Key Takeaways

- Rising ESG trends, decarbonization, and diminishing gold demand threaten Galiano Gold's access to capital, revenue growth, and long-term profitability.

- Operational risks from declining ore grades, Ghana's political landscape, and increasing costs may squeeze margins and challenge future project viability.

- Strong operational improvements, exploration success, financial strength, and a stable jurisdiction underpin resource growth and margin expansion, supporting positive long-term prospects and valuation.

Catalysts

About Galiano Gold- A mining, development, and exploration company.

- Growing momentum behind divestment from extractive industries and a global acceleration of ESG investing could significantly reduce Galiano Gold's future access to capital and limit investor interest, leading to multiple contraction in the share price and higher cost of capital for project development, ultimately compressing cash flows and pressuring earnings growth.

- The ongoing push toward decarbonization and increasing adoption of renewable energy sources globally is likely to diminish gold's role as a portfolio hedge in the long term, resulting in downward pressure on demand and pricing, which would directly impact Galiano Gold's top line revenues and squeeze profit margins.

- Declining ore grades and limited proven reserves at the Asanko Gold Mine threaten to reduce production volumes over time, and without sufficient high-grade exploration success, this will lead to a persistent decrease in revenue and operating cash flow.

- Galiano Gold's heavy reliance on the regulatory and political stability of Ghana exposes it to escalating geopolitical risks and potential resource nationalism, which could disrupt operations, increase compliance costs and taxes, and jeopardize net margins as well as the feasibility of long-term capital-intensive projects.

- Sharp rises in operating costs driven by inflation, energy price increases, new royalty and sustainability levies from the Ghanaian government, and local currency appreciation against the US dollar will likely outpace productivity gains-resulting in sustained higher all-in sustaining costs and net margin compression even if gold prices remain elevated.

Galiano Gold Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Galiano Gold compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

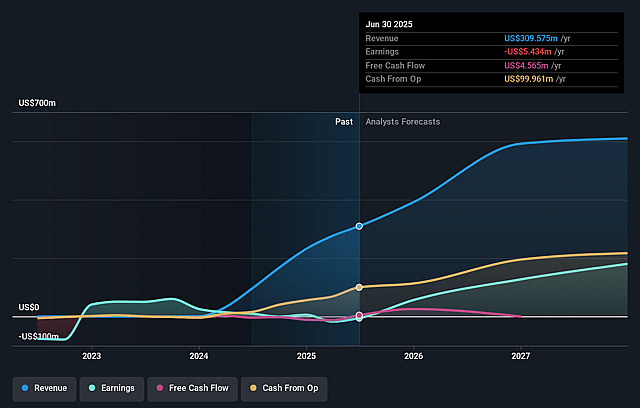

- The bearish analysts are assuming Galiano Gold's revenue will grow by 28.7% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from -1.8% today to 20.7% in 3 years time.

- The bearish analysts expect earnings to reach $136.8 million (and earnings per share of $1.25) by about September 2028, up from $-5.4 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 4.2x on those 2028 earnings, up from -118.3x today. This future PE is lower than the current PE for the US Metals and Mining industry at 17.8x.

- Analysts expect the number of shares outstanding to grow by 0.54% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.56%, as per the Simply Wall St company report.

Galiano Gold Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company reported strong operational improvements, including a 46 percent increase in gold production quarter-over-quarter, successful commissioning of key infrastructure like the secondary crusher and carbon regeneration kiln, and ongoing cost optimizations that have reduced all-in sustaining cash costs, all of which can contribute to higher profit margins and stronger cash flow in future periods.

- Exploration success at Abore has demonstrated mineralization well below current reserve pit shells, with high-grade, wide intercepts indicating significant resource growth potential through both open pit expansions and the eventual transition to underground mining, supporting the outlook for increased reserves and a longer mine life that could uplift revenues and earnings over the long-term.

- The balance sheet is robust with $115 million in cash and no debt, enabling the company to self-fund capital projects, accelerate high-value stripping at the Nkran deposit, and invest in organic growth and exploration without diluting shareholders, reducing financial risk and potentially supporting future dividend or buyback programs, which can positively affect earnings per share and share valuation.

- Ghana is highlighted as a stable mining jurisdiction with a mature regulatory framework, which positions Galiano Gold to benefit from secular industry trends as capital shifts away from higher-risk areas and towards established, lower-risk producers, likely resulting in improved investor appetite and a lower risk premium reflected in higher valuation multiples for its shares.

- The management team has demonstrated disciplined capital allocation and a commitment to operational excellence, with ongoing investments in processing efficiency and resource growth that could further reduce unit costs and boost margin expansion; as such, persistent operational improvements may strengthen net margins and overall financial resilience, contradicting expectations of long-term share price declines.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Galiano Gold is CA$2.49, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Galiano Gold's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$5.87, and the most bearish reporting a price target of just CA$2.49.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $660.2 million, earnings will come to $136.8 million, and it would be trading on a PE ratio of 4.2x, assuming you use a discount rate of 6.6%.

- Given the current share price of CA$3.43, the bearish analyst price target of CA$2.49 is 37.6% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Galiano Gold?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.