Key Takeaways

- Strategic inventory, supplier diversity, and early IoT investments position Avnet for outsized market share and elevated profit margins as industry demand accelerates.

- Strengthening order activity and operational execution at Farnell support faster margin recovery, driving consolidated earnings and long-term revenue outperformance amid rising industry complexity.

- Increasing supply chain risks, weak Western market demand, and direct manufacturer distribution threaten Avnet's revenue growth, value proposition, and long-term profitability.

Catalysts

About Avnet- Distributes electronic component technology.

- Analyst consensus expects inventory optimization to modestly improve efficiency and meet demand, but the potential for Avnet to leverage its strategic inventory positions and diverse supplier base could enable it to capture outsized market share during the next industry upcycle, positioning the company for an accelerated rebound in sales growth and higher gross margins as supply tightness returns globally.

- While analysts broadly agree Farnell's gradual execution should translate to incrementally better margins, the current sequential growth in operating income and early evidence of improving order activity across all regions point to a faster-than-expected return to double-digit margins at Farnell, which would drive a material uplift in Avnet's consolidated earnings power.

- The ongoing transformation toward IoT, edge computing, and industry automation is set to create a step-change in component and solutions demand, and Avnet's early investments in higher-margin IoT platforms and design services position it for structurally higher revenue growth and recurring revenue streams over the coming years, fundamentally changing the net margin profile of the company.

- Industry consolidation and heightened supply chain complexity-especially as regulatory and ESG requirements rise-pave the way for Avnet to capture a larger share of wallet from OEMs/EMS by offering unmatched scale, compliance, and secure distribution, laying the groundwork for sustained top-line outperformance and higher long-term profitability versus peers.

- The acceleration in end-markets like electric vehicles, renewables, and AI hardware, combined with Avnet's global logistics and deep supplier relationships, will enable the company to rapidly scale with new, secular demand waves, supporting structurally higher revenue run-rates and resilient earnings even through cyclical downturns.

Avnet Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Avnet compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

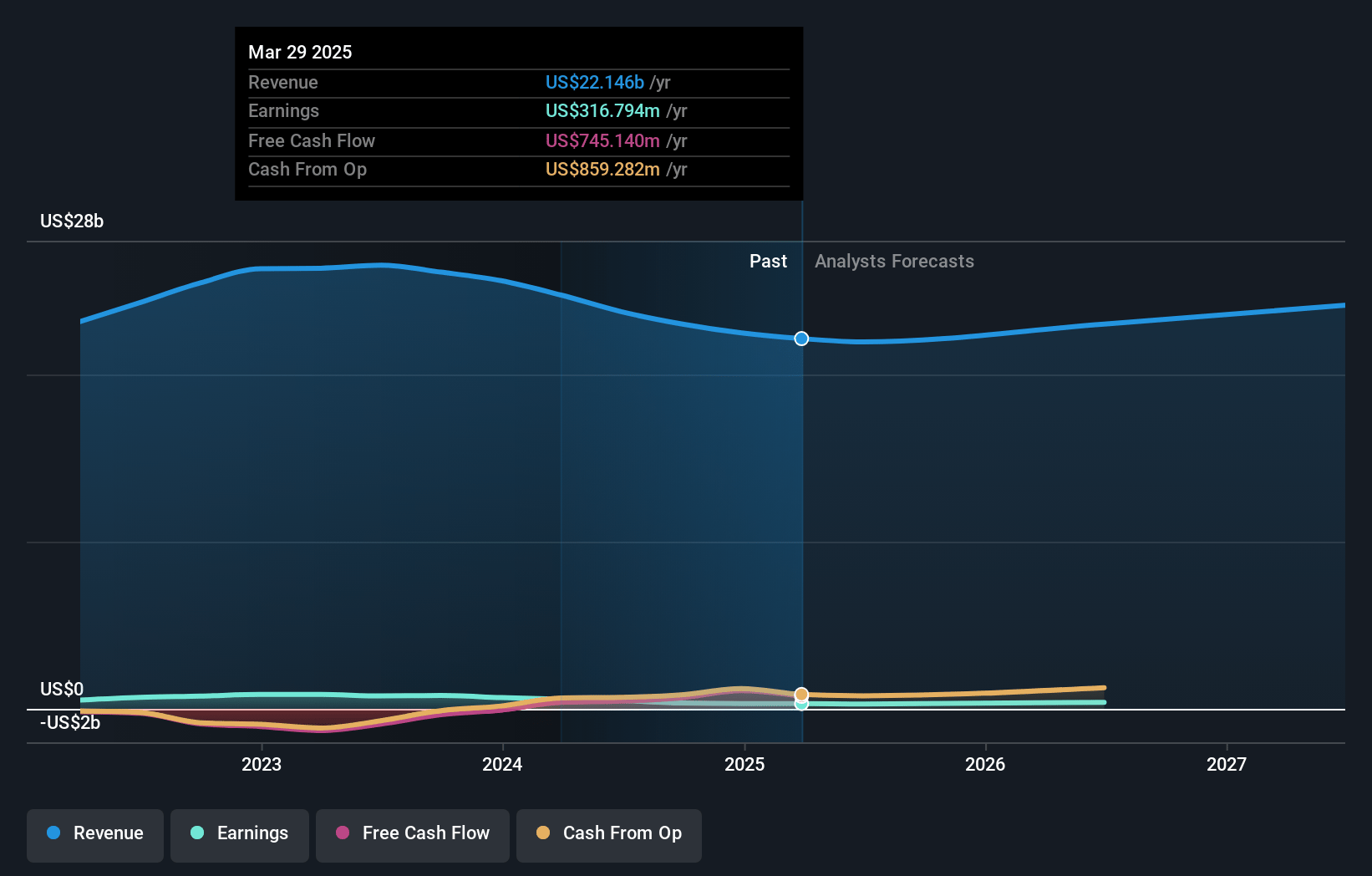

- The bullish analysts are assuming Avnet's revenue will grow by 4.3% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 1.4% today to 2.7% in 3 years time.

- The bullish analysts expect earnings to reach $666.2 million (and earnings per share of $7.96) by about July 2028, up from $316.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 9.0x on those 2028 earnings, down from 14.6x today. This future PE is lower than the current PE for the US Electronic industry at 23.8x.

- Analysts expect the number of shares outstanding to decline by 4.83% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.16%, as per the Simply Wall St company report.

Avnet Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Rising geopolitical tensions and newly enacted tariffs, particularly between the US and China, create ongoing supply chain volatility and increase operational complexity, which could pressure Avnet's revenues and margins if cost mitigation strategies prove insufficient.

- Persistent weakness in mature Western markets, particularly in EMEA where sales declined 24% year-over-year, signals a shrinking addressable market and limited topline growth, directly threatening Avnet's long-term revenue trajectory.

- Intensifying customer destocking and shorter lead times have resulted in lower backlog and reduced inventory turnover, which, if prolonged, may challenge Avnet's ability to drive sustainable revenue and profit recovery in the face of weak demand.

- The accelerating trend of direct-to-manufacturer distribution and vertical integration by large OEMs and EMS companies threatens to bypass traditional distributors like Avnet, risking ongoing erosion of Avnet's value proposition and future revenue streams.

- Margin compression remains a long-term risk, as Avnet faces fierce competition from global distributors and limited success in developing high-margin proprietary offerings, which may constrain net earnings and future profitability growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Avnet is $64.0, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Avnet's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $64.0, and the most bearish reporting a price target of just $43.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $25.1 billion, earnings will come to $666.2 million, and it would be trading on a PE ratio of 9.0x, assuming you use a discount rate of 9.2%.

- Given the current share price of $55.03, the bullish analyst price target of $64.0 is 14.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.