Catalysts

About Penumbra

Penumbra develops and commercializes advanced catheter based thrombectomy and embolization technologies to treat vascular and neurovascular diseases.

What are the underlying business or industry changes driving this perspective?

- Rapid adoption of CAVT for pulmonary embolism and deep vein thrombosis, reinforced by highly positive STORM PE and STRIKE PE data and strong physician enthusiasm, is poised to expand the treatable VTE population materially, supporting sustained double digit revenue growth and higher earnings power.

- Dedicated, scaled peripheral embolization sales infrastructure and successful launches such as Ruby XL are unlocking underpenetrated U.S. embolization demand and shifting mix toward higher margin products, supporting both top line acceleration and gross margin expansion.

- Next generation CAVT innovations, including Lightning Bolt 16 and Lightning Flash 3.0, meaningfully improve procedure speed, ease of use and safety. This could catalyze share gains from older mechanical technologies and convert more hospitals to Penumbra systems, increasing revenue density per account.

- Impending introduction of Thunderbolt into neurovascular stroke, combined with a thrombectomy and coil platform, may help reinvigorate stroke procedure growth and capture share in a large, under treated patient pool, potentially amplifying long term revenue and operating leverage.

- International growth reaccelerating as China headwinds subside, combined with U.S. VTE and embolization momentum and a trajectory toward a 70% plus gross margin by 2026, points to structurally higher free cash flow generation and expanding net margins over the coming years.

Assumptions

This narrative explores a more optimistic perspective on Penumbra compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts. How have these above catalysts been quantified?

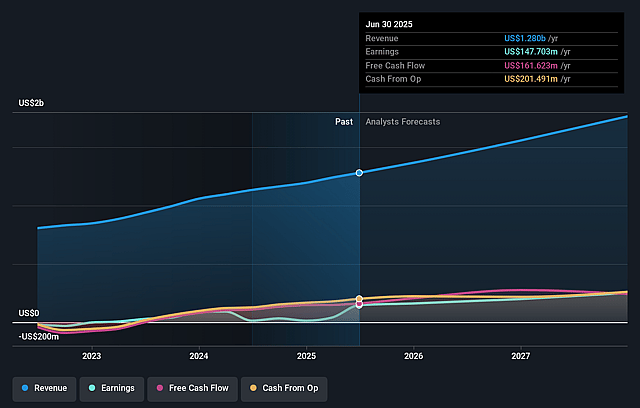

- The bullish analysts are assuming Penumbra's revenue will grow by 14.9% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 12.3% today to 16.7% in 3 years time.

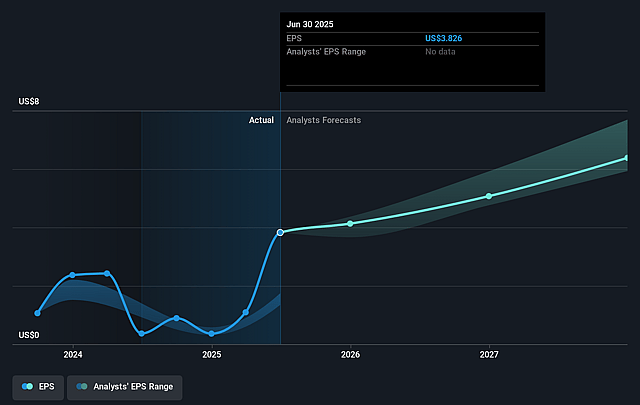

- The bullish analysts expect earnings to reach $337.9 million (and earnings per share of $8.26) by about December 2028, up from $164.0 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $243.5 million.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 54.1x on those 2028 earnings, down from 70.4x today. This future PE is greater than the current PE for the US Medical Equipment industry at 28.9x.

- The bullish analysts expect the number of shares outstanding to grow by 1.68% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.74%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Penumbra’s growth thesis relies heavily on rapid adoption of CAVT for VTE and PE. If hospital protocols and guideline updates move more slowly than management anticipates or PER team formation stalls, procedure volumes could plateau below expectations. This could limit long term revenue expansion and earnings compounding.

- The company is concentrating its growth engine in a few flagship technologies such as Lightning Flash, Lightning Bolt 16 and Thunderbolt. Any regulatory delay, safety concern or competing innovation that narrows their perceived clinical or economic advantage could compress pricing power, slow share gains and pressure both revenue growth and net margins.

- U.S. sales already represent over three quarters of revenue and are growing much faster than international markets. If the macro stroke and VTE markets in the U.S. continue to ebb or China and other key geographies fail to reaccelerate as expected, mix could remain skewed and constrain the durability of high teens revenue growth and operating margin expansion.

- Management has made large, ongoing investments in sales infrastructure, market access and R&D to capitalize on the STORM PE catalyst and embolization opportunity. If incremental volumes and pricing do not scale in line with these higher fixed and variable costs, SG&A and R&D intensity could remain elevated, limiting operating leverage and net margin improvement.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Penumbra is $355.0, which represents up to two standard deviations above the consensus price target of $306.33. This valuation is based on what can be assumed as the expectations of Penumbra's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $355.0, and the most bearish reporting a price target of just $186.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2028, revenues will be $2.0 billion, earnings will come to $337.9 million, and it would be trading on a PE ratio of 54.1x, assuming you use a discount rate of 7.7%.

- Given the current share price of $294.72, the analyst price target of $355.0 is 17.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Penumbra?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.