Key Takeaways

- MongoDB's focus on AI capabilities and app modernization aims to expand revenue streams and improve long-term earnings.

- Strong new workload acquisitions and Atlas's stable growth are expected to sustain revenue and leverage competitive advantages.

- Strategic initiatives and AI integration may not significantly boost revenue in fiscal '26, with headwinds from non-Atlas business and seasonal Atlas volatility impacting growth.

Catalysts

About MongoDB- Provides general purpose database platform worldwide.

- MongoDB anticipates strong new workload acquisition in fiscal '26, driven by the trend of companies building competitive advantages through custom-built software on MongoDB, which could positively impact revenue growth.

- The company expects stable consumption growth for Atlas, maintaining consistency with recent quarters, supported by an improved fiscal '25 workload cohort, which is likely to sustain revenue growth.

- With the rise of AI, MongoDB foresees gradual but incremental contributions to revenue growth as enterprises develop competencies in leveraging AI, impacting both revenue and future net margins.

- MongoDB is investing heavily in AI and expanding its app modernization efforts, targeting significant revenue opportunities in modernizing legacy applications starting in fiscal '27, which should expand their revenue streams and potentially improve long-term earnings.

- The acquisition of Voyage AI is aimed at enhancing MongoDB's capabilities in AI, providing high-quality and trustworthy AI applications, which could drive Atlas’s contribution to revenue growth as the database redefines its role in the AI era.

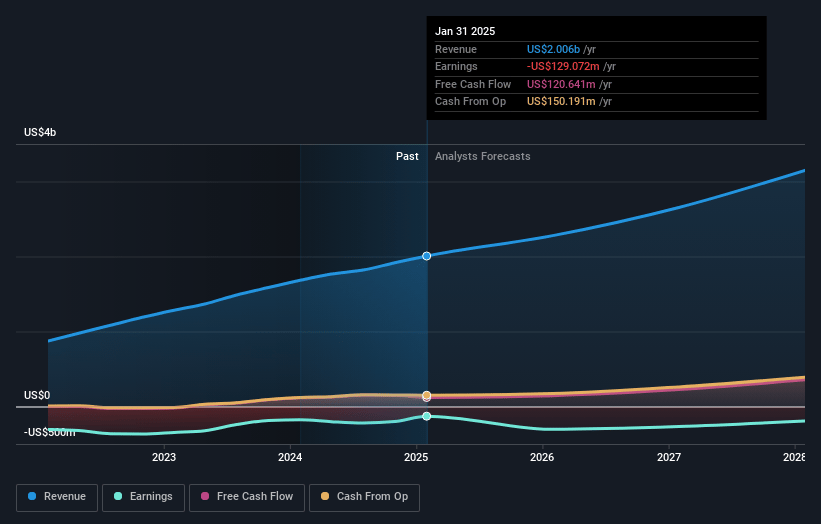

MongoDB Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming MongoDB's revenue will grow by 15.9% annually over the next 3 years.

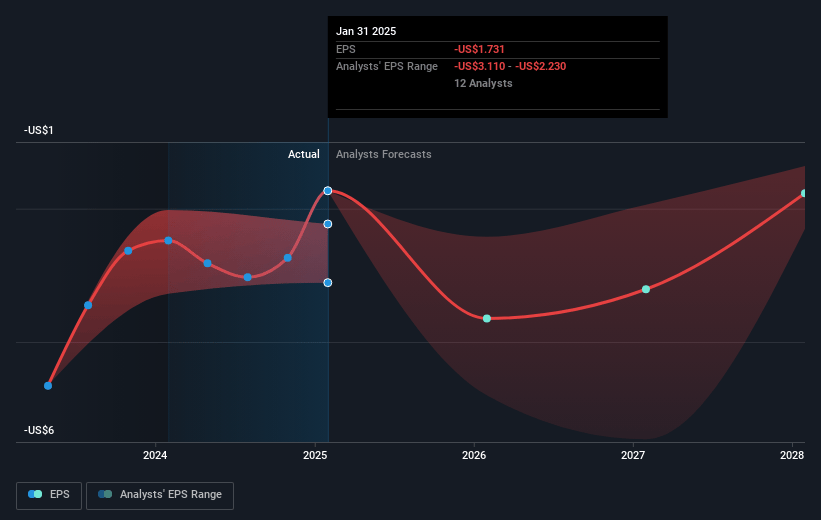

- Analysts are not forecasting that MongoDB will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate MongoDB's profit margin will increase from -6.4% to the average US IT industry of 7.9% in 3 years.

- If MongoDB's profit margin were to converge on the industry average, you could expect earnings to reach $248.0 million (and earnings per share of $2.5) by about May 2028, up from $-129.1 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 132.3x on those 2028 earnings, up from -109.9x today. This future PE is greater than the current PE for the US IT industry at 31.0x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.87%, as per the Simply Wall St company report.

MongoDB Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The non-Atlas business is expected to be a significant headwind to growth in fiscal '26, with a projected high single-digit decline due to fewer multiyear deals and non-Atlas customers deploying more incremental workloads on Atlas, impacting revenue patterns.

- The transition to AI applications is anticipated to be gradual, with most enterprise customers still developing in-house skills, suggesting that benefits from AI will only modestly contribute to revenue growth in fiscal '26.

- The acquisition of Voyage AI, while promising, is expected to be only modestly dilutive to operating margins for the year as it will take time to integrate and materialize in terms of revenue impact.

- Seasonality and volatility in Atlas consumption, particularly slower growth around holiday periods, could affect Atlas revenue growth, challenging MongoDB’s ability to show stable financial performance.

- The transition year for strategic initiatives, like AI and app modernization, may not yield immediate revenue acceleration, posing a risk to sustaining current growth rates beyond fiscal '26.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $264.107 for MongoDB based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $430.0, and the most bearish reporting a price target of just $160.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $3.1 billion, earnings will come to $248.0 million, and it would be trading on a PE ratio of 132.3x, assuming you use a discount rate of 7.9%.

- Given the current share price of $174.69, the analyst price target of $264.11 is 33.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.