Narratives are currently in beta

Key Takeaways

- Successful expansion in Green Energy Solutions and strategic partnerships boost future revenue potential with consistent growth opportunities.

- Improved gross margins and effective expense management indicate higher profitability and stable earnings through diversified revenue streams.

- Declining sales in key segments and inventory-related risks could challenge Richardson Electronics' revenue stability and financial health amidst uncertain market conditions.

Catalysts

About Richardson Electronics- Engages in the provision of engineered solutions, power grid and microwave tube, and related consumables worldwide.

- The successful growth of the Green Energy Solutions (GES) business, with a 129% increase in sales for Q2, is driven by global expansion efforts and exclusive partnerships with top wind turbine operators. This expansion is likely to boost future revenues as Richardson Electronics continues to penetrate the market further.

- The improvement in gross margins across the board, particularly in the Healthcare division and PMT sales due to better product mix and manufacturing efficiencies, indicates a positive outlook for net margins and earnings.

- The focus on repowering wind turbines and securing long-term projects like ULTRA3000, listed on the bill of materials for repower programs, should lead to predictable and consistent revenue streams, enhancing future earnings stability.

- The company's approach of designing new products in collaboration with strategic partners to fill technology gaps presents opportunities for increased revenue channels and diversified income streams in power management and RF/microwave applications.

- Richardson Electronics' strategy of maintaining a strong balance sheet and managing operating expenses effectively could increase operating leverage, resulting in higher profitability as sales continue to grow.

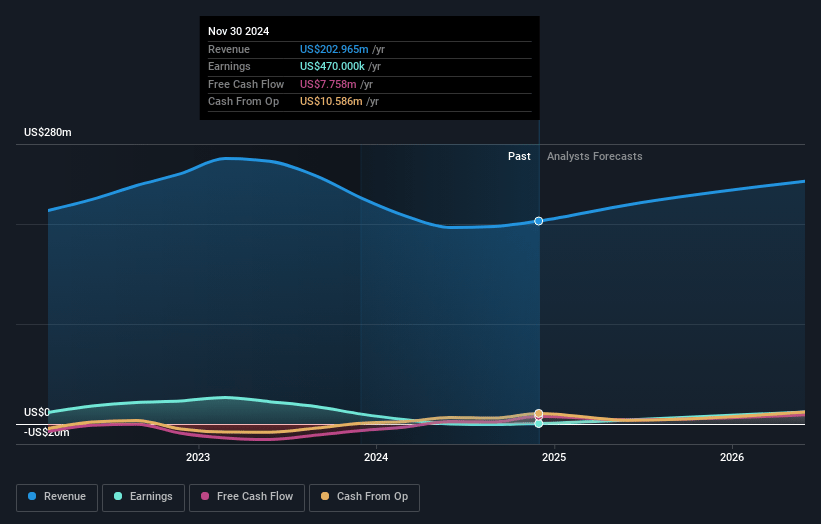

Richardson Electronics Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Richardson Electronics's revenue will grow by 13.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 0.2% today to 15.2% in 3 years time.

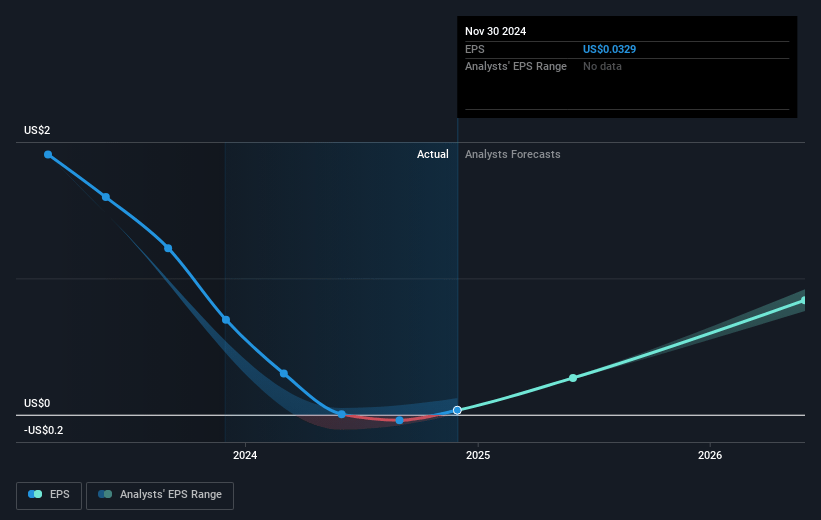

- Analysts expect earnings to reach $45.7 million (and earnings per share of $3.17) by about January 2028, up from $470.0 thousand today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 5.8x on those 2028 earnings, down from 404.4x today. This future PE is lower than the current PE for the US Electronic industry at 25.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.07%, as per the Simply Wall St company report.

Richardson Electronics Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The Healthcare division experienced a 22.8% decline in sales, raising concerns about the sustainability of revenue from this segment.

- Canvys' 6.0% decrease in sales, primarily due to lower demand in European markets, may indicate challenges in maintaining revenue growth amid macroeconomic headwinds.

- The company's reliance on inventory sales, especially in the ULTRA3000 segment, might lead to inventory depletion issues, affecting future revenue and cash flow stability.

- Challenges in the semiconductor wafer fab business visibility and reliance on uncertain customer forecasts could affect long-term revenue predictability.

- Significant inventory buildup related to Thales could represent a financial risk if future sources for these products are not secured, potentially impacting cash flow and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $15.5 for Richardson Electronics based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $300.1 million, earnings will come to $45.7 million, and it would be trading on a PE ratio of 5.8x, assuming you use a discount rate of 7.1%.

- Given the current share price of $13.19, the analyst's price target of $15.5 is 14.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives