Key Takeaways

- Strategic partnerships and new products enhance Confluent's market reach and customer adoption, potentially boosting revenue and solidifying its leadership in data streaming.

- Transition to consumption-based selling and expanded offerings target diverse customer needs, driving potential revenue growth and improved margins.

- Confluent faces challenges in financial transparency, market competition, and execution risks, all potentially impacting investor confidence and future revenue growth.

Catalysts

About Confluent- Operates a data streaming platform in the United States and internationally.

- Confluent's strategic partnership with Databricks is expected to expand its market reach and enable its data streaming platform to integrate with real-time AI-driven analytics. This can lead to increased revenue as enterprises adopt Confluent's solutions to power sophisticated AI applications, enhancing its position as a leader in data streaming.

- The introduction of new products like Tableflow, which bridges operational and analytical systems, is set to drive substantial ROI for customers. This could lead to increased adoption and higher revenues as customers seek efficient data streaming solutions across their operations.

- The improved deployment options, including the expansion with offerings like freight clusters and WarpStream, are aimed at penetrating new accounts and addressing cost-sensitive workloads, potentially boosting revenue by attracting cost-conscious customers.

- The increased adoption of DSP components, such as Stream, Connect, Process, and Govern, which grew faster than the overall cloud business, suggests potential for revenue growth as these solutions become more integrated into customer use cases.

- The transition to consumption-based selling and focus on enabling DSP use cases are designed to accelerate revenue growth by driving customer adoption and expansion, potentially improving net margins as the company leverages its complete data streaming platform.

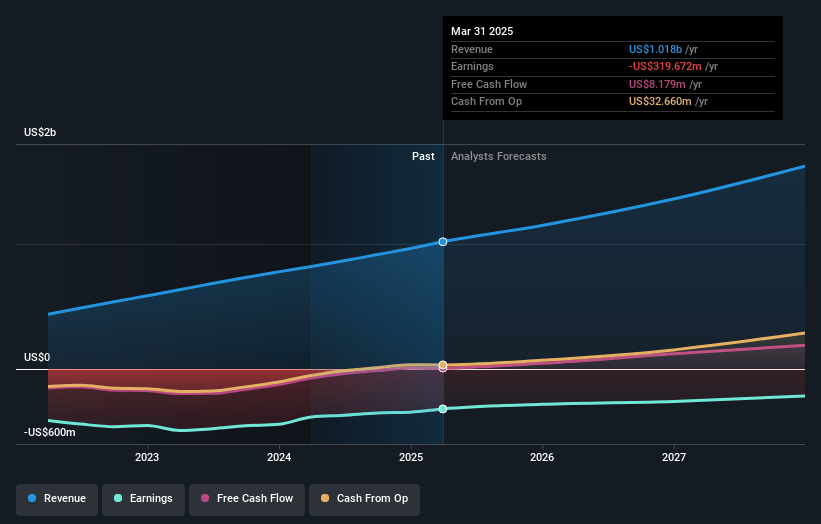

Confluent Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Confluent's revenue will grow by 20.8% annually over the next 3 years.

- Analysts are not forecasting that Confluent will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Confluent's profit margin will increase from -35.8% to the average US Software industry of 12.0% in 3 years.

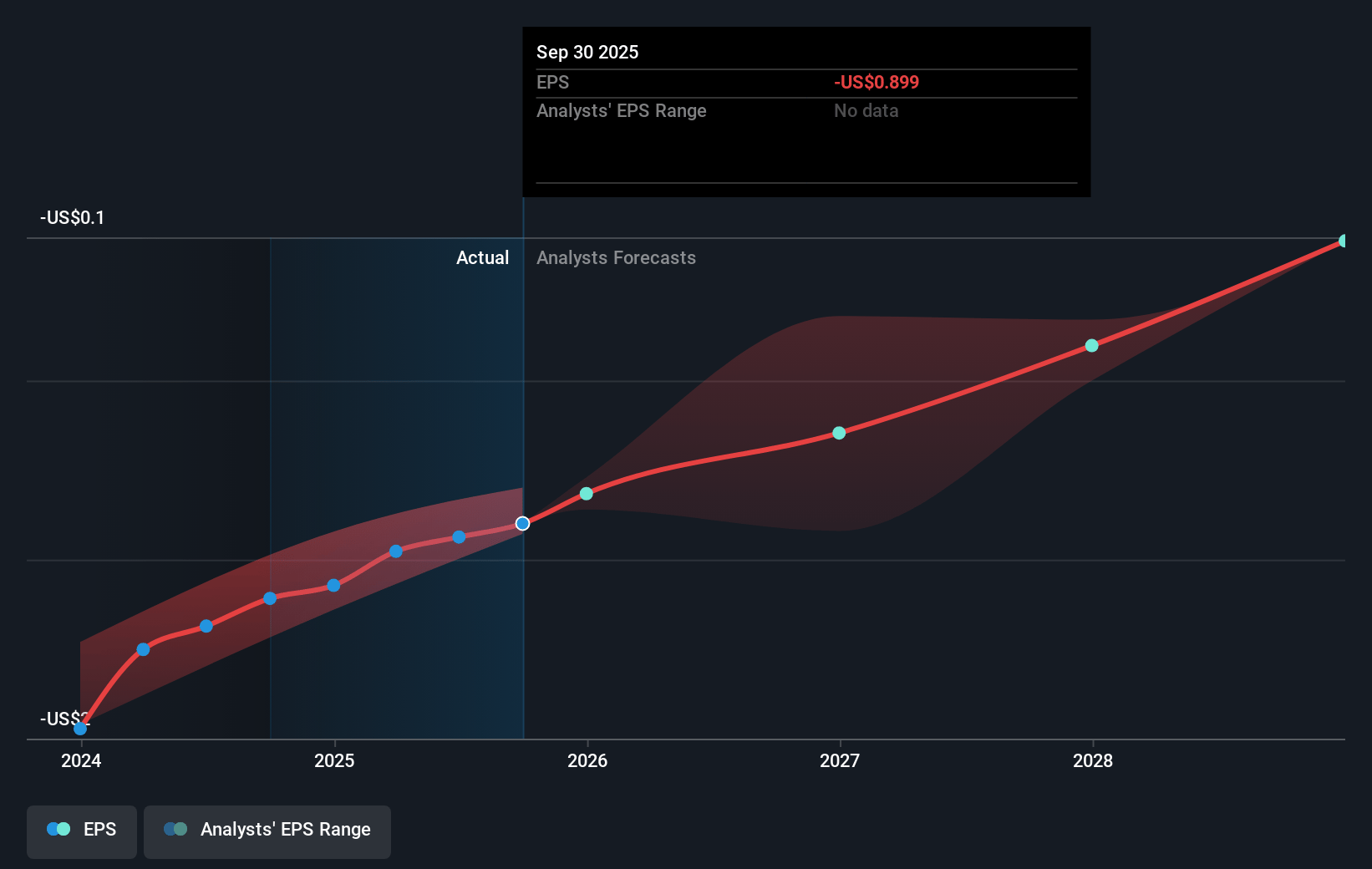

- If Confluent's profit margin were to converge on the industry average, you could expect earnings to reach $204.5 million (and earnings per share of $0.52) by about May 2028, up from $-345.1 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 81.3x on those 2028 earnings, up from -23.7x today. This future PE is greater than the current PE for the US Software industry at 31.6x.

- Analysts expect the number of shares outstanding to grow by 5.09% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.01%, as per the Simply Wall St company report.

Confluent Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's reliance on non-GAAP financial measures and reconciliations may obscure the true financial health of Confluent, potentially affecting investor confidence and impacting net margins and earnings.

- The increased competition, evidenced by Confluent's competitors like Snowflake potentially acquiring Redpanda, could put pressure on market share, affecting future revenue growth.

- The shift to a consumption-driven go-to-market model, while promising, may introduce variability in revenue, particularly if adoption rates are slower than expected, impacting subscription revenue predictability.

- The success of partnerships, such as with Databricks, is not guaranteed and depends on effective joint go-to-market strategies. Any failures here could impact revenue growth and customer acquisition.

- There is execution risk in scaling the adoption of their new products like Tableflow and WarpStream, where delays or integration challenges could impact customer satisfaction and future revenue streams.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $33.509 for Confluent based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $42.0, and the most bearish reporting a price target of just $22.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.7 billion, earnings will come to $204.5 million, and it would be trading on a PE ratio of 81.3x, assuming you use a discount rate of 8.0%.

- Given the current share price of $24.06, the analyst price target of $33.51 is 28.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.