Key Takeaways

- Rapid growth of distributed and renewable energy threatens both customer retention and profitability due to declining demand for grid electricity and increased competition.

- Regulatory uncertainty and high nuclear operating costs risk eroding earnings stability and may necessitate plant closures or limit long-term investment viability.

- Leadership in reliable, low-emission nuclear capacity and strategic expansion into renewables positions Constellation Energy for sustained, stable growth amid rising power demand and supportive regulation.

Catalysts

About Constellation Energy- Produces and sells energy products and services in the United States.

- The rapid advancement and widespread adoption of distributed energy resources like rooftop solar and energy storage could erode Constellation Energy’s long-term customer base, undermining future load growth and putting downward pressure on revenues and market share as more commercial and residential customers bypass grid-supplied electricity.

- Political and social pushback against nuclear energy, driven by heightened concerns about radioactive waste management and the ever-present risk of high-profile nuclear incidents, may result in escalating regulatory costs, more stringent safety requirements, and an uncertain policy environment—all of which would increase operating costs, reduce net margins, and threaten the economic viability of Constellation’s nuclear fleet over time.

- Persistently high costs associated with aging nuclear plants and the heavy capital needed for license extensions may outpace what can be recovered in power markets or through regulatory mechanisms, leading to potential plant shutdowns and significantly reducing future earnings and cash flow reliability.

- Ongoing declines in the costs of renewables and batteries will intensify competition for traditional baseload nuclear and gas-fired generation, steadily eroding Constellation’s pricing power and compressing margins as low-cost renewable sources win increasing share of power generation.

- Regulatory and policy instability, particularly around carbon pricing, state-level mandates, and subsidies for renewables, could disrupt long-term planning and capital allocation, creating uncertainty for large-scale investment decisions and potentially undermining the consistency of future earnings and returns to shareholders.

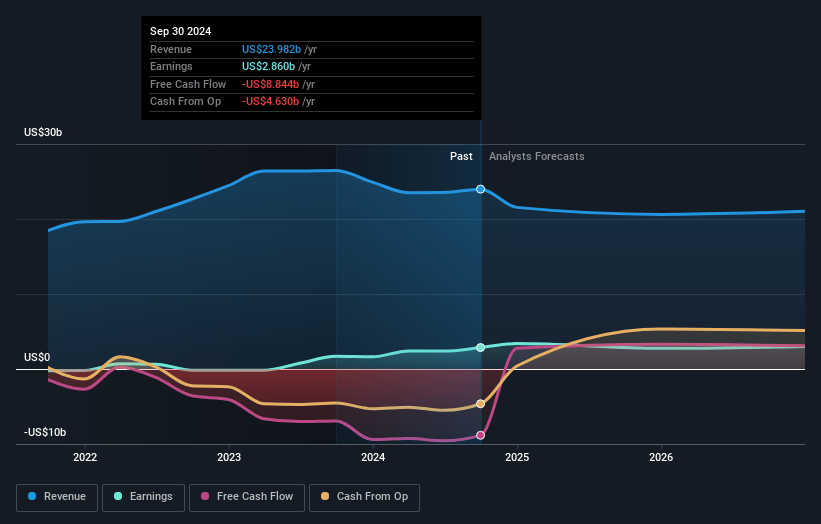

Constellation Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Constellation Energy compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Constellation Energy's revenue will decrease by 4.2% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 12.3% today to 7.1% in 3 years time.

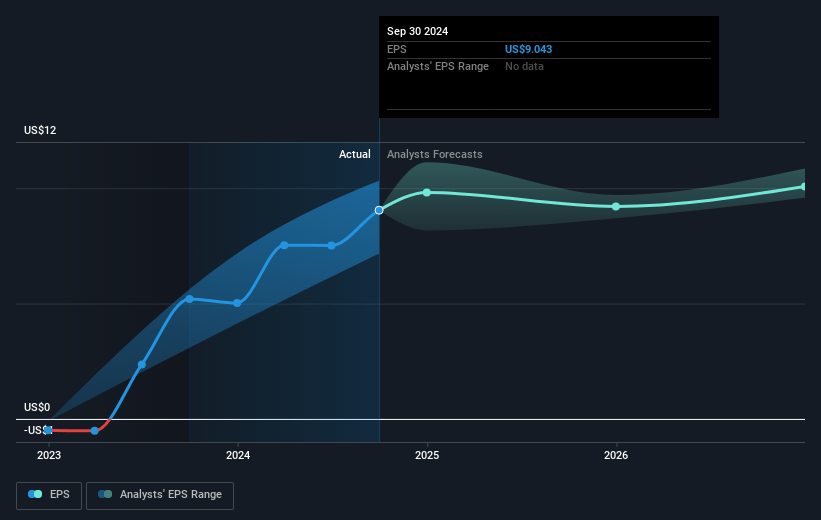

- The bearish analysts expect earnings to reach $1.5 billion (and earnings per share of $5.38) by about July 2028, down from $3.0 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 46.8x on those 2028 earnings, up from 34.0x today. This future PE is greater than the current PE for the US Electric Utilities industry at 22.0x.

- Analysts expect the number of shares outstanding to grow by 0.23% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.4%, as per the Simply Wall St company report.

Constellation Energy Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Accelerating demand for data center power driven by AI adoption and onshoring of manufacturing, together with electrification across multiple industries, is creating a secular growth trend in U.S. electricity usage, which positions Constellation Energy to benefit from rising generation volumes and elevated power prices, supporting revenue growth for the long term.

- Constellation’s industry-leading nuclear fleet and ability to relicense and upgrade existing assets provide durable production capacity with high reliability and low emissions, supporting stable high-margin base earnings and enabling above-market revenue growth through at least 2060.

- Structural inflation hedges, including the nuclear production tax credit (PTC) that escalates with inflation, protect Constellation’s earnings and cash flows even in lower power price environments, while providing multi-year visibility and financial stability for both margins and cash generation.

- Strategic acquisition and integration of Calpine adds significant natural gas and renewables capacity, expanding geographic reach and product offerings, while expected synergies are anticipated to add at least $2 in annual EPS and $2 billion in free cash flow beginning next year, materially boosting both earnings and free cash flow.

- Robust bipartisan and regulatory support for nuclear power, including continued and expanding tax incentives and inclusion in clean energy standards, underpins predictable profitability, lowers policy risk, and encourages further capital inflows that can support premium valuation multiples and thus support the share price.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Constellation Energy is $186.37, which represents two standard deviations below the consensus price target of $315.12. This valuation is based on what can be assumed as the expectations of Constellation Energy's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $385.0, and the most bearish reporting a price target of just $184.05.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $21.3 billion, earnings will come to $1.5 billion, and it would be trading on a PE ratio of 46.8x, assuming you use a discount rate of 6.4%.

- Given the current share price of $323.7, the bearish analyst price target of $186.37 is 73.7% lower.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.