Key Takeaways

- Shifting industry trends and technology threaten the company's intermediary role, undermining pricing power and compressing margins.

- Regulatory demands and digital disintermediation increase costs while eroding growth prospects and the ability to maintain a competitive operational edge.

- Ongoing investment in automation and disciplined cost optimization have positioned the company for margin expansion and earnings growth despite industry headwinds.

Catalysts

About C.H. Robinson Worldwide- Provides freight transportation and related logistics and supply chain services in the United States and internationally.

- The accelerating trend of onshoring and reshoring is likely to materially reduce the complexity and volume of cross-border and international freight, directly undermining one of C.H. Robinson's core revenue streams and constraining long-term top-line growth.

- The rapid rise of autonomous logistics solutions-including AI-powered platforms, autonomous vehicles, and drones-is set to diminish the relevance of human-centric, intermediary brokers, threatening C.H. Robinson's role and compressing both brokerage margins and overall earnings over time.

- Intensifying regulatory scrutiny regarding carbon emissions, supply chain transparency, and cybersecurity is expected to drive up compliance costs and add operational rigidity, eroding operating margins and limiting the company's ability to maintain its historical rate of cost optimization.

- The continued commoditization of logistics, along with the proliferation of digital freight marketplaces and platforms that connect shippers directly to carriers, severely undermines C.H. Robinson's pricing power, reduces revenue per transaction, and exposes the company to enduring market share erosion.

- An overreliance on technology-enabled productivity improvements creates a risk of diminishing marginal returns; as competitive technology adoption saturates the industry, C.H. Robinson's unique operational edge will dissipate, ultimately restricting further net margin expansion and leaving revenue growth vulnerable to persistent market headwinds.

C.H. Robinson Worldwide Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on C.H. Robinson Worldwide compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

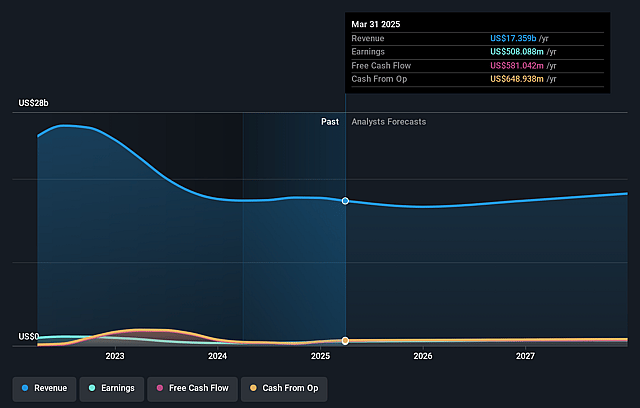

- The bearish analysts are assuming C.H. Robinson Worldwide's revenue will grow by 1.2% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 3.1% today to 3.7% in 3 years time.

- The bearish analysts expect earnings to reach $646.8 million (and earnings per share of $5.63) by about September 2028, up from $534.3 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 19.8x on those 2028 earnings, down from 28.2x today. This future PE is greater than the current PE for the US Logistics industry at 16.6x.

- Analysts expect the number of shares outstanding to decline by 0.1% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.37%, as per the Simply Wall St company report.

C.H. Robinson Worldwide Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Robust investment in proprietary AI-enabled automation and process improvements has created evergreen productivity gains of over 35% since 2022, positioning the company to expand margins and operating leverage even as freight volumes stagnate, thus supporting higher net margins and operating income in the long run.

- The company's lean operating model and discipline in decoupling headcount from volume growth are driving sustained cost optimization, resulting in lower operating expenses and a structurally improved cost base, which can raise long-term earnings and profitability.

- Outperformance in market share growth, margin expansion, and productivity improvement during an extended freight recession signals business model resilience, indicating that C.H. Robinson is well positioned to deliver revenue and earnings growth when freight cycles recover.

- Management's confidence in continued outperformance through technology deployment, strategic agility in pricing and capacity, and the ability to gain higher highs and higher lows in all market cycles suggest that revenue and earnings could rise as secular logistics demand rebounds.

- The company's strong balance sheet, improving leverage ratio, and steady capital returns to shareholders-including ongoing share repurchases and dividends-provide further downside protection and can support long-term share price appreciation through enhanced earnings per share and investor confidence.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for C.H. Robinson Worldwide is $88.54, which represents two standard deviations below the consensus price target of $117.56. This valuation is based on what can be assumed as the expectations of C.H. Robinson Worldwide's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $136.0, and the most bearish reporting a price target of just $71.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $17.7 billion, earnings will come to $646.8 million, and it would be trading on a PE ratio of 19.8x, assuming you use a discount rate of 7.4%.

- Given the current share price of $127.64, the bearish analyst price target of $88.54 is 44.2% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.