Narratives are currently in beta

Key Takeaways

- Accelerated sales hiring and CRM system upgrades aim to capture market opportunities, boost productivity, and support revenue and margin growth.

- The strong growth in contract and new business value, along with share repurchases, enhances revenue potential and supports improved shareholder returns.

- Reliance on financially challenged small vendors and variability in consulting business may impact Gartner's revenue growth and earnings stability.

Catalysts

About Gartner- Operates as a research and advisory company in the United States, Canada, Europe, the Middle East, Africa, and internationally.

- Gartner's accelerated hiring of sales headcount in the second half of 2024, expected to continue into 2025 and beyond, is set to capture large untapped market opportunities, likely impacting future revenue growth positively.

- Growth in contract value with enterprise function leaders at 9% and new business growth in Global Business Sales (GBS) at 10% indicates strong underlying demand, supporting higher revenue generation in future periods.

- The rebound in tech vendor contracts, with new business growth returning to historical norms, suggests potential for accelerated contract value growth, which could translate to improved revenue streams.

- Implementation of a state-of-the-art CRM system and enhancements in sales training are expected to boost sales productivity, supporting margin improvements and earnings growth.

- Continuation of a disciplined share repurchase program, with more than $1 billion authorization remaining, is anticipated to be accretive to earnings per share, enhancing shareholder returns and potentially driving EPS growth.

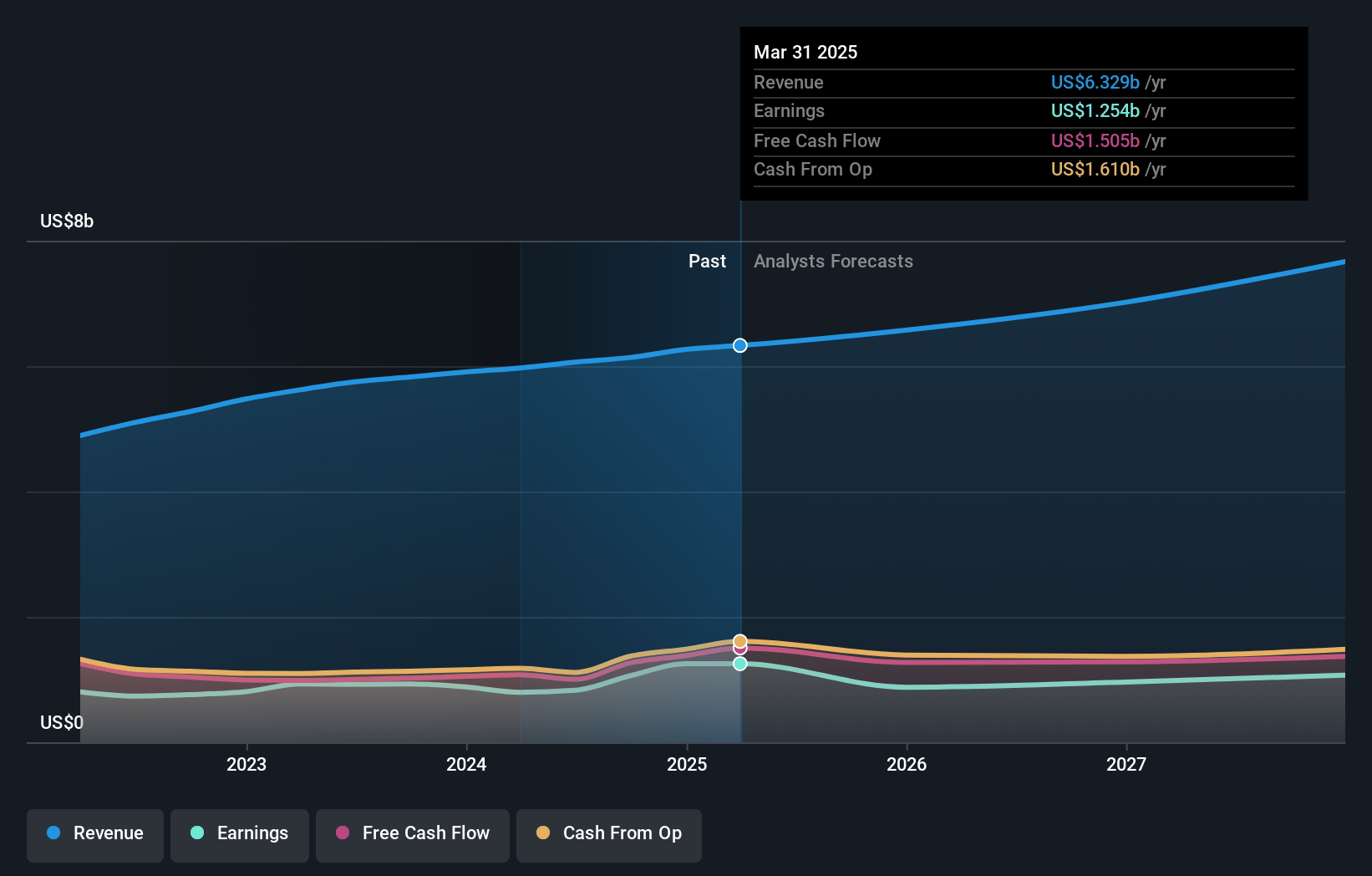

Gartner Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Gartner's revenue will grow by 9.3% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 17.3% today to 15.0% in 3 years time.

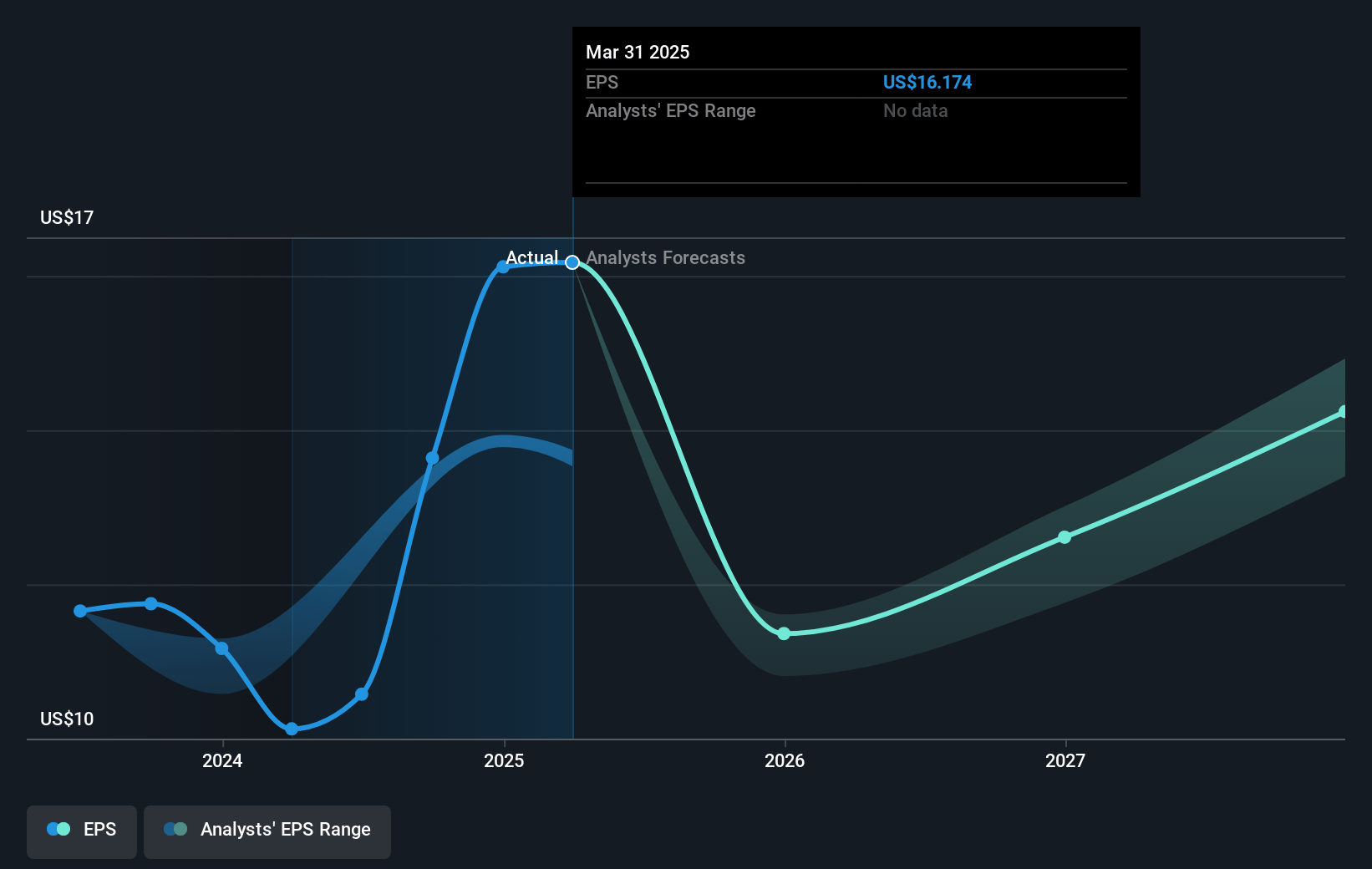

- Analysts expect earnings to reach $1.2 billion (and earnings per share of $16.15) by about December 2027, up from $1.1 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 41.8x on those 2027 earnings, up from 35.5x today. This future PE is greater than the current PE for the US IT industry at 41.2x.

- Analysts expect the number of shares outstanding to decline by 1.21% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.53%, as per the Simply Wall St company report.

Gartner Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Gartner's reliance on small tech vendors, which are experiencing financial challenges, could impact growth, as these vendors may renew contracts at lower rates, potentially affecting future revenues and earnings.

- Variability in Gartner’s consulting business, particularly in contract optimization, which depends on client deal closures, can cause fluctuations in quarterly results and impact overall earnings stability.

- The decline in nonsubscription research revenue suggests potential softness in these areas, which could limit revenue growth if this trend continues.

- Marketing and sales, a part of GBS with higher legacy CV, face economic scrutiny and slower renewals, which might affect GBS contract value growth and future revenue.

- The ramp-up time for new sales employees, taking about three years to reach full productivity, might delay expected improvements in sales growth and related revenue increases.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $545.01 for Gartner based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $592.0, and the most bearish reporting a price target of just $470.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $8.0 billion, earnings will come to $1.2 billion, and it would be trading on a PE ratio of 41.8x, assuming you use a discount rate of 7.5%.

- Given the current share price of $489.96, the analyst's price target of $545.01 is 10.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives