Narratives are currently in beta

Key Takeaways

- Divesting non-core businesses and integrating medical operations may focus growth in medical and expand revenue opportunities.

- Strategic cost adjustments and facility relocations aim to enhance efficiency and margins, with benefits to shareholders via EPS and debt reduction.

- Declines in net sales and gross margins, alongside inventory and market demand challenges, threaten Kimball Electronics' revenue forecasts and short-term profitability.

Catalysts

About Kimball Electronics- Engages in the provision of electronics manufacturing, engineering, and supply chain support services to customers in the automotive, medical, and industrial end markets.

- The restructuring of the company by divesting the non-core AT&M business and integrating the medical CMO business into the core EMS portfolio could lead to increased focus on key growth areas in the Medical vertical. This is likely to impact revenue positively by opening up new customer opportunities.

- The strategic focus on high-growth market spaces, such as domain controllers in Automotive and energy storage solutions in Industrial, may enable Kimball Electronics to capture new revenue streams and expand market share.

- The proactive cost adjustments in response to market demand softness and efforts to right-size resources are expected to improve operational efficiencies, resulting in potential net margin improvements as demand stabilizes.

- The closure of the Tampa facility and the corresponding relocation of production to Mexico and Jasper is a strategic move to enhance competitiveness and reduce overhead, likely contributing to better net margins by streamlining efficiencies.

- The company’s focus on generating positive cash flow and reducing debt levels while maintaining a strong balance sheet, along with the potential for further share buybacks, could enhance earnings per share (EPS) over time, benefiting shareholders.

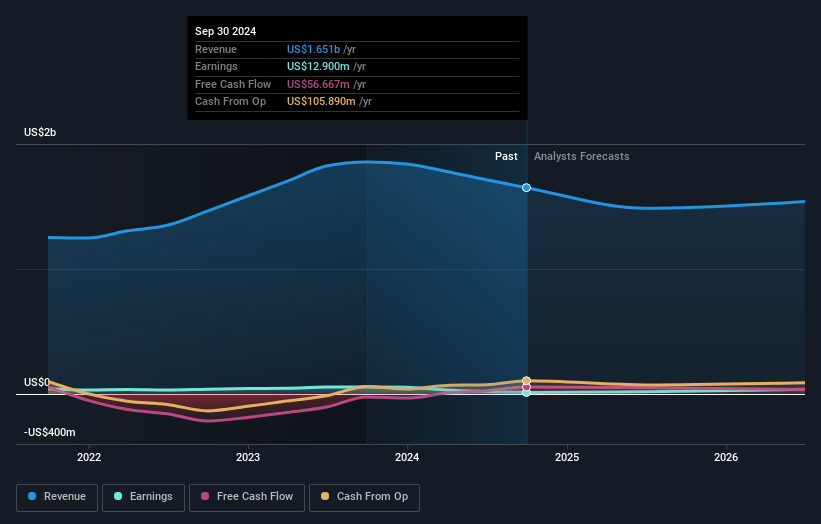

Kimball Electronics Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Kimball Electronics's revenue will decrease by -5.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 0.8% today to 4.4% in 3 years time.

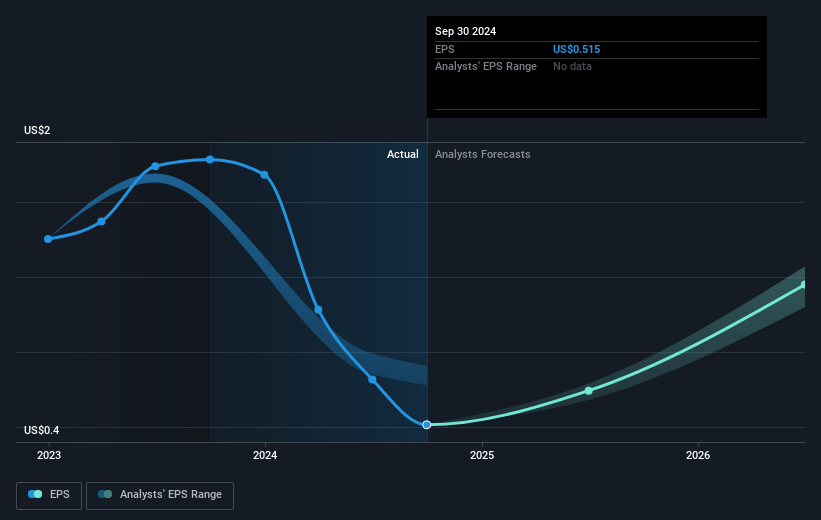

- Analysts expect earnings to reach $61.6 million (and earnings per share of $2.37) by about January 2028, up from $12.9 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.9x on those 2028 earnings, down from 35.5x today. This future PE is lower than the current PE for the US Electronic industry at 25.5x.

- Analysts expect the number of shares outstanding to grow by 1.77% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.34%, as per the Simply Wall St company report.

Kimball Electronics Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company experienced a significant 15% decline in net sales year-over-year, reflecting challenges in its core markets that could dampen future revenue growth.

- The closure of the Tampa manufacturing facility, though intended to streamline operations, involves restructuring costs of $8 million to $11 million, which could negatively impact short-term earnings.

- Persistent inventory challenges, particularly in the Automotive vertical due to overstocking and demand fluctuations, may continue to pressure profit margins and lead to increased holding costs.

- Decreases in gross margin to 6.3% from adjustments in operational efficiencies coupled with weak demand in industrial sectors, may hinder overall profitability improvements.

- Uncertainty related to the broader economic environment, including the impact of market demand softness and currency fluctuations, could disrupt revenue forecasts and EBITDA margin performance.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $24.0 for Kimball Electronics based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $29.0, and the most bearish reporting a price target of just $20.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.4 billion, earnings will come to $61.6 million, and it would be trading on a PE ratio of 12.9x, assuming you use a discount rate of 8.3%.

- Given the current share price of $18.55, the analyst's price target of $24.0 is 22.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives