Key Takeaways

- Enphase aims to boost margins with U.S. production and innovative products, leveraging tax credits and incentives for domestic manufacturing.

- Expansion into new international markets and high-margin service areas like AI energy management supports revenue growth and improved net margins.

- Decreasing European demand, supply chain reliance on China, and strong competition could pressurize Enphase's revenue growth, market share, and profit margins.

Catalysts

About Enphase Energy- Designs, develops, manufactures, and sells home energy solutions for the solar photovoltaic industry in the United States and internationally.

- Enphase is focusing on significantly increasing shipments from U.S. facilities, leveraging production tax credits, which should enhance gross margins through domestic manufacturing incentives.

- The introduction of the IQ8HC microinverters with higher domestic content SKUs is expected to qualify for a 10% domestic content ITC adder, potentially boosting revenue through improved competitiveness and cost savings for lease and PPA customers.

- New product launches, such as the fourth-generation IQ Battery and commercial IQ8P microinverters, are designed to reduce costs and increase system efficiency, likely contributing to higher revenue and improved net margins in future periods.

- Enphase's expansion into new geographical markets like Japan and strengthening its presence in underpenetrated markets such as Germany and the Netherlands are expected to drive revenue growth through increased market share and international sales.

- The roll-out of AI-powered energy management software and expansion into EV charging solutions positions Enphase for growth in related, high-margin service revenues, enhancing overall net margins and earnings.

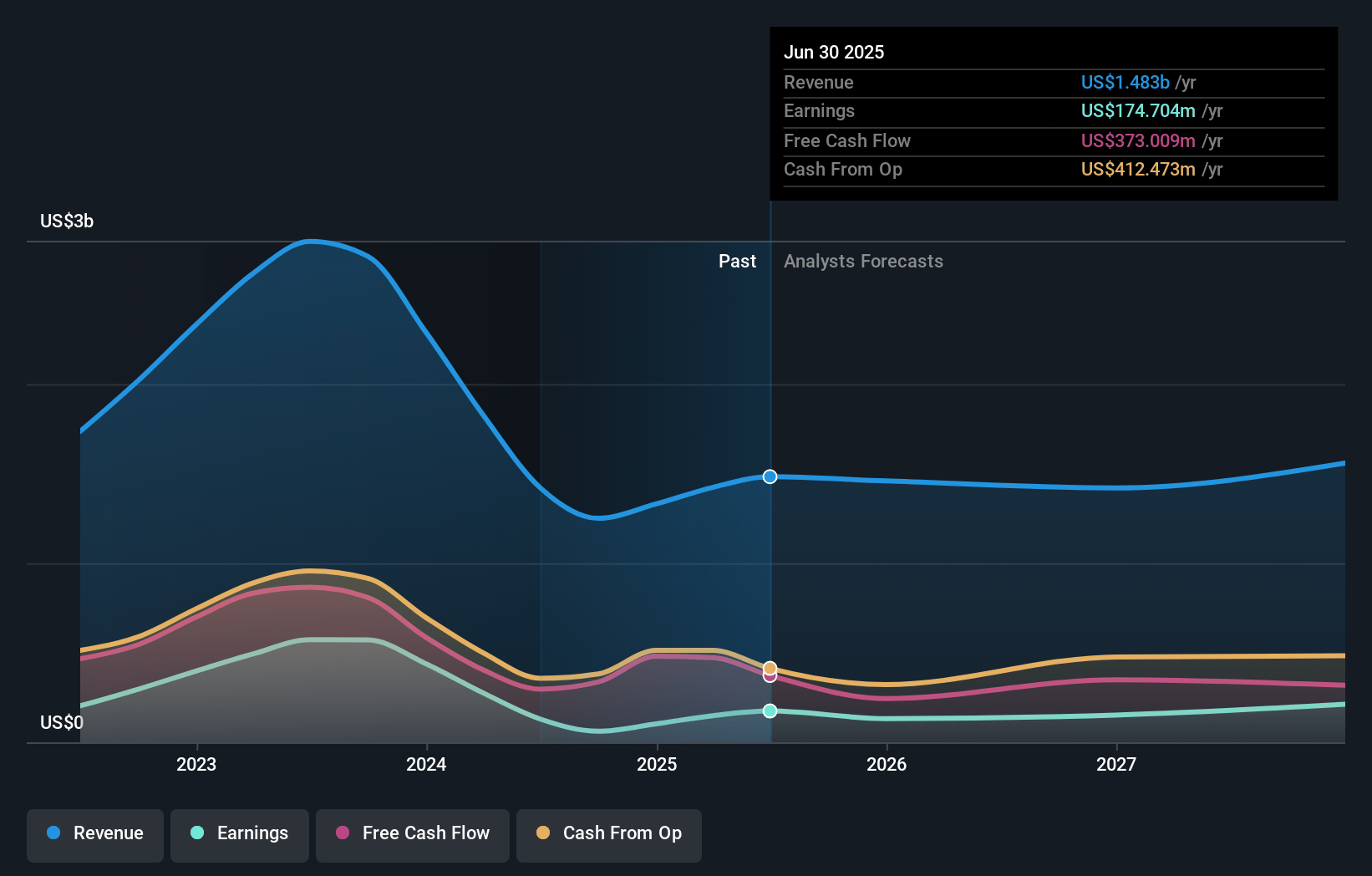

Enphase Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Enphase Energy's revenue will grow by 24.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.9% today to 27.2% in 3 years time.

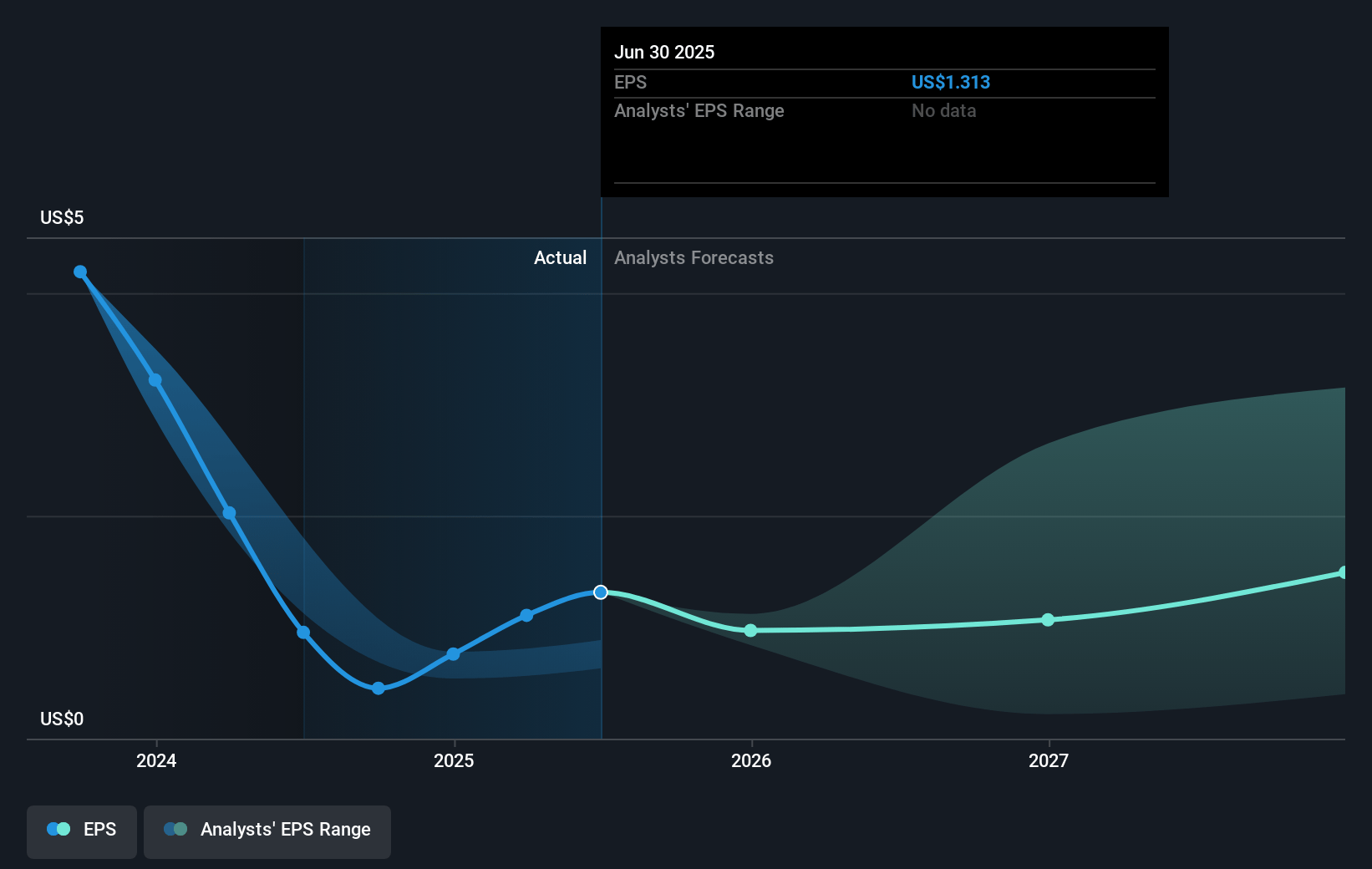

- Analysts expect earnings to reach $648.4 million (and earnings per share of $3.94) by about January 2028, up from $61.4 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $288.9 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 28.3x on those 2028 earnings, down from 136.9x today. This future PE is lower than the current PE for the US Semiconductor industry at 31.2x.

- Analysts expect the number of shares outstanding to grow by 6.76% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.34%, as per the Simply Wall St company report.

Enphase Energy Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Decreasing power prices in Europe and slow economic growth can negatively impact consumer confidence and demand for Enphase's products, limiting revenue growth and earnings potential in that region.

- The bankruptcy of a large U.S. customer poses a revenue risk, as some of these lost revenues may not be fully recovered in future quarters.

- The company's reliance on suppliers in China for cell packs, amid potential geopolitical tensions and supply chain uncertainties, could lead to disruptions impacting production costs and net margins.

- Ongoing regulatory uncertainty in European markets, such as the Netherlands, could delay consumer transitions to solar plus storage systems, thereby affecting revenue and market penetration.

- Competition from companies like Tesla's Powerwall 3 could affect Enphase's battery storage market share and pricing power, potentially impacting revenue and profit margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $87.95 for Enphase Energy based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $145.0, and the most bearish reporting a price target of just $57.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.4 billion, earnings will come to $648.4 million, and it would be trading on a PE ratio of 28.3x, assuming you use a discount rate of 8.3%.

- Given the current share price of $62.24, the analyst's price target of $87.95 is 29.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

GO

Equity Analyst

Market Leadership Amidst Increasing Competition Won't Hurt Solid Revenue Growth

Key Takeaways Electricity prices, incentives (tax credits, net metering) and technology advancements will drive sales. Microinverters are gaining traction but their advantage over traditional inverters is unclear.

View narrativeUS$76.86

FV

14.6% undervalued intrinsic discount24.00%

Revenue growth p.a.

5users have liked this narrative

0users have commented on this narrative

9users have followed this narrative

4 months ago author updated this narrative