Narratives are currently in beta

Key Takeaways

- Heavy investment in AI and event-driven architecture could drive revenue growth by enhancing claims processing efficiency and industry adoption.

- New AI solutions and product roll-outs aim to boost operational efficiencies, earnings potential, and recurring revenue through enhanced customer interactions and upsell opportunities.

- Slower product adoption and market pressures may delay revenue growth and challenge CCC's financial projections and operational efficiency in the near term.

Catalysts

About CCC Intelligent Solutions Holdings- Operates as a software as a service company for the property and casualty insurance economy in the United States and China.

- CCC is investing heavily in AI and event-driven architecture to enhance the efficiency and speed of claims processing, which is expected to drive future revenue growth as these solutions gain traction across the industry.

- The IX Cloud platform's interoperability with existing customer workflows could significantly boost customer adoption rates, thus potentially increasing CCC's revenue from cross-sell and upsell opportunities.

- CCC's continued focus on developing high-impact AI solutions for the P&C insurance economy, such as the First Look and Intelligent Reinspection tools, aims to deliver operational efficiencies and ROI for clients, which could, in turn, enhance margins and earnings over the long term.

- The roll-out of new products like Mobile Jumpstart and CCC Build Sheets represents fast-growing revenue segments, which signal growing earnings potential as adoption among repair facilities accelerates.

- Organizational changes to streamline customer interactions and focus on newer solutions may enhance the effectiveness of CCC's sales efforts, potentially translating to higher net dollar retention rates and an increase in recurring revenue streams.

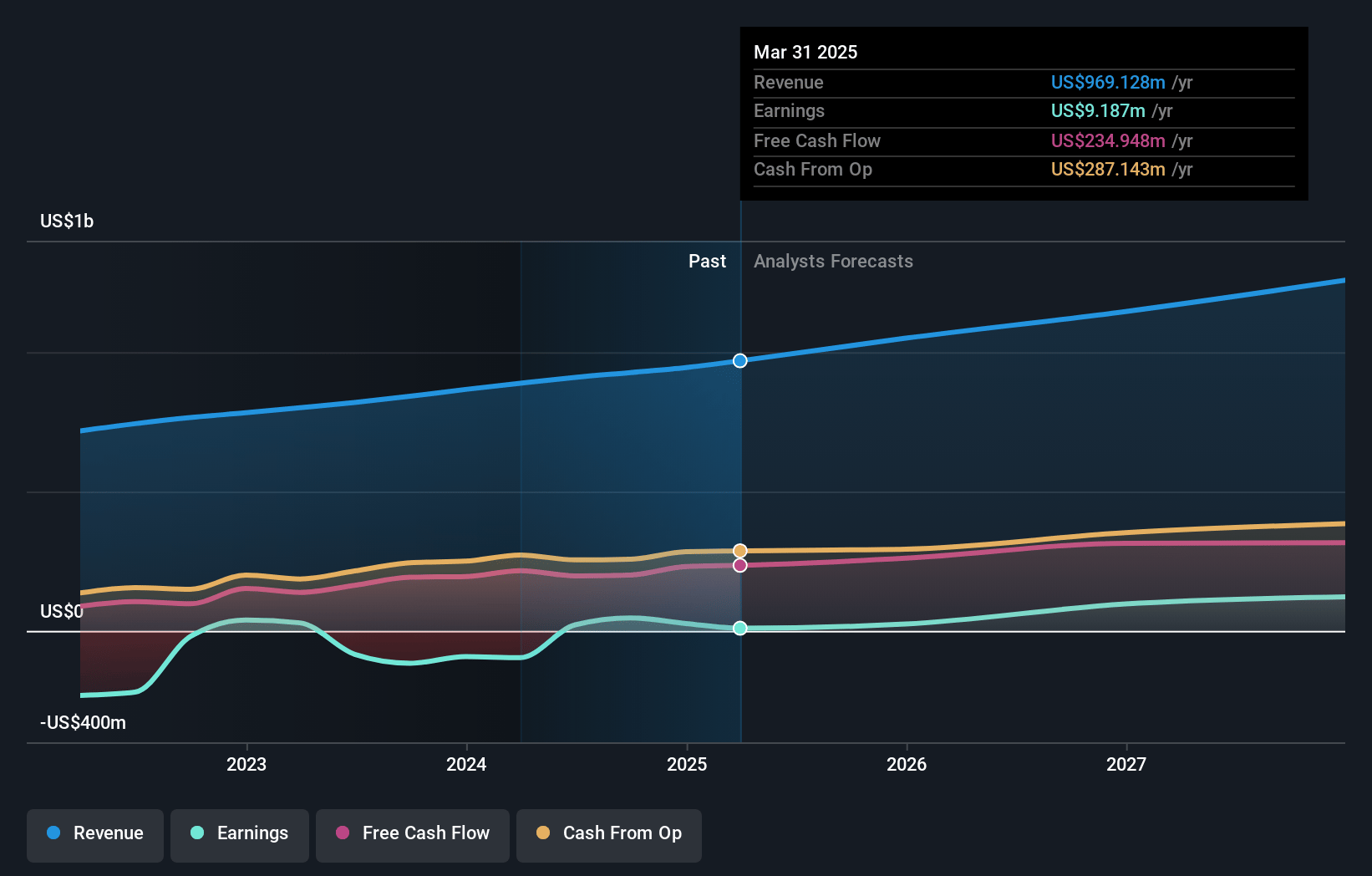

CCC Intelligent Solutions Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming CCC Intelligent Solutions Holdings's revenue will grow by 8.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.0% today to 11.4% in 3 years time.

- Analysts expect earnings to reach $136.7 million (and earnings per share of $0.19) by about January 2028, up from $46.5 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 87.9x on those 2028 earnings, down from 158.6x today. This future PE is greater than the current PE for the US Software industry at 43.6x.

- Analysts expect the number of shares outstanding to grow by 3.07% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.22%, as per the Simply Wall St company report.

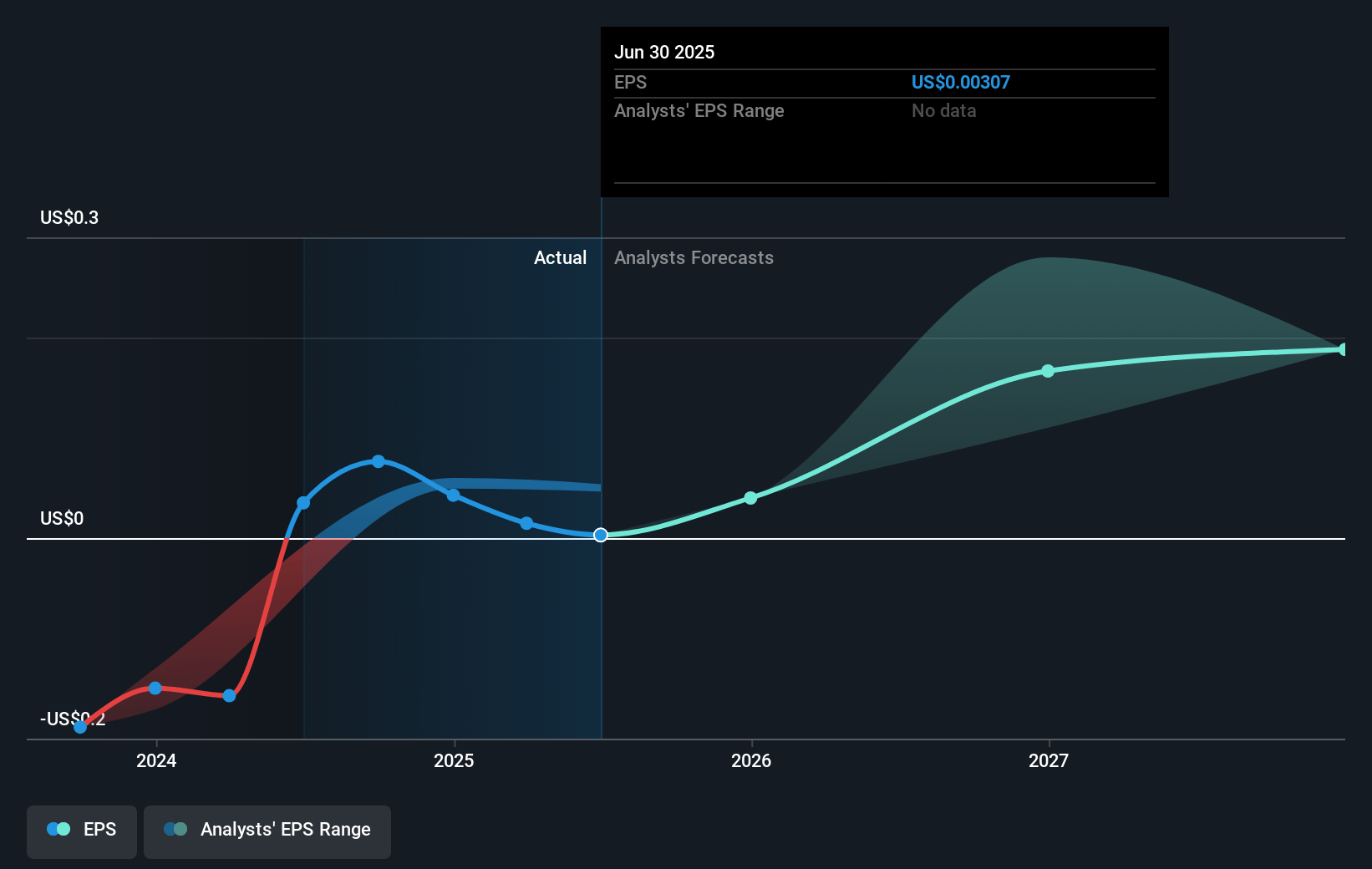

CCC Intelligent Solutions Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The adoption of CCC's new products is progressing slower than anticipated, which may delay revenue growth and affect short-term financial projections.

- Softness in claim volumes has been experienced throughout 2024, potentially impacting revenue as part of CCC's business model is transaction-based.

- Payroll extensions and emerging solutions are still in early stages, and the slower conversion to revenue could mean lower-than-expected financial contributions in the near term.

- Competitive pressures from evolving market demands and new technology entrants might challenge CCC to maintain its growth and share, potentially squeezing net margins.

- Industry-wide labor shortages and the retirement of experienced industry professionals could exacerbate challenges in adoption and execution of new solutions, potentially affecting operational efficiency and revenue realization.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $13.58 for CCC Intelligent Solutions Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $15.0, and the most bearish reporting a price target of just $12.01.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.2 billion, earnings will come to $136.7 million, and it would be trading on a PE ratio of 87.9x, assuming you use a discount rate of 7.2%.

- Given the current share price of $11.24, the analyst's price target of $13.58 is 17.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives