Narratives are currently in beta

Key Takeaways

- Strategic collaboration with Amazon and product innovations are expected to drive significant revenue growth in data center semiconductors and AI products.

- Focus on high-margin data center solutions and efficient production ramps will likely enhance operating margins and strengthen Marvell's market position.

- Heavy reliance on AI demand and custom silicon poses revenue risks, while debt may impact financial flexibility amid shifting customer relationships and interest rates.

Catalysts

About Marvell Technology- Provides data infrastructure semiconductor solutions, spanning the data center core to network edge.

- Expansion of strategic relationship with Amazon Web Services through a multigenerational 5-year agreement is expected to drive significant volume for Marvell's data center semiconductors, including custom AI products, which should boost revenue.

- The continued production ramp in custom silicon programs and strong growth in optics are expected to accelerate Marvell's revenue growth and lead to improved operating margins due to operating leverage.

- The release of advanced chipsets like the 3-nanometer 1.6T DSP is projected to strengthen Marvell’s position in the electro-optics market, potentially expanding revenue and increasing margins through improved energy efficiency.

- Marvell's increased focus on the data center, supported by strategic redirection of R&D investments, is expected to capitalize on the AI super cycle and enhance earnings by driving higher-margin products.

- Strong operating cash flows and stock repurchase programs are projected to boost EPS, while supply chain capacity to support customer growth forecasts should ensure revenue stability and expansion.

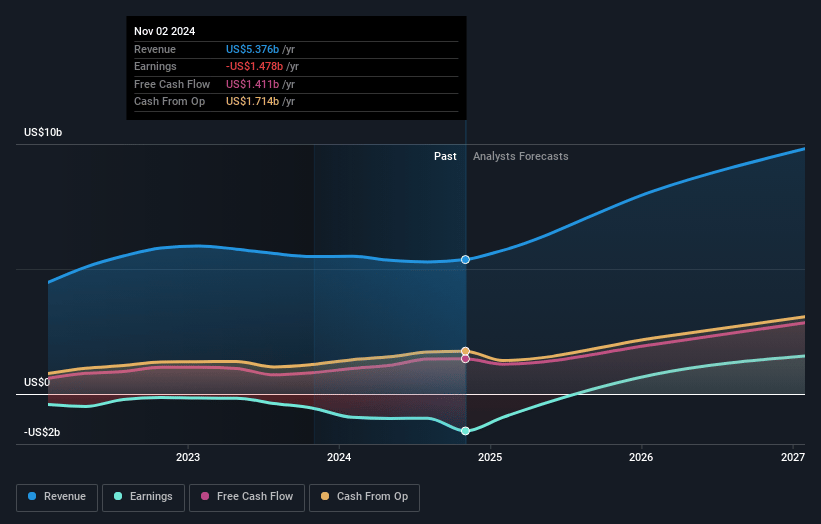

Marvell Technology Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Marvell Technology's revenue will grow by 28.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from -27.5% today to 21.9% in 3 years time.

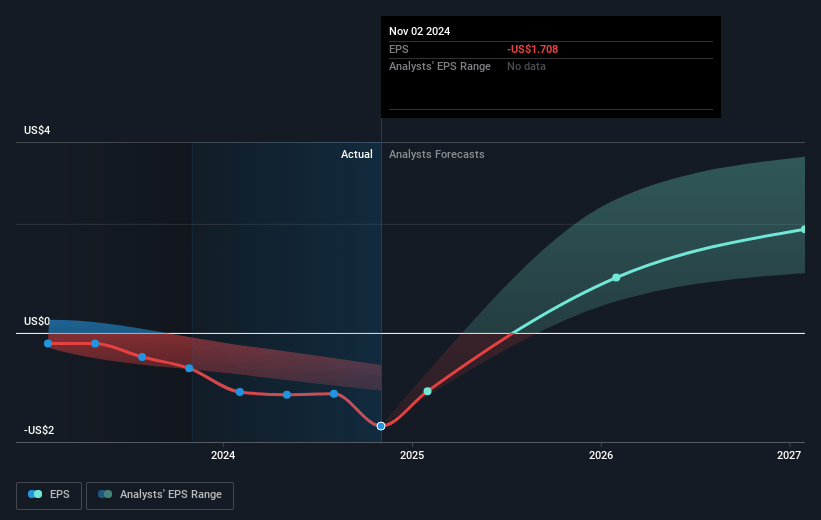

- Analysts expect earnings to reach $2.5 billion (and earnings per share of $2.92) by about January 2028, up from $-1.5 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 54.9x on those 2028 earnings, up from -60.8x today. This future PE is greater than the current PE for the US Semiconductor industry at 31.2x.

- Analysts expect the number of shares outstanding to decline by 0.73% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.02%, as per the Simply Wall St company report.

Marvell Technology Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The substantial reliance on AI-driven demand and custom silicon might present a risk if AI adoption slows or there are technological setbacks, potentially impacting Marvell's revenue growth and operating margins.

- Significant investments being redirected towards the data center from other end markets may undermine diversification and leave Marvell vulnerable to downturns in the data center or AI sectors, affecting revenue stability.

- The stated plan to increase R&D intensity on data center results in high upfront costs and restructuring charges, highlighting risks that could potentially weigh on net margins if anticipated revenue growth fails to materialize.

- The AI-guided custom silicon and electro-optics markets have high barriers to entry, but increasing reliance on a handful of large customers like AWS and other major cloud providers creates concentration risk, which may impact earnings stability if these customer relationships change or shift.

- Marvell's significant debt load, with total debt at $4.1 billion, could impair financial flexibility, particularly in an environment of rising interest rates or if expected cash flows from high-growth segments, such as AI, do not meet projections, affecting net profits and investor returns.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $127.52 for Marvell Technology based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $160.0, and the most bearish reporting a price target of just $87.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $11.3 billion, earnings will come to $2.5 billion, and it would be trading on a PE ratio of 54.9x, assuming you use a discount rate of 8.0%.

- Given the current share price of $103.88, the analyst's price target of $127.52 is 18.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives