Narratives are currently in beta

Key Takeaways

- Strategic acquisitions and cloud partnerships enhance offerings and fuel customer acquisition, potentially boosting revenue and increasing operating expenses.

- Focus on cyber resilience and compliance solutions aligns with emerging regulations, creating upselling opportunities and impacting revenue and margins.

- Commvault's strong revenue growth, SaaS expansion, strategic cloud partnerships, and share repurchase strategy bolster its potential for increased earnings and market competitiveness.

Catalysts

About Commvault Systems- Provides a platform that enhances cyber resiliency by protecting the data in the United States and internationally.

- The surge in demand for cloud-first and multi-cloud resilience solutions, as enterprises transition their infrastructure to cloud environments, positions Commvault well to grow its subscription and SaaS revenues significantly in upcoming years. This prediction influences revenue growth expectations.

- Commvault's strategic acquisitions, such as Appranix and Clumio, are set to enhance its product offerings and integration capabilities, potentially leading to higher operating expenses but also potentially boosting revenue and ARR if the features drive customer acquisition and retention, impacting net earnings positively in the longer term.

- The company's robust partnerships with major cloud providers like AWS and Google Cloud could fuel cross-selling opportunities and drive new customer acquisition, expected to contribute positively to subscription revenue growth.

- Expansion of unique offerings such as Cloud Rewind aims to simplify cloud recovery processes, potentially increasing customer adoption and reliance on Commvault's solutions, thereby improving ARR and boosting revenue streams.

- The focus on cyber resilience and strategic compliance solutions, in light of emerging regulations like the EU's DORA, creates opportunities for upselling and expanding within existing and new customer bases, potentially impacting both revenue and net margins as customers seek comprehensive data protection solutions.

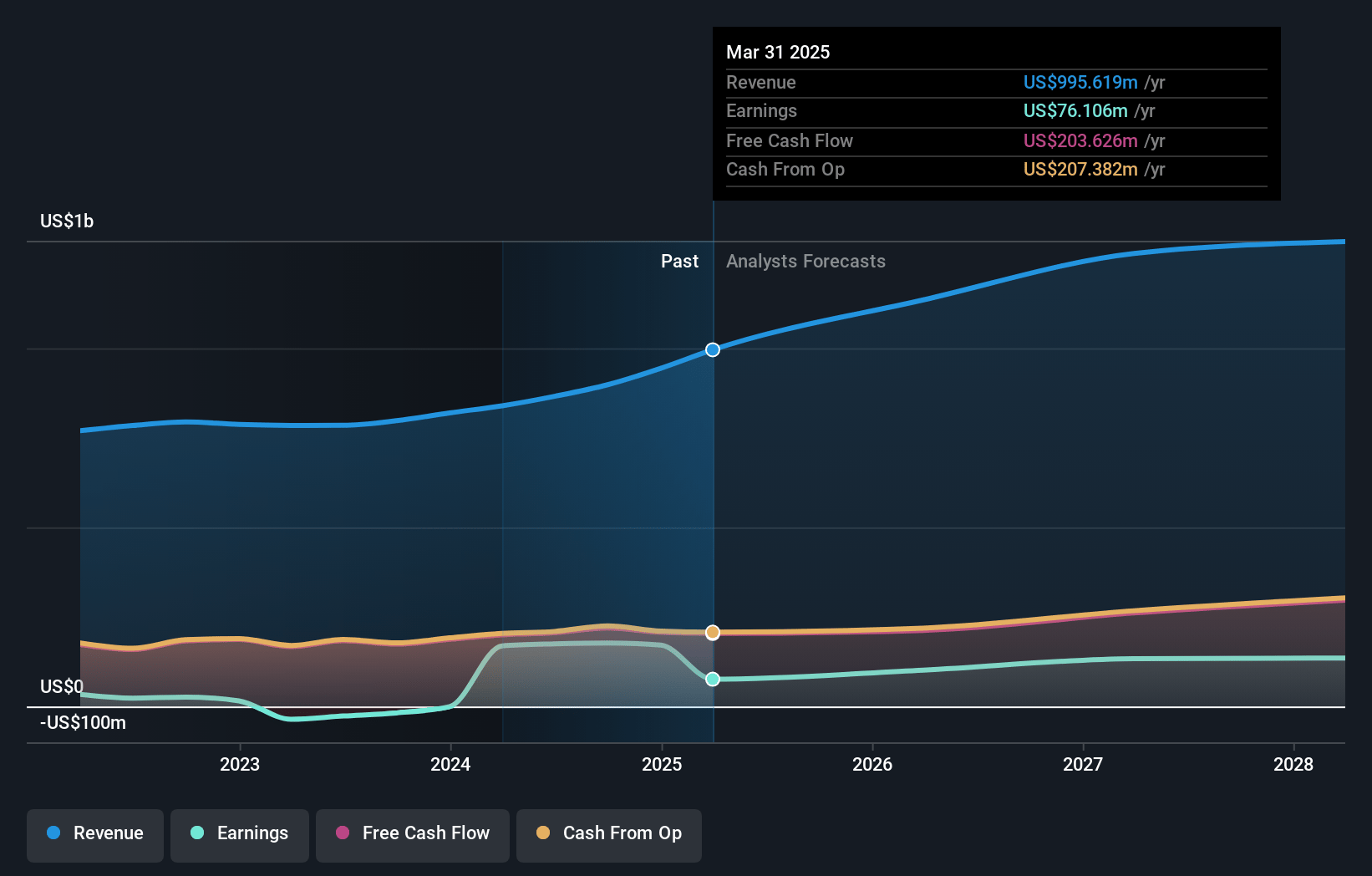

Commvault Systems Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Commvault Systems's revenue will grow by 11.0% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 19.7% today to 7.4% in 3 years time.

- Analysts expect earnings to reach $90.8 million (and earnings per share of $2.68) by about December 2027, down from $177.4 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 77.5x on those 2027 earnings, up from 41.0x today. This future PE is greater than the current PE for the US Software industry at 42.0x.

- Analysts expect the number of shares outstanding to decline by 8.15% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.95%, as per the Simply Wall St company report.

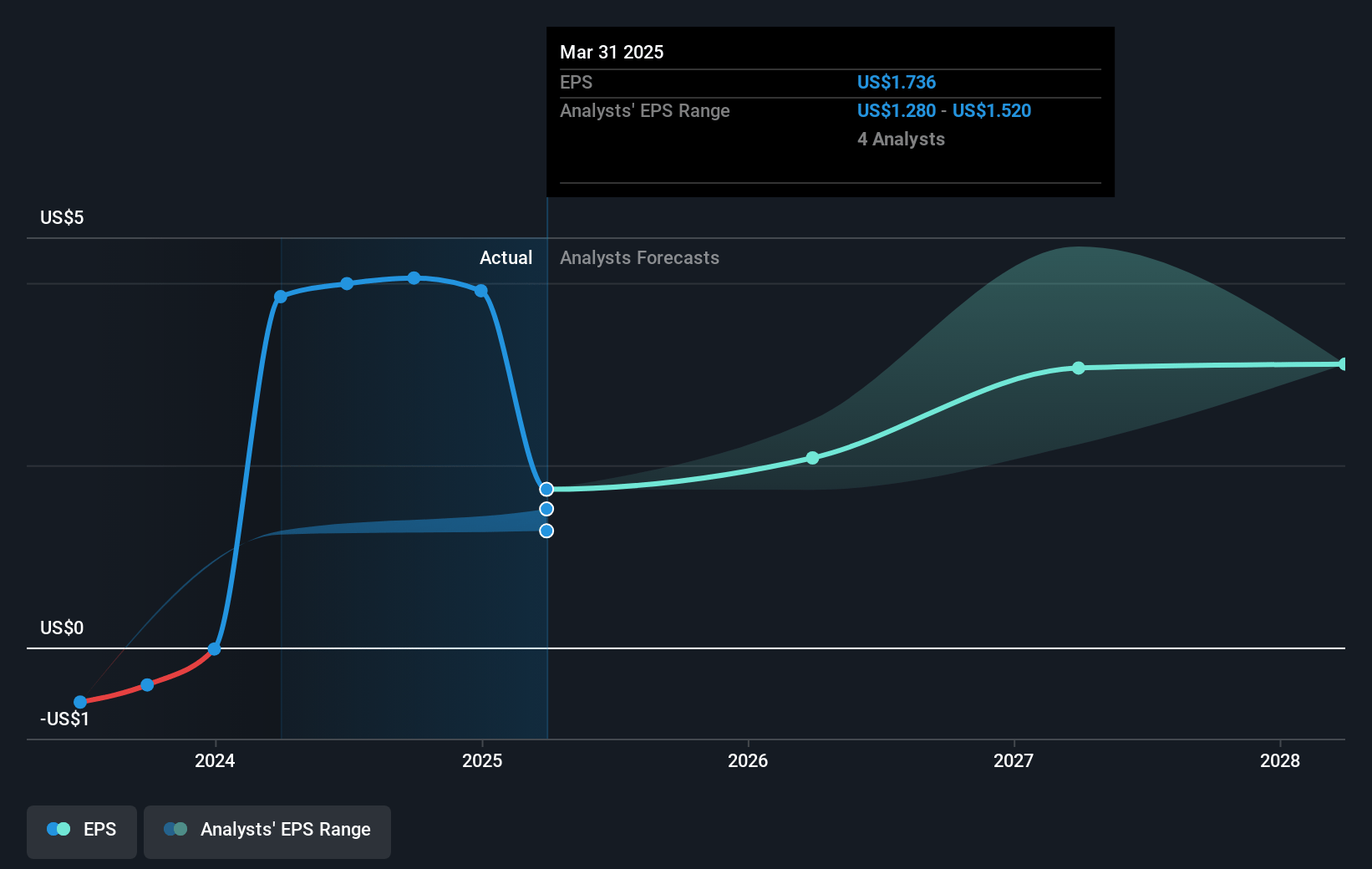

Commvault Systems Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Commvault reported a fourth consecutive quarter of double-digit revenue growth, with total revenue increasing 16% and total ARR accelerating 20%, indicating strong demand for its services which could positively impact revenue.

- The company's SaaS ARR jumped 64% and now represents 25% of total ARR, showing significant growth in its SaaS offerings and potential for increased recurring revenue and net margins.

- Commvault introduced innovative cloud recovery solutions like Commvault Cloud Rewind and formed strategic partnerships with major cloud providers like AWS and Google Cloud, enhancing its competitiveness and potential for future earnings growth.

- Encouraging existing customer expansion with a Q2 SaaS net dollar retention rate of 127% suggests strong customer satisfaction and the ability to cross-sell and upsell additional services, supporting revenue and net margins.

- A commitment to return 75% of free cash flow through share repurchases reflects confidence in cash flow generation, possibly stabilizing or enhancing earnings per share.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $174.2 for Commvault Systems based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $200.0, and the most bearish reporting a price target of just $144.2.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $1.2 billion, earnings will come to $90.8 million, and it would be trading on a PE ratio of 77.5x, assuming you use a discount rate of 7.0%.

- Given the current share price of $166.44, the analyst's price target of $174.2 is 4.5% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives