Narratives are currently in beta

Key Takeaways

- Operational improvements and strategic asset reduction reduce costs and enhance network efficiency, positively impacting Norfolk Southern’s net margins and cost structure.

- Investments in technology, training, and the intermodal reservation system drive competitive advantage, volume growth, and revenue, while supporting financial stability.

- The company faces multiple revenue and margin pressures from declining coal prices, sector-specific challenges, fuel price normalization, and weather-related disruptions.

Catalysts

About Norfolk Southern- Engages in the rail transportation of raw materials, intermediate products, and finished goods in the United States.

- Continued execution of operational resilience and improvements, despite adverse weather conditions, is expected to enhance Norfolk Southern’s network efficiency and reduce costs, positively impacting net margins.

- The intermodal reservation system, which improves terminal visibility and maximizes train capacity, is projected to increase competitive advantage in the industry and drive volume growth, potentially leading to increased revenue.

- Strategic asset reduction, including storing locomotives and railcars, allows for decreased capital expenditure and improved fuel efficiency, enhancing overall cost structure and contributing to net margin improvement.

- Completion and potential continuation of line sales provide cash flow that assists in balance sheet repair, supporting improved earnings through cost management and financial stability.

- Investments in technology and operational training through the Thoroughbred Academy foreseeably bolster service performance and employee productivity, driving both revenue growth and margin expansion.

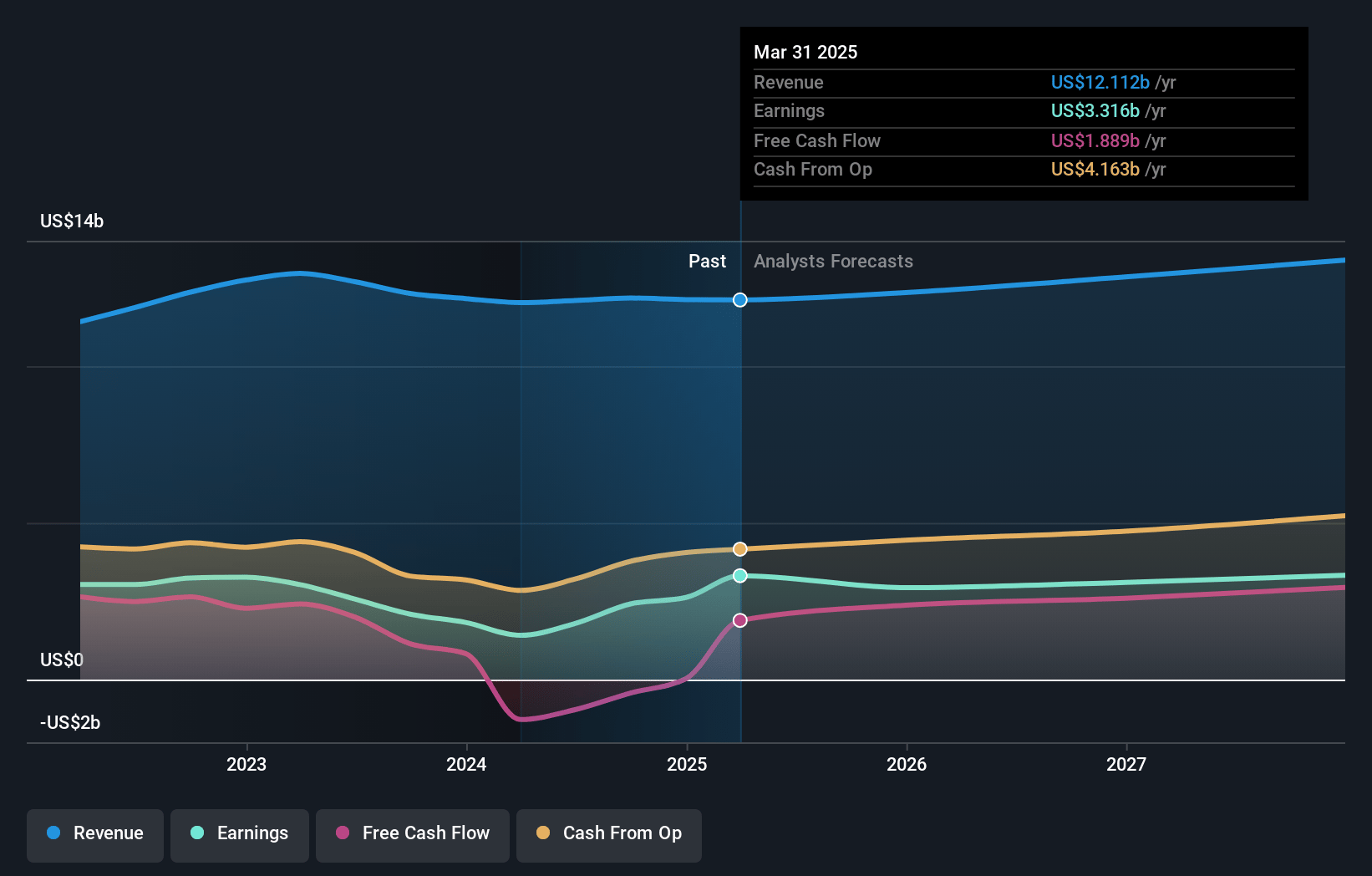

Norfolk Southern Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Norfolk Southern's revenue will grow by 4.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 19.8% today to 26.1% in 3 years time.

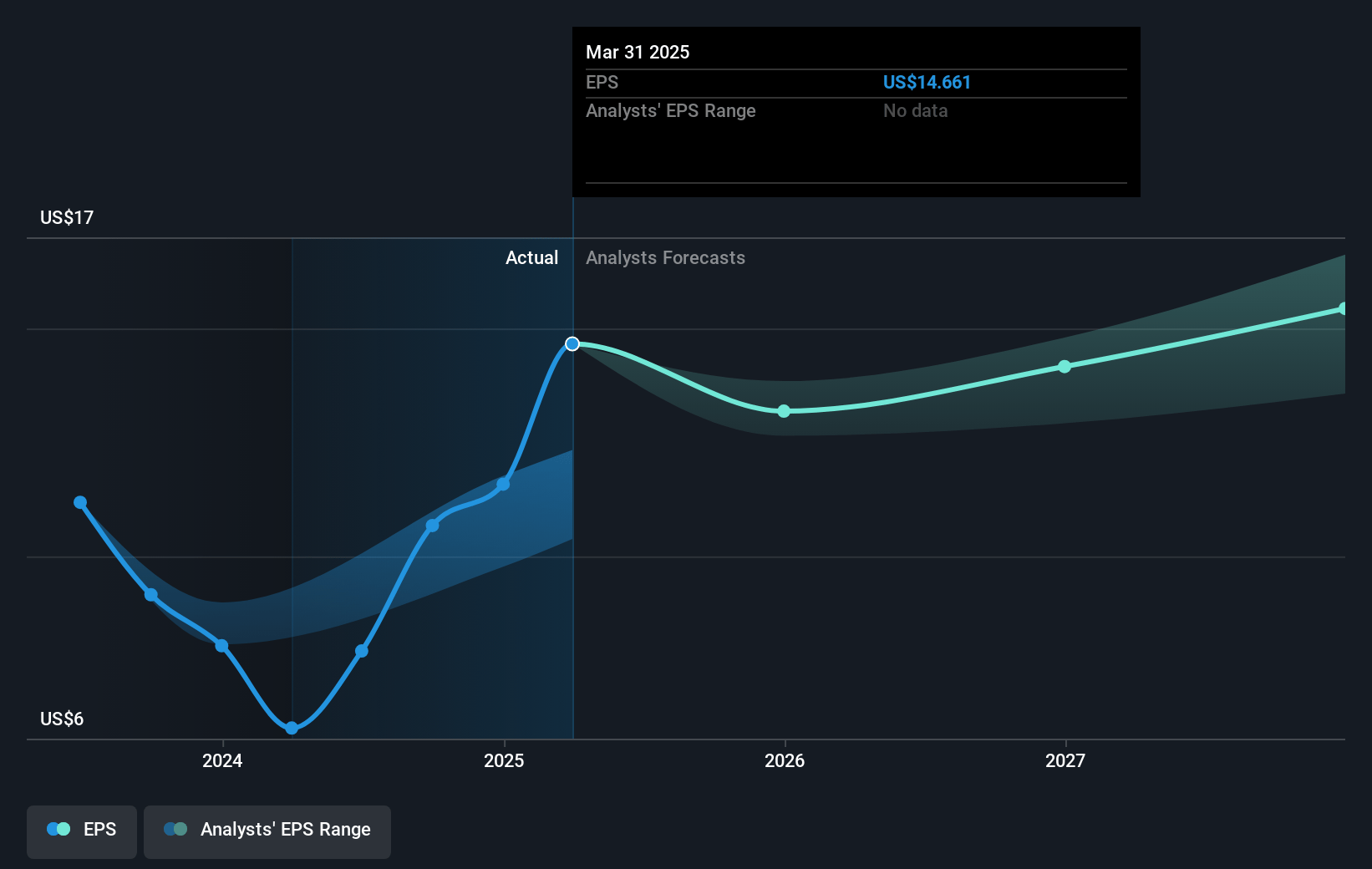

- Analysts expect earnings to reach $3.6 billion (and earnings per share of $16.83) by about January 2028, up from $2.4 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 20.1x on those 2028 earnings, down from 22.3x today. This future PE is lower than the current PE for the US Transportation industry at 28.9x.

- Analysts expect the number of shares outstanding to decline by 1.73% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.32%, as per the Simply Wall St company report.

Norfolk Southern Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company faces potential revenue headwinds from a decline in seaborne met coal prices and unfavorable intermodal market mix impacts, which could affect pricing power and revenue growth.

- NS is experiencing pressure on its export coal prices due to downward trends in seaborne met coal pricing, which, combined with headwinds from easing export prices, may negatively impact revenue and operating margins.

- There are sector-specific headwinds expected in automotive and metal markets, which could limit volume growth and potentially affect overall revenues and earnings.

- The normalization of fuel price impacts from 2022 historic highs is anticipated to be a significant revenue headwind, potentially affecting net margins and bottom-line profitability.

- Weather-related disruptions, such as hurricanes, despite showing resilience, still pose risks to operations and can result in increased costs, which could affect the net margins and financial performance in future quarters.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $274.88 for Norfolk Southern based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $320.0, and the most bearish reporting a price target of just $175.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $13.9 billion, earnings will come to $3.6 billion, and it would be trading on a PE ratio of 20.1x, assuming you use a discount rate of 7.3%.

- Given the current share price of $237.76, the analyst's price target of $274.88 is 13.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives