Key Takeaways

- Discontinuation of deep discounts may impact member retention and revenue stability, as price adjustments risk alienating existing customers.

- Dependence on government partnerships and processes could slow execution and delay expected revenue benefits in airport technology enhancements.

- CLEAR's focus on travel and identity services, government partnerships, and operational efficiencies is expected to drive revenue growth and margin expansion.

Catalysts

About Clear Secure- Operates a secure identity platform under the CLEAR brand name primarily in the United States.

- The company faces uneven net adds distribution in 2025 due to historical airport openings, promotions, partnerships, and credit card launches, potentially causing fluctuations in quarterly revenue and making sustained growth difficult.

- As Clear transitions away from early deep discount programs, they aim to boost unit economics through price adjustments, which risks alienating existing customers, potentially impacting member retention and revenue stability.

- Clear's expiration of their current credit card partnership poses a risk; as the gap between wholesale and retail pricing becomes significant, a potential renegotiation or lapse could depress total bookings and EBITDA without a suitable partner.

- The ambitious expansion of TSA PreCheck and CLEAR1, while contributing to growth, requires significant upfront investment and may not instantaneously translate into increased gross profit, affecting short-term operating margins.

- While the company is optimistic about strategic public-private partnerships and airport technology enhancements, reliance on government cooperation and bureaucratic processes may slow execution timelines, delaying anticipated revenue and margin benefits.

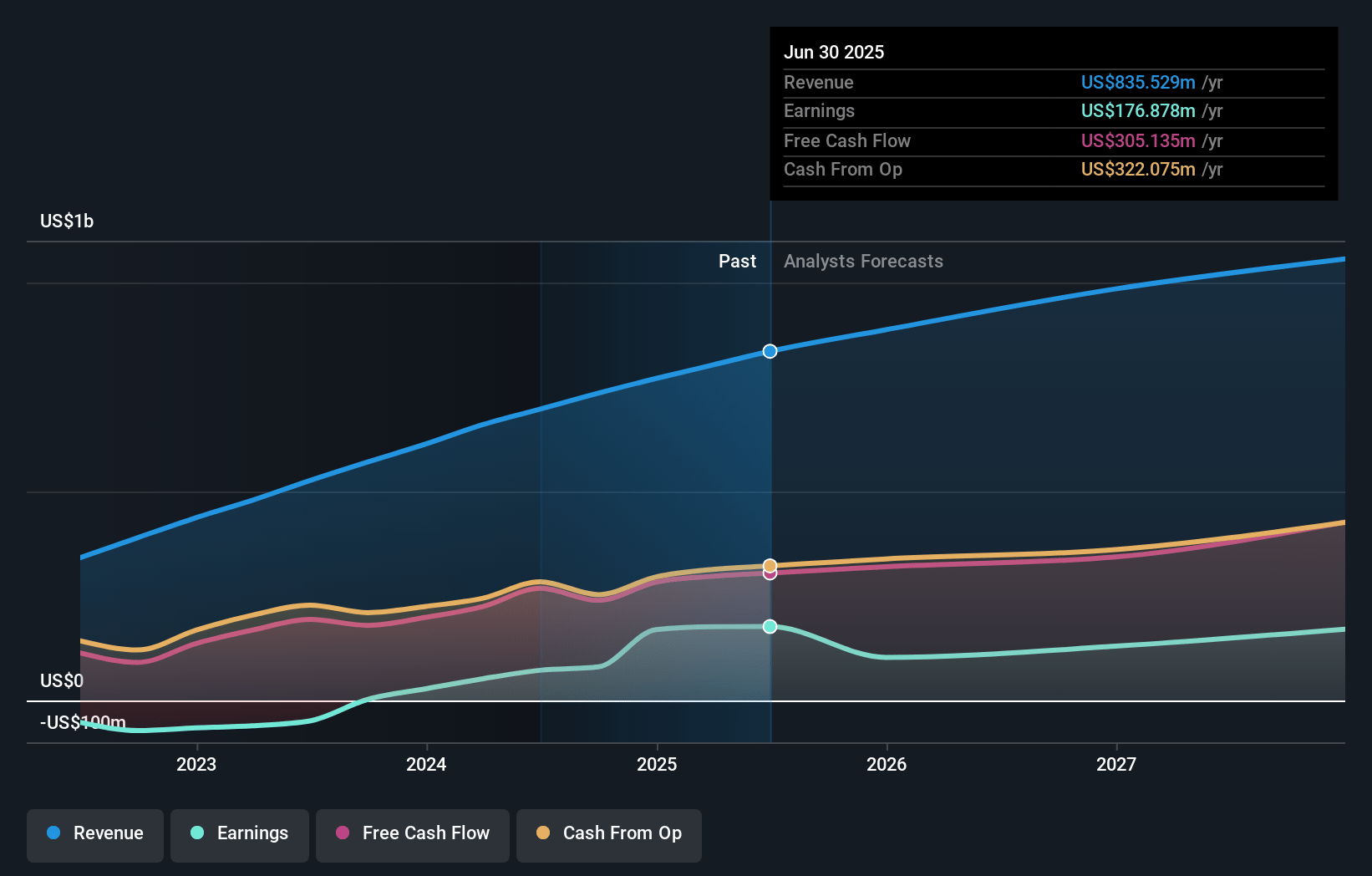

Clear Secure Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Clear Secure compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Clear Secure's revenue will grow by 8.6% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 22.0% today to 14.9% in 3 years time.

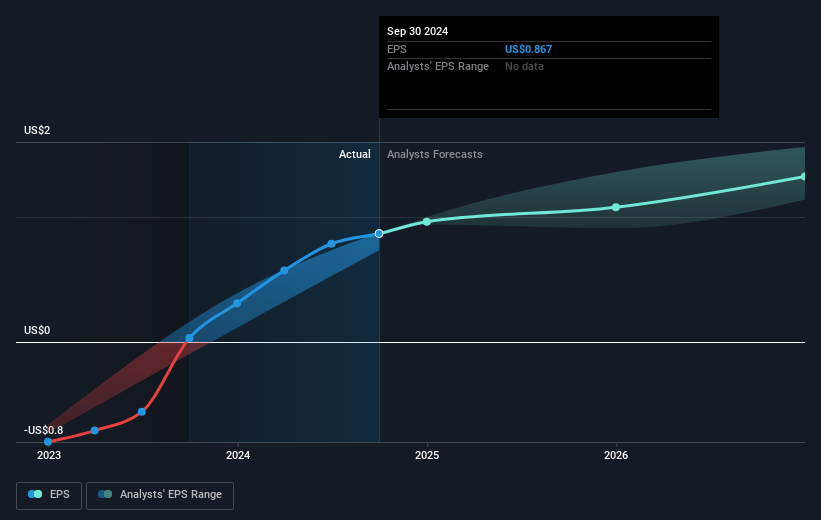

- The bearish analysts expect earnings to reach $153.5 million (and earnings per share of $1.48) by about July 2028, down from $176.3 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 24.9x on those 2028 earnings, up from 16.2x today. This future PE is lower than the current PE for the US Software industry at 42.7x.

- Analysts expect the number of shares outstanding to decline by 0.23% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.96%, as per the Simply Wall St company report.

Clear Secure Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- CLEAR is expecting strong top-line growth driven by both its travel services and identity solutions, which are likely to positively impact revenue and margin expansion in the coming years.

- The successful rollout and customer approval of new technologies like EnVe's and eGates are expected to improve operational efficiencies and customer satisfaction, potentially increasing revenue and operating margins.

- Engagement with the U.S. government and a focus on public-private partnerships to enhance airport infrastructure could open up new revenue streams and improve profitability as CLEAR positions itself as a leader in this sector.

- CLEAR's efforts to increase its TSA PreCheck and identity platform offerings, including through new enrollment locations, signal potential revenue growth opportunities and improved profitability through expanded service reach.

- The company anticipates free cash flow of at least 310 million dollars in 2025, aided by strong operational execution and growing demand for its services, which could contribute to a stronger financial position and shareholder value.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Clear Secure is $23.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Clear Secure's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $45.0, and the most bearish reporting a price target of just $23.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $1.0 billion, earnings will come to $153.5 million, and it would be trading on a PE ratio of 24.9x, assuming you use a discount rate of 8.0%.

- Given the current share price of $30.8, the bearish analyst price target of $23.0 is 33.9% lower.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.