Last Update 24 Jun 26

III: AI Research Expansion And Buybacks Will Support Future Upside

Analysts have maintained their $6.67 price target on Information Services Group, citing only minor model adjustments, including a slightly higher discount rate and small tweaks to long term revenue growth, profit margin, and future P/E assumptions.

What’s in the News for Information Services Group

- Information Services Group announced a new ISG AI Index that tracks how AI is affecting the global technology and business services sector, including infrastructure as a service, software as a service and managed services, using revenue, profitability, stock performance and segment specific AI indicators as inputs (source: ISG AI Index launch).

- The company provided earnings guidance for the second quarter of 2026, targeting revenues between $62.5 million and $63.5 million (source: corporate guidance).

- From January 1, 2026 to March 31, 2026, Information Services Group repurchased 268,000 shares for $2.09 million, bringing total buybacks under the August 3, 2023 program to 4,983,475 shares for $21.17 million (source: share repurchase update).

- Information Services Group launched multiple ISG Provider Lens research studies focused on generative AI services, advanced analytics and AI services, and AI enabled cloud and multicloud offerings. The firm surveyed hundreds of providers across these areas for reports scheduled through late 2026 (sources: Generative AI Services, Advanced Analytics and AI Services, Multi Public Cloud Services, AWS Ecosystem Partners announcements).

- The company also initiated sector specific research programs covering manufacturing, life sciences, medical devices, automotive and mobility, public sector services, HR outsourcing, enterprise service management and several SaaS ecosystems such as Workday, UKG Pro and Guidewire. Findings from these programs are expected to appear in a series of ISG Provider Lens reports during 2026 (sources: Manufacturing Industry Services and Solutions, AI Services in Life Sciences, Medical Device Digital Services, Automotive and Mobility Services and Solutions, Public Sector Services and Solutions, HR Outsourcing, Enterprise Service Management, Workday, UKG Pro and Guidewire ecosystem announcements).

Valuation Changes

- Fair Value: The $6.67 fair value estimate for Information Services Group is unchanged, indicating no revision to the overall valuation outcome.

- Discount Rate: The discount rate has risen slightly from 9.60% to 9.80%, reflecting a modest adjustment to the risk or return expectations used in the valuation model.

- Revenue Growth: The long term revenue growth assumption is essentially unchanged at about 4.29%, with only an immaterial numerical refinement.

- Net Profit Margin: The long term profit margin assumption remains effectively flat at about 6.12%, with only a very small model adjustment.

- Future P/E: The future P/E multiple has risen slightly from 23.61x to 23.74x, indicating a small change in the valuation multiple applied to Information Services Group’s projected earnings.

Key Takeaways

- Expanding demand for AI and digital transformation services is boosting ISG's revenue growth, while recurring revenues and acquisitions improve earnings quality and geographic reach.

- Growing need for specialized advisory due to regulatory and technological complexity enhances ISG's competitive position and supports stable, higher-margin performance.

- Rising automation, client insourcing, and intensifying competition threaten ISG's revenue, margins, and scalability as demand for traditional advisory services becomes less predictable and more commoditized.

Catalysts

About Information Services Group- Operates as an artificial intelligence (AI) centered technology research and advisory company in the Americas, Europe, and the Asia Pacific.

- Accelerating enterprise investment in AI and digital transformation-driven by the ongoing modernization of IT infrastructure and operations-continues to expand the addressable market for advisory firms like ISG, as seen by surging AI-related revenues and expanding client interest, which is likely to fuel strong top-line revenue growth.

- ISG's increasing penetration into the mid-market via its ISG Tango platform, alongside growth in recurring revenue streams (now 45% of total revenue), is creating more stable, higher-margin revenue sources and is poised to improve net margins and earnings quality going forward.

- Strategic acquisitions, such as the recent purchase of Martino & Partners to grow the European public sector business and deepen service offerings beyond central to municipal government clients, are expanding ISG's client base and geographic reach, representing future catalysts for both revenue and EBITDA growth.

- Clients' ongoing need to optimize technology spend amid economic uncertainty, cost pressures, and the shift toward cloud and AI is sustaining strong demand for ISG's core sourcing, benchmarking, and advisory services-positioning the company to benefit from long-term, resilient demand that supports consistent revenue growth.

- The rising complexity of AI, multi-vendor sourcing, and increasing regulatory scrutiny means enterprises require specialized, independent expertise, enhancing the competitive positioning and pricing power of firms like ISG and supporting sustained expansion in net margins.

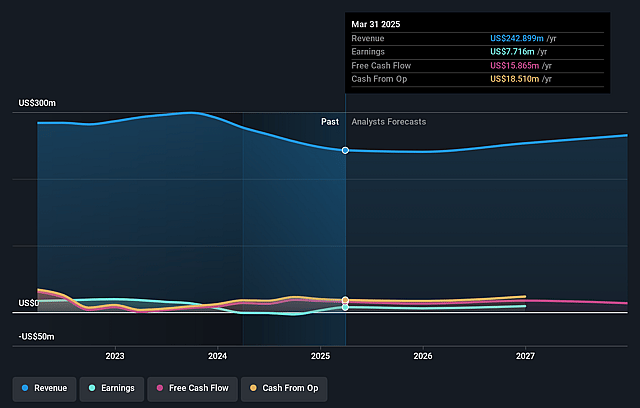

Information Services Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Information Services Group's revenue will grow by 4.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.3% today to 6.1% in 3 years time.

- Analysts expect earnings to reach $17.1 million (and earnings per share of $0.32) by about June 2029, up from $10.6 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $23.6 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 24.1x on those 2029 earnings, up from 18.2x today. This future PE is greater than the current PE for the US IT industry at 16.1x.

- Analysts expect the number of shares outstanding to decline by 0.74% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.8%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The rapid maturation of AI and automation technologies could commoditize many advisory services currently offered by ISG, leading clients to use digital tools or in-house solutions instead, thereby suppressing long-term revenue growth and potentially compressing margins.

- Larger enterprises are focusing on building in-house AI, IT strategy, and benchmarking expertise in order to retain control and cut external consulting costs, which threatens ISG's addressable market and can negatively impact revenues and client retention rates.

- Despite near-term momentum, European markets remain cautious and subject to macroeconomic and geopolitical uncertainties, which could delay or cancel large transformation projects and result in more cyclical and unpredictable revenues for ISG.

- Increased competition from major consulting and technology firms expanding their end-to-end digital transformation offerings may outcompete ISG's more focused, niche portfolio, putting pressure on market share and pricing, thus impacting revenue growth and profit margins.

- ISG's business model remains heavily reliant on recurring but human-capital-intensive services, and limited operational leverage may restrict the scalability of earnings, particularly if technology-driven clients increasingly adopt DIY benchmarking tools or more fully automated solutions, pressuring both revenues and net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $6.67 for Information Services Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $8.0, and the most bearish reporting a price target of just $5.5.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $279.4 million, earnings will come to $17.1 million, and it would be trading on a PE ratio of 24.1x, assuming you use a discount rate of 9.8%.

- Given the current share price of $4.01, the analyst price target of $6.67 is 39.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Information Services Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.