Last Update 02 Jun 26

NTGR: Share Repurchases Will Drive Future Upside Despite Weaker Near-Term Margins

Analysts have maintained their $35.00 price target for NETGEAR, noting only modest adjustments to assumptions for the discount rate, profit margin, and future P/E that do not materially change their view of the stock's valuation.

What's in the News

- From January 1, 2026 to March 27, 2026, NETGEAR repurchased 928,778 shares, representing 3.32% of its shares, for US$20 million under its existing buyback program. [Source: Key Developments]

- The company has now completed repurchases of 5,440,899 shares, representing 18.89% of its shares, for a total of US$115.14 million under the buyback announced on October 27, 2021. [Source: Key Developments]

- For the second quarter ending June 28, 2026, NETGEAR expects net revenue in the range of US$150 million to US$165 million. [Source: Corporate Guidance]

- The company expects its GAAP operating margin for the same quarter to be in a range from an 8.4% loss to a 5.4% loss. [Source: Corporate Guidance]

Valuation Changes

- Fair Value: Held steady at $35.0 per share, with no change in the central valuation estimate.

- Discount Rate: Decreased slightly from 8.78% to 8.72%, reflecting a small adjustment to the required return used in the model.

- Revenue Growth: Kept essentially unchanged at 106.90%, with no practical shift in the growth assumption.

- Net Profit Margin: Increased slightly from 11.17% to 11.22%, indicating a minor upward tweak to profitability expectations.

- Future P/E: Declined slightly from 11.78x to 11.71x, showing a small reduction in the valuation multiple applied to future earnings.

Key Takeaways

- Shift toward enterprise networking, cloud-managed solutions, and services is enhancing high-margin, recurring revenue streams and supporting sustained margin improvement.

- Expanded premium home networking portfolio and strengthened cybersecurity positioning are enabling greater market share in both consumer and enterprise segments.

- Intensifying competition, commoditization, and supply constraints threaten NETGEAR's pricing power, growth prospects, and margins across both consumer and business segments.

Catalysts

About NETGEAR- Provides connectivity solutions the Americas; Europe, the Middle East, Africa; and the Asia Pacific.

- NETGEAR's investments in expanding its ProAV and SMB/cloud-managed networking business (notably through NFB, the Exium acquisition, and professional services) directly align with the increasing global demand for robust enterprise and hybrid work solutions. These efforts are driving higher-margin revenue streams and recurring revenue potential, likely to bolster both revenue growth and improve net margins over time.

- The continued proliferation of connected devices and adoption of advanced wireless standards (WiFi 7, mesh systems) are increasing demand for high-performance home networking; NETGEAR's broadened product portfolio-especially the introduction of mid

- and high-end mesh offerings like Orbi 370-positions the company to capture share in both premium and mainstream segments, supporting future top-line growth and margin expansion.

- Heightened focus on cybersecurity and regulatory/compliance trends, combined with intensified scrutiny of Chinese networking competitors, strengthens NETGEAR's market positioning as a trusted, independent US-based supplier. This increases its potential to gain share in enterprise, government, and retail channels, directly supporting revenue growth and stabilizing gross margins.

- The company's ongoing operational optimization-including streamlined supply chain management, leaner inventory, in-sourcing of software development, and organizational restructuring-has already led to record gross margins and provides a foundation for sustainable margin improvement, enhanced earnings quality, and improved operating leverage as growth resumes.

- Scaling of subscription-based services-including expanded software/AV services and integration of security solutions-gives NETGEAR more exposure to high-margin, recurring revenue streams. This transition from reliant hardware sales to service-based models is set to drive both net margin expansion and revenue stability over the longer term.

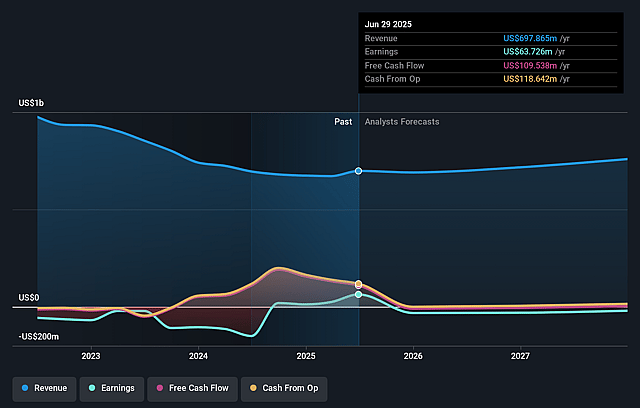

NETGEAR Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming NETGEAR's revenue will grow by 1.1% annually over the next 3 years.

- Analysts are not forecasting that NETGEAR will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate NETGEAR's profit margin will increase from -3.6% to the average US Communications industry of 11.2% in 3 years.

- If NETGEAR's profit margin were to converge on the industry average, you could expect earnings to reach $80.7 million (and earnings per share of $3.74) by about June 2029, up from -$24.9 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 12.0x on those 2029 earnings, up from -28.8x today. This future PE is lower than the current PE for the US Communications industry at 36.2x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.72%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The intense price competition in the U.S. retail home networking market-especially from low-cost players like TP-Link-has resulted in a "dog fight" for market share, declining average selling prices, and oscillating share gains/losses, which could continue to pressure NETGEAR's consumer revenue and gross margins over the long term.

- The rapid commoditization of home networking hardware, highlighted by the need to aggressively expand into "good, better, best" low-end mesh products, risks further eroding brand differentiation and pricing power, threatening sustainable ASPs and profitability in the core consumer segment.

- NETGEAR's future growth case relies heavily on scaling high-margin, recurring services revenue (particularly in NFB and home networking), but these initiatives are still nascent and face execution risk; slow adoption or under-penetration of premium, subscription, or services offerings could constrain expected earnings and margin expansion.

- Persistent supply constraints and component shortages, as repeatedly emphasized for ProAV Managed Switch products, have resulted in growing sales backlogs-if not resolved, these bottlenecks could prevent NETGEAR from capturing full top-line growth, while prolonged inefficiencies may increase inventory risk and compress earnings.

- Despite successes in diversification, NETGEAR remains exposed to industry trends favoring cloud-managed networking and integrated smart home ecosystems-if customers shift away from on-premise hardware toward competitors' end-to-end ecosystems (or towards cloud-based solutions), NETGEAR's addressable market, revenues, and margins could face secular pressure over time.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $35.0 for NETGEAR based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $719.0 million, earnings will come to $80.7 million, and it would be trading on a PE ratio of 12.0x, assuming you use a discount rate of 8.7%.

- Given the current share price of $26.71, the analyst price target of $35.0 is 23.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on NETGEAR?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.