Last Update 16 Jun 26

APPF: AI-Driven Housing Reset Will Support Future Margin Expansion

AppFolio's analyst price targets have seen mixed revisions, with some firms lifting their views by about $4 and others cutting targets by as much as $35 to $57, as analysts reassess the stock's valuation inputs and the housing market backdrop.

Analyst Commentary

Recent AppFolio research reports show a clear split in how analysts are framing the stock, with some highlighting supportive housing trends and product execution, and others focusing on valuation risk and exposure to a potential reset in the housing market.

Bullish Takeaways

- Bullish analysts point to prior research that described the housing market as ready to reset, and view AppFolio as positioned to benefit if property managers continue to invest in software to improve efficiency during that transition.

- The US$4 price target increase reflects confidence that AppFolio can keep executing on its product roadmap. These analysts see this as important for supporting revenue quality and potential operating leverage over time.

- Supportive research initiation with a bullish view signals that some analysts see room for further adoption of AppFolio's platform. They connect this to longer term growth in its customer base and transaction volumes.

- Bullish commentary generally frames current pricing as acceptable for investors who prioritize execution on software delivery and customer retention, even with a mixed housing backdrop.

Bearish Takeaways

- Bearish analysts have cut AppFolio price targets by about US$35 and US$57, indicating concern that earlier valuation assumptions may have been too generous relative to current housing market conditions.

- The target reductions suggest caution around how sensitive AppFolio's growth and profitability could be if property managers slow spending or delay upgrades while the housing market resets.

- Some research highlights the risk that expectations embedded in prior targets may have set too high a bar for execution, particularly around delivering on product initiatives and sustaining adoption trends.

- Overall, the more cautious view frames AppFolio stock as needing clearer evidence of consistent performance and capital discipline before warranting prior, higher price targets.

What’s in the News for AppFolio

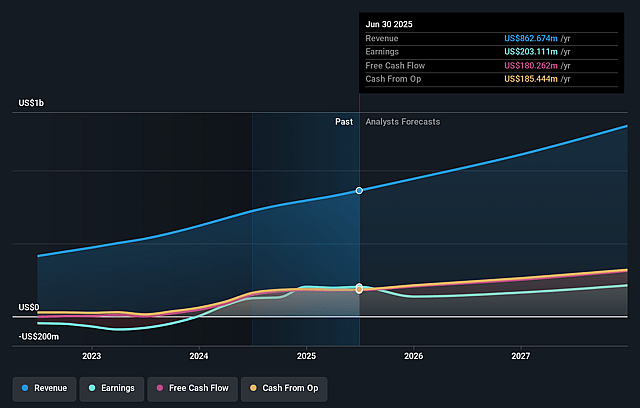

- AppFolio reported Q1 2026 revenue of US$262.21 million and earnings of US$1.61 per share, with management indicating this was a record first quarter for new residential business units on the platform, according to recent earnings coverage.

- Management highlighted broad adoption of AppFolio’s AI-enabled products, including RealmX Performers, with AI actions reported at roughly seven times the level of the prior year, and emphasized a focus on monetization through AI-driven workflows, premium tiers, and value-added services. Source: Q1 2026 earnings reports.

- Cost of revenue was described as flat in recent coverage, while management raised full-year 2026 guidance for revenue growth to 17.5% and projected a non-GAAP operating margin of 26%, citing expectations for profitability and efficiency gains from AI initiatives. Source: Q1 2026 earnings commentary.

- AppFolio launched an agent-to-agent connector that links its Realm-X AI suite with Anthropic’s Claude, aiming to support automated, governed workflows for reporting, occupancy, maintenance, leasing, and marketing; the company plans to feature this at the National Apartment Association’s Apartmentalize conference in June 2026. Source: product integration announcements.

- AppFolio updated 2026 guidance, with revenue expected in a range of US$1.11 billion to US$1.125 billion, and disclosed that between January 1 and March 31, 2026 it repurchased 703,000 shares for US$125.1 million, completing 946,987 shares repurchased for US$175.06 million under its April 24, 2025 buyback plan. Source: company guidance and buyback filings.

Valuation Changes for AppFolio

- Fair Value: Model fair value remains unchanged at $229.25 per share. This indicates no adjustment to the core valuation output in this update.

- Discount Rate: The discount rate has risen slightly from 8.52% to 8.58%, a modest increase that makes future cash flows marginally less valuable in the model.

- Revenue Growth: The revenue growth assumption is essentially unchanged at about 16.25%, with only a negligible numerical adjustment in the underlying input.

- Net Profit Margin: The net profit margin assumption remains steady at roughly 17.63%, with only a very small technical change in the modeled figure.

- Future P/E: The assumed future P/E multiple has risen slightly from 35.06x to 35.12x, a minimal shift in how the model prices AppFolio stock relative to projected earnings.

Key Takeaways

- Rising AI adoption and digital transformation in property management strengthen AppFolio's customer acquisition, platform engagement, and long-term revenue prospects.

- Integrated ecosystem partnerships and investment in high-margin services increase platform stickiness, recurring revenue, and operational efficiency.

- Competitive pressures, regulatory risks, reliance on domestic growth, rising innovation costs, and exposure to third-party threats could constrain future revenue, margins, and differentiation.

Catalysts

About AppFolio- Provides cloud-based platform for the real estate industry in the United States.

- Accelerating adoption of AI-powered workflow automation within property management-demonstrated by a 46% increase in industry intent to use AI and 96% of customers engaging with AI solutions-positions AppFolio to continue expanding unit counts, drive top-line revenue growth, and support future increases in net margins through productivity gains.

- Expansion of integrated ecosystem partnerships (e.g., AppFolio Stack, fintech solutions, and third-party partner integrations) provides customers with more seamless, end-to-end experiences, increasing the platform's stickiness, ARPU, and recurring revenue potential.

- Elevated labor shortages and ongoing economic pressures in real estate are driving property management customers to adopt technology for cost reduction and efficiency, supporting consistent customer acquisition and minimizing churn, which will have a positive impact on revenue and retention rates.

- The growing shift toward digital transformation and cloud-based SaaS across the industry expands AppFolio's addressable market, fueling sustained customer growth, higher subscription sales, and potential long-term earnings expansion.

- Sustained investment in high-margin, value-added services-such as advanced screening (FolioScreen), payment processing, and insurance-alongside continued operational efficiency is expected to further increase net margins and support profitable revenue growth.

AppFolio Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming AppFolio's revenue will grow by 16.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 15.3% today to 17.6% in 3 years time.

- Analysts expect earnings to reach $275.8 million (and earnings per share of $6.85) by about June 2029, up from $152.0 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 36.1x on those 2029 earnings, down from 36.8x today. This future PE is greater than the current PE for the US Software industry at 26.4x.

- Analysts expect the number of shares outstanding to decline by 1.38% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.58%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Customer growth primarily comes from new business wins and increased adoption of premium tiers within an already competitive property management segment, which may face commoditization and pricing pressure as more providers develop similar AI-powered SaaS offerings-risking future revenue growth and margin expansion as customers gain greater bargaining power.

- The company's focus remains overwhelmingly domestic, with no mention of international expansion initiatives, implying a limited addressable market; if industry growth slows or saturates in the U.S., future revenue and earnings growth could be capped as the core customer base matures.

- Heavy investment in product innovation (especially AI features) requires continually rising R&D and go-to-market spend; if competitors develop or offer comparable automation and agentic technologies, AppFolio's differentiation could erode, leading to margin pressures and slower operating leverage improvements.

- Major revenue drivers like screening, payments, and risk mitigation services rely on increasing compliance complexity and data handling; rising regulatory scrutiny and new privacy legislation could require expensive platform overhauls and increase compliance costs, directly impacting net margins.

- Partnerships with fintech and third-party integrations are becoming central to the platform's value proposition, exposing AppFolio to third-party risk (including data security) and greater competitive overlap; any significant cybersecurity incident or loss of integration partners could negatively impact customer trust, retention rates, and long-term revenue stability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $229.25 for AppFolio based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $300.0, and the most bearish reporting a price target of just $185.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $1.6 billion, earnings will come to $275.8 million, and it would be trading on a PE ratio of 36.1x, assuming you use a discount rate of 8.6%.

- Given the current share price of $158.21, the analyst price target of $229.25 is 31.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on AppFolio?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.