Last Update 03 May 26

Fair value Decreased 0.046%GAU: New Underground Resources And Mine Plan Will Support Future Outperformance

Analysts have adjusted their price target on Galiano Gold marginally to CA$6.44 from CA$6.44, reflecting small tweaks to assumptions around fair value, discount rate, and future P/E rather than any major change in the outlook.

What's in the News

- Galiano Gold has scheduled a special or extraordinary shareholders meeting for June 11, 2026, which may address corporate matters that investors will want to monitor closely (Key Developments).

- The company released updated Mineral Reserve and Mineral Resource estimates for the Asanko Gold Mine, effective December 31, 2025, including maiden underground Mineral Resources at the Nkran and Abore deposits, with detailed tonnage, grade, and contained gold figures across open pit and underground categories (Key Developments).

- New underground Mineral Resource estimates at Nkran and Abore total 3.4 Mt of Indicated Mineral Resources at 2.74 g/t for 0.30 Moz of contained gold and 6.5 Mt of Inferred Mineral Resources at 2.52 g/t for 0.53 Moz of contained gold, based on a gold price assumption of $2,400/oz and a 1.5 g/t cut off grade (Key Developments).

- Management outlined a multi stage business plan focused on organic growth at the Asanko Gold Mine, mine life extension across Abore, Nkran and Esaase, and potential accretive acquisitions, supported by continued capital investment in exploration and mine studies (Key Developments).

- For fiscal 2026, Galiano Gold issued production guidance for the Asanko Gold Mine of 140,000 to 160,000 ounces of gold, with 60,000 to 70,000 ounces expected in the first half and 80,000 to 90,000 ounces in the second half, reflecting higher mined grades from Abore later in the year (Key Developments).

Valuation Changes

- Fair Value: CA$6.44 has been revised fractionally to CA$6.44, reflecting only a very small numerical adjustment in the model output.

- Discount Rate: The discount rate assumption moved slightly from 7.76% to 7.77%, indicating a marginally higher required return in the valuation framework.

- Revenue Growth: The long term revenue growth input remains effectively unchanged at about 35.52% in both the prior and updated assumptions.

- Net Profit Margin: The projected net profit margin stays essentially flat at roughly 31.98% in the updated model.

- Future P/E: The assumed future P/E ratio is adjusted modestly from 5.99x to 6.03x, pointing to a slightly higher valuation multiple being used in the forecast period.

Key Takeaways

- Higher gold prices and ongoing process plant upgrades are expected to boost revenues, margins, and profitability amid increasing investor demand for gold.

- Significant exploration success and a strong cash position enable mine life extension, future production growth, and investment flexibility.

- Heavy dependence on a single asset, rising regulatory and operational costs, limited exploration growth, and ESG pressures threaten profitability and long-term sustainability.

Catalysts

About Galiano Gold- A mining, development, and exploration company.

- Increasing global instability and ongoing economic uncertainty are fueling investor flows into gold as a safe-haven and inflation-hedging asset. With Galiano highly leveraged to the gold price, sustained or higher gold prices will directly support higher realized revenues and strengthen operating cash flows.

- Successful step-out and deep drilling at Abore has intercepted significant widths and grades of mineralization below current reserves, confirming the deposit is open at depth and along strike. This creates significant reserve and resource expansion potential, supporting future production growth and longer-term revenue visibility.

- Commissioning of the secondary crusher and other process plant upgrades is expected to enable higher mill throughput (5.8 Mtpa design), making harder ore sources economic to process, reducing per-unit processing costs, and driving improved net margins and earnings as production increases.

- Sustained cost optimization and operational discipline, including a 10% reduction in all-in sustaining costs (AISC) and strong control over fixed costs, are setting the stage for improved operating margins and enhanced profitability as production ramps up.

- A strong, debt-free balance sheet with $115 million in cash enables accelerated investment in mine life extension and future growth projects, while maintaining optionality for shareholder returns or opportunistic acquisitions-laying the foundation for long-term free cash flow and EPS growth.

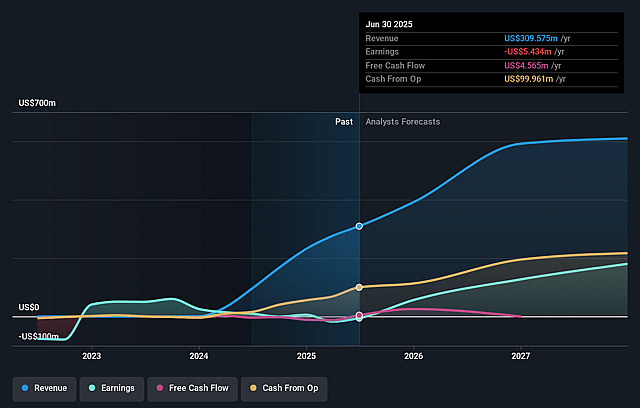

Galiano Gold Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Galiano Gold's revenue will grow by 35.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from -8.9% today to 32.0% in 3 years time.

- Analysts expect earnings to reach $261.4 million (and earnings per share of $1.01) by about May 2029, up from -$29.3 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 6.0x on those 2029 earnings, up from -20.6x today. This future PE is lower than the current PE for the US Metals and Mining industry at 16.4x.

- Analysts expect the number of shares outstanding to grow by 0.87% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.77%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Galiano Gold's continued reliance on a single asset-the Asanko Gold Mine in Ghana-means that any operational, geological, or regulatory disruptions at this site could directly and substantially impact future revenues and net margins, especially as current mine life and resource expansion are still being defined.

- Increasing government royalties and levies in Ghana, including a new 2% growth and sustainability levy applied from April, are driving up all-in sustaining costs (AISC) by an estimated $100/oz at current gold prices and could erode net earnings and reduce shareholder returns if regulatory costs continue to rise.

- Sustained local currency (cedi) appreciation against the U.S. dollar, as noted in Q2, may add additional upward pressure to cost structures, potentially reducing operating margins and free cash flow despite predominantly U.S. dollar-based expenses.

- The company's still-limited organic exploration pipeline, with near-term growth almost exclusively focused on Abore, raises concerns about long-term production growth and reserve replacement, which could threaten future top-line revenues if new discoveries or reserve expansions do not materialize as expected.

- Ongoing global investor focus on ESG and the potential for heightened scrutiny of gold mining operations may increase Galiano Gold's cost of capital or limit access to funding if the company cannot demonstrate continued progress on sustainability and environmental best practices, ultimately impacting future investment and growth opportunities.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of CA$6.44 for Galiano Gold based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$9.01, and the most bearish reporting a price target of just CA$3.9.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $817.5 million, earnings will come to $261.4 million, and it would be trading on a PE ratio of 6.0x, assuming you use a discount rate of 7.8%.

- Given the current share price of CA$3.15, the analyst price target of CA$6.44 is 51.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Galiano Gold?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.