up from -348.9x today. This future PE is greater than the current PE for the US Aerospace & Defense industry at 39.6x.

- The bullish analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.92%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Rocket Lab's continued high cash consumption and negative free cash flow, especially driven by Neutron development and scaling, make its path to sustainable profitability and positive cash generation uncertain, which could put pressure on future earnings and the company's ability to fund growth internally.

- Secular trends of rising regulation and scrutiny on space launches, such as the need for more environmental approvals and potential carbon emission limits, could increase Rocket Lab's compliance costs and delay missions, negatively impacting revenue growth and launch margins over the long term.

- The company remains highly dependent on large, lumpy government contracts for both its Space Systems and Launch Services segments, making its backlog and future revenues vulnerable to delays, non-renewals, or political budget changes that can lead to significant volatility in earnings.

- Intensifying competition in the commercial launch sector, with increasing entrants and established giants like SpaceX, may drive down launch prices, dampen revenue per launch, and compress net margins as Rocket Lab attempts to remain competitive, particularly if launch supply grows faster than demand.

- Delays or underperformance in scaling reusable Neutron production and reliable launches could result in missed market opportunities, slow contract awards, and greater R&D and capital expenditures than planned, directly threatening long-term revenue growth and margin expansion.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Rocket Lab is $149.03, which represents up to two standard deviations above the consensus price target of $105.28. This valuation is based on what can be assumed as the expectations of Rocket Lab's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $150.0, and the most bearish reporting a price target of just $60.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $1.8 billion, earnings will come to $358.5 million, and it would be trading on a PE ratio of 370.5x, assuming you use a discount rate of 7.9%.

- Given the current share price of $110.08, the analyst price target of $149.03 is 26.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Rocket Lab?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.