Narratives are currently in beta

Key Takeaways

- Verizon's strategic network expansion and focus on underserved markets support future revenue growth and EBITDA via enhanced broadband and mobility services.

- Investments in customer offerings and capital efficiency target increased market share, customer retention, and long-term free cash flow generation.

- Market competition and substantial capital commitments could pressure Verizon's margins and revenue growth, while policy changes might impact operational costs and financial flexibility.

Catalysts

About Verizon Communications- Through its subsidiaries, engages in the provision of communications, technology, information, and entertainment products and services to consumers, businesses, and governmental entities worldwide.

- Verizon's focus on expanding its fixed wireless access subscriber base to 8-9 million by 2028 could drive future revenue growth by tapping into underserved markets and leveraging existing C-Band and millimeter wave technology.

- The company’s strategy to cover more than 100 million households with its combined Fios and fixed wireless access offerings positions it for sustained revenue growth and EBITDA expansion as it enhances broadband penetration.

- Verizon’s ongoing investments in customer-first offerings, brand refresh, and strategic acquisitions like Frontier aim to increase market share and enhance customer retention, which could result in improved net margins.

- The planned expansion of Verizon’s 5G Ultra Wideband coverage to include 80-90% of their planned footprint by the end of 2025 supports future mobility revenue growth, particularly through fixed wireless access and business applications leveraging 5G.

- Verizon's continued focus on capital allocation efficiency and strategic investments in network infrastructure, coupled with its deleveraging efforts, are aligned to support enhanced free cash flow generation and potential share buybacks in the longer term.

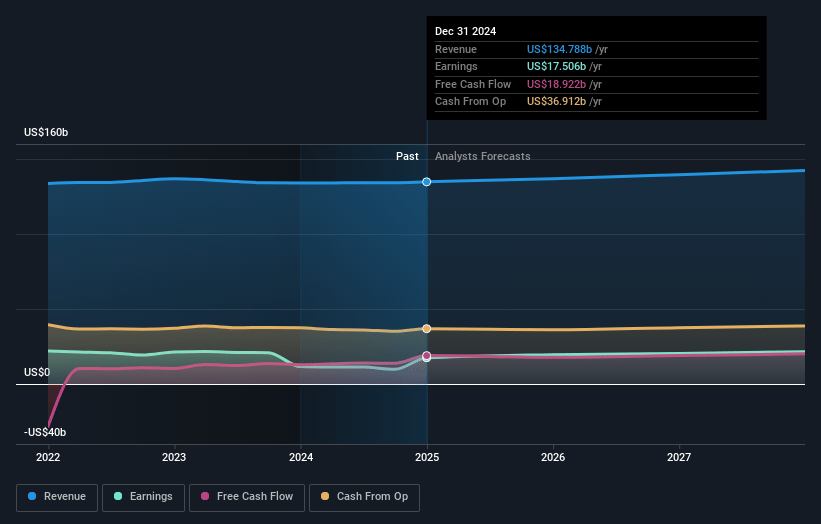

Verizon Communications Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Verizon Communications's revenue will grow by 1.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.3% today to 14.9% in 3 years time.

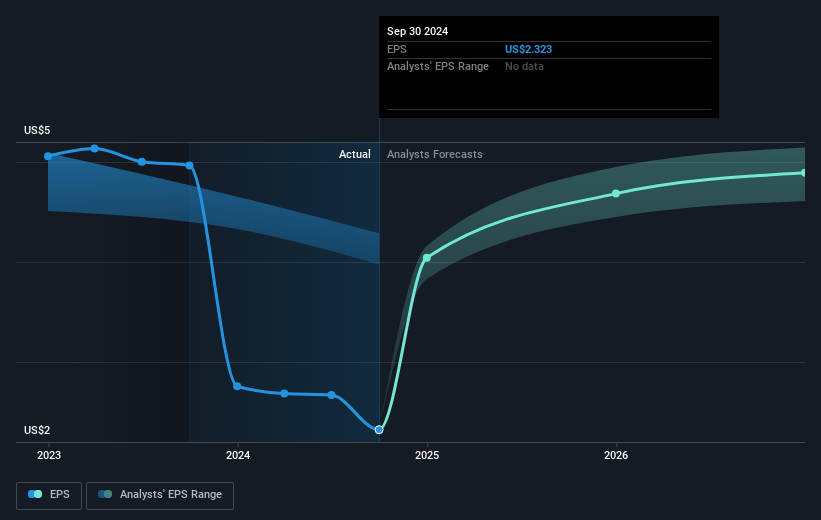

- Analysts expect earnings to reach $21.2 billion (and earnings per share of $5.01) by about January 2028, up from $9.8 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $18.2 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 11.3x on those 2028 earnings, down from 16.7x today. This future PE is lower than the current PE for the GB Telecom industry at 18.5x.

- Analysts expect the number of shares outstanding to grow by 0.14% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.92%, as per the Simply Wall St company report.

Verizon Communications Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Natural disasters and network disruptions, such as hurricanes, can affect Verizon's operations and infrastructure, potentially impacting service reliability and customer satisfaction, which can influence both revenues and earnings.

- The capital commitment to expanding their broadband through fiber and fixed wireless access involves significant expenditure, which could pressure net margins if returns are slower than anticipated.

- The integration and performance of acquired assets, such as TracFone, require ongoing attention and resources, posing risks to operational efficiency and potentially affecting net margins and overall earnings.

- Market competition in both fiber and wireless sectors, including pricing pressures from rivals and alternative technologies like satellite, may limit revenue growth and margin expansion.

- Policy and regulatory changes, such as those related to cash taxes, can increase operational costs and affect cash flow, potentially impacting net earnings and reducing financial flexibility for further investments.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $47.5 for Verizon Communications based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $56.0, and the most bearish reporting a price target of just $40.79.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $141.8 billion, earnings will come to $21.2 billion, and it would be trading on a PE ratio of 11.3x, assuming you use a discount rate of 5.9%.

- Given the current share price of $38.92, the analyst's price target of $47.5 is 18.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives