Key Takeaways

- Expanding manufacturing capacity and AI platform demand are poised to drive revenue growth and improve margins through economies of scale and efficiencies.

- Strategic investments in new technologies and international market expansion enhance revenue prospects and secure sustainable competitive advantages.

- Delays in financial filings and product mix shifts could hurt investor confidence and margins, while supplier dependency risks revenue growth and audit issues may lead to penalties.

Catalysts

About Super Micro Computer- Develops and sells high performance server and storage solutions based on modular and open architecture in the United States, Europe, Asia, and internationally.

- The transition to new generation platforms and increased AI demand are anticipated to drive continued revenue growth, as the company expects fiscal '25 growth to potentially mirror or surpass 2023 levels. This optimism is contingent on the supply chain keeping pace with demand, positively impacting future revenue.

- Expansion in manufacturing capacity and liquid cooling (DLC) technology utilization are set to support the anticipated rise in demand for AI-related platforms, which comprised over 70% of Q2 revenue, thereby potentially enhancing net margins through economies of scale and efficiencies in production.

- Strategic investments and initiatives, such as the $700 million convertible senior notes, are directed towards supporting business growth, including new architecture designs and the DLC fab initiatives. These actions can drive revenue expansion and improve net margins if executed effectively.

- With the company's strong focus on sustainable competitive advantages through liquid cooling technology and the Data Center Building Block Solution, which reduces customers' operational expenses and offers up to 40% lower total cost of ownership, Super Micro expects to improve its net margins and secure sustainable growth.

- Expansion into international markets, particularly in Asia and Europe, alongside the anticipated repeat of growth patterns seen in the U.S. market, can significantly enhance Super Micro's revenue and earnings prospects by diversifying and increasing its global market presence.

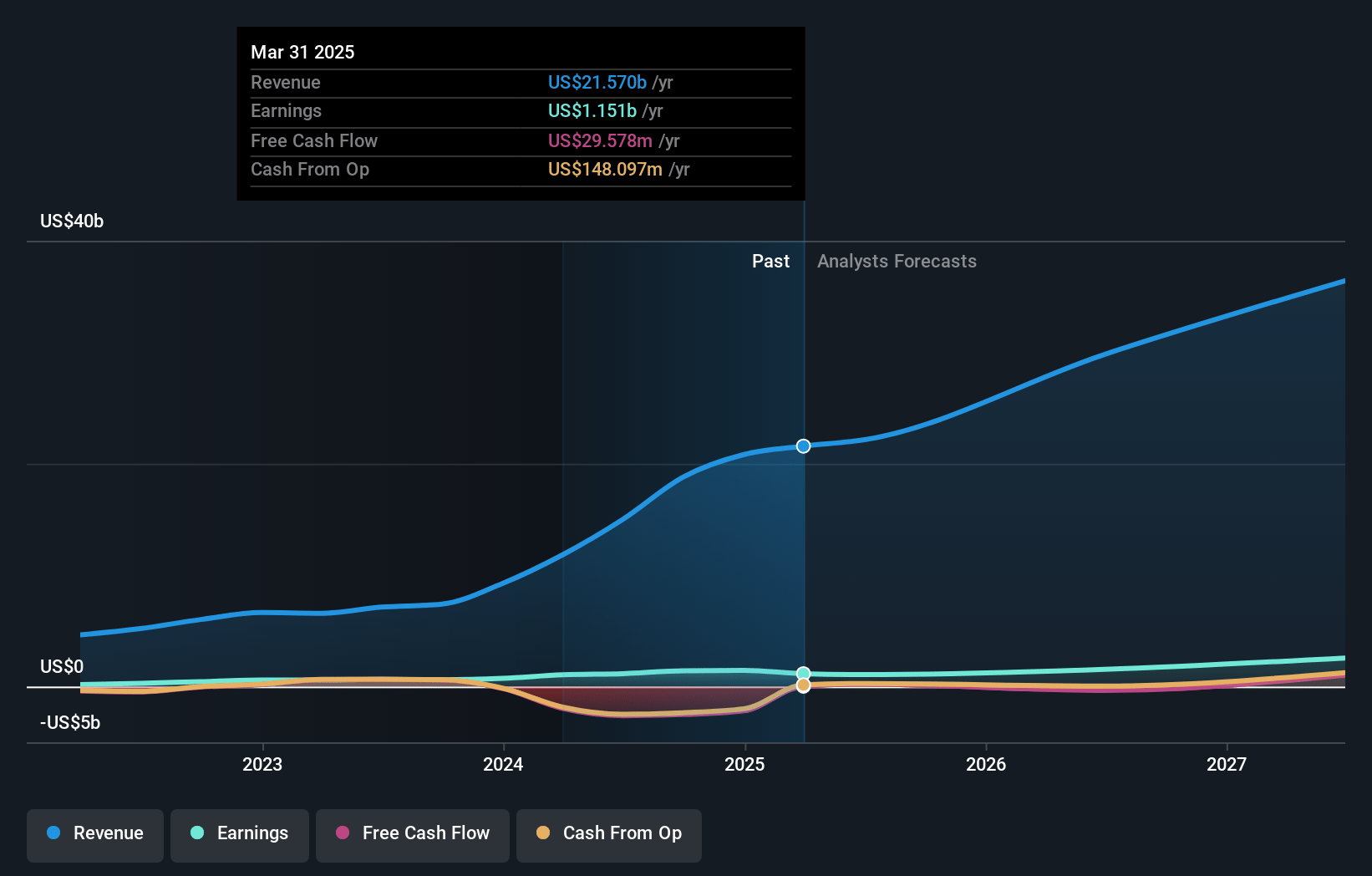

Super Micro Computer Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Super Micro Computer's revenue will grow by 25.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.9% today to 8.2% in 3 years time.

- Analysts expect earnings to reach $3.3 billion (and earnings per share of $3.66) by about April 2028, up from $1.4 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $4.1 billion in earnings, and the most bearish expecting $1.5 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 11.8x on those 2028 earnings, down from 14.8x today. This future PE is lower than the current PE for the US Tech industry at 12.9x.

- Analysts expect the number of shares outstanding to grow by 1.35% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.98%, as per the Simply Wall St company report.

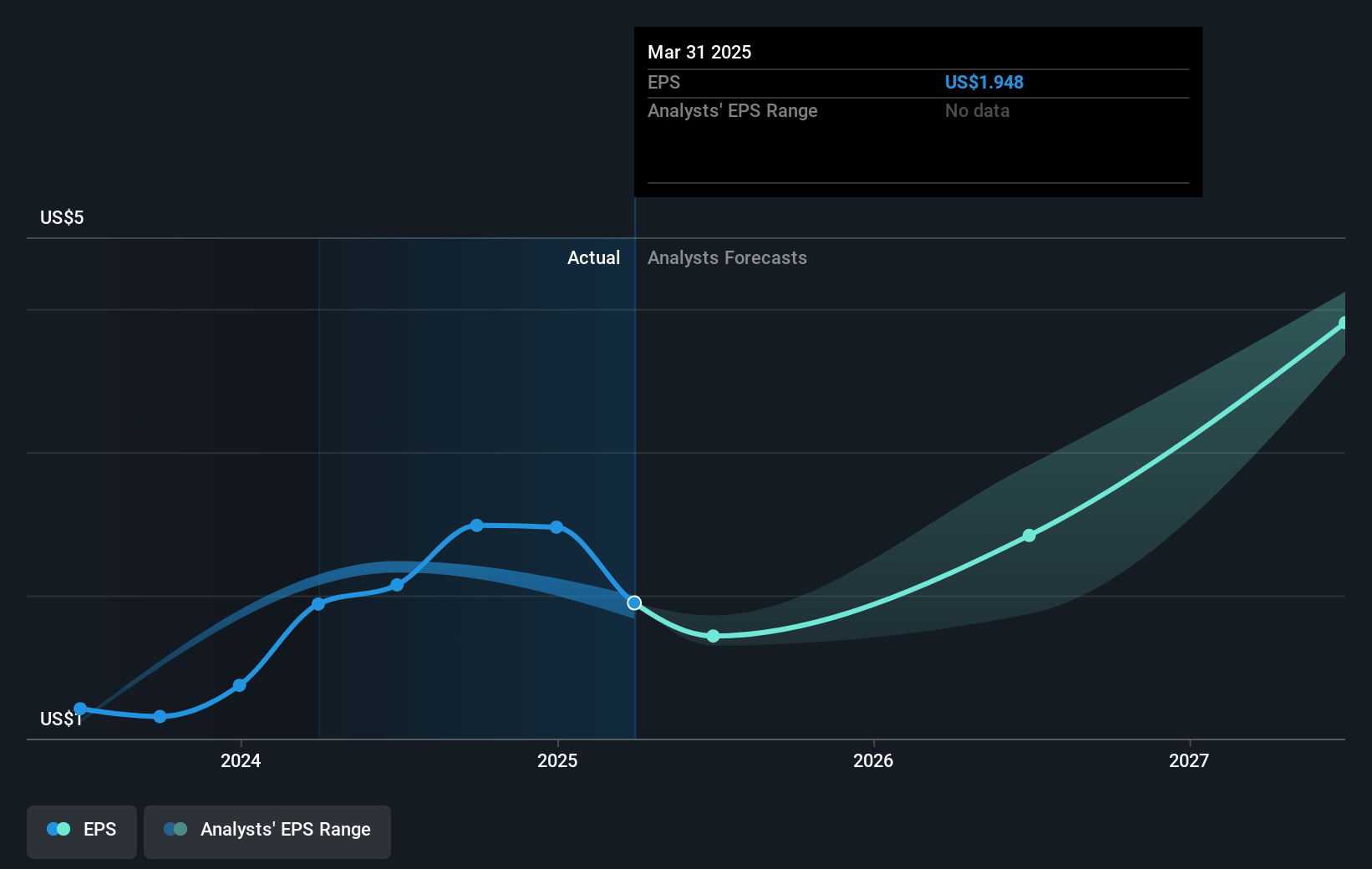

Super Micro Computer Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The delay in filing Super Micro's 10-K and 10-Q forms could lead to adverse market perceptions and financial impacts, such as reduced investor confidence and potential disruptions in cash flow, affecting earnings stability.

- Fluctuations in product and customer mix have pressured gross margins, which declined from 13.1% to 11.9% quarter-over-quarter, signaling potential risks to future net earnings if these trends continue.

- Increasing competition in AI systems and liquid cooling technology may exert additional pressure on pricing and margins, potentially impacting net margins as more players enter the market.

- Dependency on key suppliers like NVIDIA for GPU allocations and potential delays in supply could affect Super Micro's ability to meet demand, putting anticipated revenue growth at risk.

- Any further delays in resolving audit processes and filing requirements with the SEC may result in regulatory penalties or further market skepticism, directly impacting financial stability and net earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $50.581 for Super Micro Computer based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $93.0, and the most bearish reporting a price target of just $15.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $40.7 billion, earnings will come to $3.3 billion, and it would be trading on a PE ratio of 11.8x, assuming you use a discount rate of 8.0%.

- Given the current share price of $36.0, the analyst price target of $50.58 is 28.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.