Last Update 16 Jun 26

Fair value Increased 5.56%OSS: Defense AI Momentum And Acquisition Optionality Will Shape Measured Upside

For this Narrative Update on One Stop Systems, the analyst fair value estimate has moved from $18 to $19, reflecting recent Street price target increases and analyst comments that indicate greater confidence in the business momentum following management meetings.

Analyst Commentary

Recent commentary on One Stop Systems reflects a series of upward price target revisions following management meetings, with analysts pointing to higher confidence in the company’s business momentum and execution.

Bullish Takeaways

- Bullish analysts raised formal price targets on One Stop Systems multiple times, which signals a higher assessment of the company’s potential value based on the information they received from recent management meetings.

- Comments about increased confidence in business momentum suggest that execution on current initiatives is tracking in line with, or better than, prior expectations, which feeds directly into their fair value work.

- The sequence of price target increases, rather than a single adjustment, indicates that bullish analysts are revisiting their models as they gain more detail on the company’s pipeline and growth plans.

- These higher targets provide a reference point for investors on how the Street currently frames risk and reward for One Stop Systems, particularly around revenue growth potential and the scalability of its business model.

Bearish Takeaways

- The available research focuses on higher targets and positive momentum, which means investors have limited visibility on more cautious views, such as concerns about execution risk, competitive pressures, or project timing.

- Upward price target revisions typically rely on management commentary and projections, so there is a risk that expectations embedded in these targets could prove optimistic if underlying assumptions do not play out as anticipated.

- Concentration of commentary from bullish analysts can create an expectations bar that is harder for One Stop Systems to meet, potentially increasing sensitivity to any future disappointments in results or guidance.

- Investors may need to stress test their own valuation scenarios for One Stop Systems, since the research provided offers limited discussion of downside cases or more conservative growth assumptions.

What’s in the News for One Stop Systems

- One Stop Systems plans to showcase a range of mission-ready, rugged AI compute products and integrated solutions for modern warfighters at Special Operations Forces Week, scheduled for May 19 to 21, 2026, at the Tampa Convention Center, including servers and embedded platforms for vehicles, unmanned aerial systems and soldier-worn applications, with partners Latent AI, Maris Technologies and Tauro Tech featured at booth #5006. (Source: Product-related announcement)

- The company is looking for acquisitions, with CEO Michael Knowles stating on the Fourth Quarter 2025 conference call that a strengthened balance sheet provides flexibility to pursue selective deals that could complement One Stop Systems’ technology platform, expand its customer base and add capabilities over time. (Source: Earnings call commentary)

- One Stop Systems received an initial purchase order valued at over US$500,000 from a renewable-energy technology customer focused on clean energy, with follow-on orders expected by the company to exceed US$1,000,000 year-over-year and potentially reach a US$10,000,000 opportunity over five years, supported by rugged Gen5 servers and AI accelerator systems for remote environments. (Source: Client announcement)

- The company issued consolidated earnings guidance for full-year 2026 and stated that it expects revenue growth of 20% to 25% for the period. (Source: Corporate guidance)

Valuation Changes for One Stop Systems

- Fair Value: $18 to $19, a modest increase in the analyst estimate for One Stop Systems stock.

- Discount Rate: 8.43% to 8.53%, a slight uptick in the rate used to discount future cash flows.

- Revenue Growth: 20.16% to 20.16%, effectively unchanged in the model assumptions for future sales expansion.

- Net Profit Margin: 7.55% to 7.42%, a small reduction in expected profitability levels.

- Future P/E: 149.73x to 161.36x, a moderate step up in the valuation multiple applied to projected earnings.

Key Takeaways

- Sole-source supplier wins and proprietary platform launches drive long-term revenue growth, higher margins, and enhanced market positioning for AI-driven and autonomous edge platforms.

- Growing demand across defense, autonomous vehicles, and healthcare, plus strategic investments, expand OSS's addressable market and support sustained earnings predictability.

- Dependence on volatile government contracts, rapid tech shifts, integrated competition, supply issues, and weak European growth threaten revenue stability, profitability, and future market position.

Catalysts

About One Stop Systems- Designs, manufactures, and markets rugged high-performance compute, high speed switch fabrics, and storage systems for edge applications of artificial intelligence and machine learning, sensor processing, sensor fusion, and autonomy in the United States and internationally.

- Multi-year defense and commercial platform wins and sole-source supplier agreements provide strong revenue visibility and support higher margins, as OSS becomes the incumbent compute and storage supplier for next-generation AI-driven and autonomous edge platforms. This positions revenue and gross margin for sustained growth.

- Sharply rising demand for high-performance, ruggedized computing and storage, driven by greater AI, machine learning, edge data processing, and sensor fusion initiatives-especially in defense, autonomous vehicles, and healthcare-expands OSS's addressable market and underpins long-term revenue growth.

- Introduction of proprietary PCIe Gen5 platforms like Ponto, tailored for the fast-growing composable infrastructure market and data center upgrades for high-wattage GPU workloads, creates new product/revenue streams and strengthens average selling prices, supporting both top-line growth and gross margin enhancement starting in 2026.

- Strong sequential and year-over-year growth in bookings, a robust book-to-bill ratio (above 2), and a diversified pipeline of platform-level opportunities indicate increasing predictability in future earnings and operating leverage, as a higher mix of production contracts move through the margin expansion life cycle.

- Ramping investments in R&D, strategic hiring from the defense sector, and increased bid/proposal activity with new government and commercial opportunities position OSS to benefit from the ongoing shift to modular, scalable HPC architectures and government onshoring/regulatory requirements, further supporting revenue and margin expansion in the medium-to-long term.

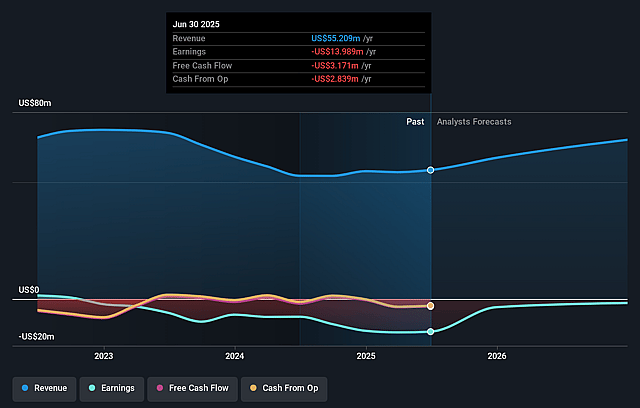

One Stop Systems Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming One Stop Systems's revenue will grow by 20.2% annually over the next 3 years.

- Analysts are not forecasting that One Stop Systems will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate One Stop Systems's profit margin will increase from -3.4% to the average US Tech industry of 7.4% in 3 years.

- If One Stop Systems's profit margin were to converge on the industry average, you could expect earnings to reach $4.5 million (and earnings per share of $0.15) by about June 2029, up from -$1.2 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 163.2x on those 2029 earnings, up from -361.4x today. This future PE is greater than the current PE for the US Tech industry at 45.1x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.53%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Heavy reliance on large, lumpy government and defense contracts means OSS is exposed to delays and unpredictability from budget cycles, continuing resolutions, and shifting government funding timelines; such volatility could negatively impact revenue stability and growth visibility.

- OSS's core business remains highly concentrated in specialized high-performance hardware for rugged and edge applications, exposing the company to rapid technological obsolescence and significant R&D investment requirements, which may compress future net margins and dilute profitability.

- Accelerated industry transition to integrated solutions and commoditization-especially as hyperscalers and larger OEMs move toward fully integrated end-to-end platforms-threatens OSS's position as a niche supplier, risking a loss of market share and downward pressure on ASPs (average selling prices), hitting gross margin and earnings potential.

- Ongoing supply chain disruptions and lengthening component lead times, highlighted by the company's own remarks, pose substantial risks to execution of the second-half ramp and future production scaling; such headwinds could increase costs, delay deliveries, and adversely impact both revenue growth and net earnings.

- The Bressner segment's very modest growth rate (projected at 2–9%) contrasts with OSS's higher target, and ongoing weakness in European IT spend and international economic uncertainty may drag consolidated performance, potentially dampening overall revenue growth and limiting operating leverage.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $19.0 for One Stop Systems based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $21.0, and the most bearish reporting a price target of just $18.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $60.9 million, earnings will come to $4.5 million, and it would be trading on a PE ratio of 163.2x, assuming you use a discount rate of 8.5%.

- Given the current share price of $17.23, the analyst price target of $19.0 is 9.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on One Stop Systems?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.