Narratives are currently in beta

Key Takeaways

- Strong merchandise business momentum, coupled with efficient operations and strategic pricing, positions CSX for stable revenue growth and solid net margins.

- Infrastructure investments and initiatives to convert truck volumes to rail promise enhanced reliability and intermodal revenue growth.

- CSX's revenue and profit margins face risks from weather disruptions, market challenges, energy fluctuations, and competitive pressures across various sectors.

Catalysts

About CSX- Provides rail-based freight transportation services.

- CSX is experiencing strong momentum in its merchandise business, with a 3% increase in volume and a 6% increase in revenue, which bodes well for future revenue growth as they continue to leverage their service leadership and new business initiatives.

- Efficiency improvements, such as using real-time data to optimize the network and reducing train starts despite volume growth, show potential for enhanced net margins by improving cost control and operational efficiency.

- Recent investments in infrastructure rebuilding, like those necessitated by the hurricanes, coupled with proactive engineering efforts, indicate long-term infrastructure improvements that may enhance reliability and potentially revenue growth through improved service.

- CSX emphasizes the development and deployment of initiatives designed to convert truck volumes to rail, presenting a growth catalyst for intermodal revenue and further merchandise revenue, which could aid in expanding revenue streams and increasing operating income.

- A strategic focus on diverse merchandise markets, especially chemicals, agriculture, and food, supports future revenue stability and growth, while effective pricing strategies in these segments should help maintain or increase net margins amidst mixed broader market conditions.

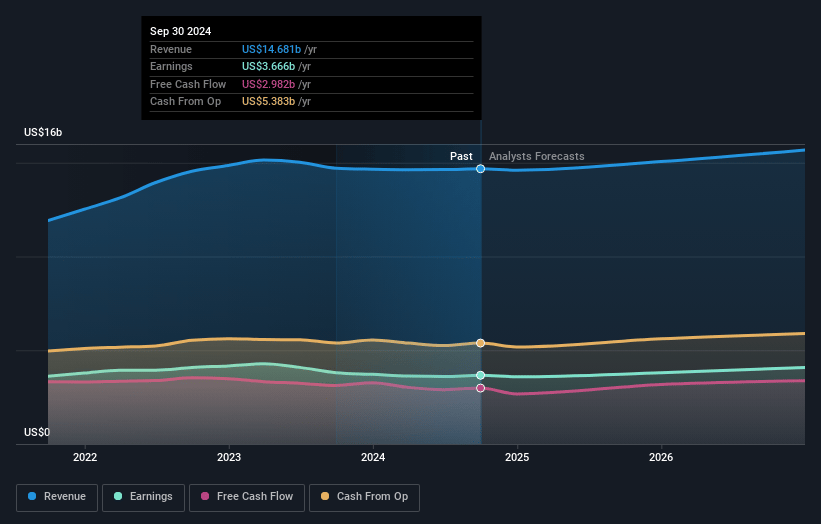

CSX Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming CSX's revenue will grow by 3.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 25.0% today to 27.3% in 3 years time.

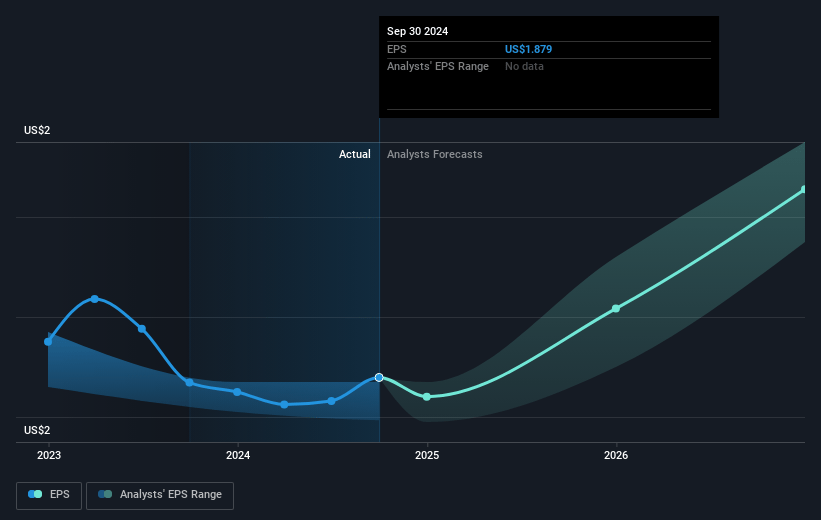

- Analysts expect earnings to reach $4.4 billion (and earnings per share of $2.46) by about December 2027, up from $3.7 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 19.4x on those 2027 earnings, up from 17.1x today. This future PE is lower than the current PE for the US Transportation industry at 28.9x.

- Analysts expect the number of shares outstanding to decline by 2.37% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.19%, as per the Simply Wall St company report.

CSX Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The impact of hurricanes, including the disruptions to revenue and potential rebuilding costs amounting to over $200 million, poses a risk to CSX's short-term financial outlook, potentially affecting revenue and profit margins.

- Ongoing challenges in the metals and automotive markets, coupled with unfavorable economic conditions like high retail prices and interest rates, could suppress demand and adversely impact CSX's revenue and earnings.

- The decline in coal revenue due to low natural gas prices and global benchmark reductions suggests a vulnerability to energy market fluctuations that could negatively influence CSX's revenue and operating income.

- Export coal markets, while stable, are highly susceptible to global economic conditions, leading to potential volatility in revenue from this segment, impacting CSX's earnings and financial stability.

- Continued pressure from a loose trucking market and uncertain railway labor conditions creates a competitive pricing environment that could compress CSX's operating margins and constrain revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $38.66 for CSX based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $44.0, and the most bearish reporting a price target of just $30.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $16.1 billion, earnings will come to $4.4 billion, and it would be trading on a PE ratio of 19.4x, assuming you use a discount rate of 7.2%.

- Given the current share price of $32.57, the analyst's price target of $38.66 is 15.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives