Last Update 26 Jun 26

Fair value Decreased 25%DVLT: Wireless Audio Expansion And Tokenization Platform Will Drive Future Upside

Analysts have trimmed their Datavault AI price target by $1, reflecting updated views on fair value, a higher discount rate, and revised expectations for revenue growth, profit margins, and future P/E following recent research.

What’s in the News for Datavault AI

- WiSA Technologies, a division within Datavault AI’s Acoustic Sciences business, integrated its WiSA E Enterprise wireless audio module into Goldhorn branded Goho LS7 2.0 and 5.1 home theater and karaoke systems in China, combining 4K projectors with multi channel wireless audio for secure, low latency connectivity (source: multiple news outlets).

- Law firm Bragar Eagel & Squire, P.C. opened an investigation into Datavault AI on behalf of stockholders following a Wolfpack Research short report that alleged the company relies on misleading press releases and raised questions about its leadership and blockchain marketplace activity (source: Bragar Eagel & Squire release and related reporting).

- Johnson Fistel, PLLP began a separate investigation into Datavault AI after the same Wolfpack Research report accused the company of making false and misleading statements about its AI, quantum computing, and blockchain operations and of engaging in stock promotion through press releases (source: Johnson Fistel announcement and related coverage).

- Datavault AI’s auditor, BPM LLP, resigned as the company’s independent registered public accounting firm on 15 June 2026. Datavault AI stated that it is in the process of selecting a successor and will disclose the new firm in accordance with SEC requirements.

- Datavault AI entered a Mutual Services Agreement and Statement of Work with Perpetuals.com Ltd. to list its real world asset token programs on the Perpetuals exchange, initially covering the MTB Copper project and providing a regulated trading venue for tokenized commodity assets backed by in ground resources and issued on Datavault AI’s blockchain platform.

Valuation Changes for Datavault AI

- Fair Value: revised from $4.0 to $3.0, indicating a lower assessed equity value per share in the latest model.

- Discount Rate: adjusted from 10.66% to 11.25%, reflecting a higher required return for Datavault AI’s cash flows.

- Revenue Growth: updated from 119.22% to 144.91%, with the new assumptions pointing to a very large projected growth rate for Datavault AI’s dollar revenue base.

- Net Profit Margin: lifted from 3.46% to 16.88%, signaling a much higher assumed profitability level on future dollar earnings.

- Future P/E: reduced from 286.38x to 41.70x, meaning the valuation model now applies a substantially lower earnings multiple to Datavault AI.

Key Takeaways

- Strategic partnerships, proprietary technology, and acquisitions position Datavault AI for robust, high-margin recurring revenue growth across diverse, regulated data markets.

- Compliance-first infrastructure and alliances with industry leaders enable scalable, secure solutions tailored to capitalize on accelerating digital transformation and shifting market regulations.

- Heavy reliance on unrecognized revenue, aggressive acquisitions, exposure to regulatory risks, and dependence on key partnerships could create earnings volatility and limit sustainable growth.

Catalysts

About Datavault AI- A data sciences technology company, owns and operates data management platforms by supercomputing capabilities in the North America, Asia Pacific, Europe, and internationally.

- The announcement of multiple proprietary data exchange platforms (International Elements Exchange, NIL Exchange, Political Exchange) launching on compliant, AI-powered infrastructure positions Datavault AI to capitalize on accelerating digital transformation across sectors, suggesting significant future revenue growth as these exchanges monetize new verticals.

- The company's deepened alliance with IBM, including Platinum Partner status and integration of Watsonx.ai, provides Datavault with scalable AI capabilities and best-in-class cybersecurity, supporting enterprise-grade adoption and efficient scaling, which could drive higher net margins by improving operational leverage and reducing per-unit delivery costs.

- Recent advancements in patented proprietary technology and licensing arrangements (e.g., Nyiax, Dolby, WiSA, DataScore systems) and a strengthening of the IP portfolio set Datavault apart from commoditized competitors, enabling monetization of unique solutions that may boost high-margin recurring revenue streams.

- The immediate booking of $2.5 million in licensing (with additional revenue recognition expected as contracts are fulfilled) and strategic acquisitions (CompuSystems, API Media) unlock access to new customer bases and event-driven data flows, enhancing revenue predictability and offering step-changes in topline growth trajectory.

- Regulatory shifts enabling large-scale data monetization in U.S. financial markets (GENIUS Act) alongside Datavault's compliance-first, automated governance infrastructure position the company to benefit from increasing mandates for data transparency and provenance, likely sustaining durable, high-quality earnings growth.

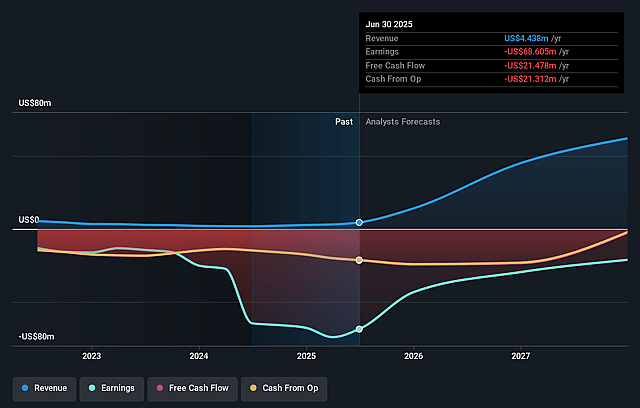

Datavault AI Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Datavault AI's revenue will grow by 144.9% annually over the next 3 years.

- Analysts are not forecasting that Datavault AI will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Datavault AI's profit margin will increase from -292.7% to the average US Semiconductor industry of 16.9% in 3 years.

- If Datavault AI's profit margin were to converge on the industry average, you could expect earnings to reach $103.8 million (and earnings per share of $0.1) by about June 2029, up from -$122.6 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 41.7x on those 2029 earnings, up from -2.3x today. This future PE is lower than the current PE for the US Semiconductor industry at 73.6x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.25%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company's heavy reliance on booking-but not yet recognizing-large licensing transactions (such as with Nyiax) introduces revenue recognition risks and underscores potential volatility in actual realized revenue, which could impact reported earnings and undermine investor confidence.

- Datavault AI's aggressive acquisition and expansion strategy (e.g., CSI and API Media acquisitions, significant growth targets) could strain integration capabilities and lead to operational inefficiencies; if synergies are not quickly realized or execution falters, this could pressure net margins and delay sustainable profitability.

- The company's positioning in tokenomics, blockchain, and real-world asset exchanges exposes Datavault AI to increased uncertainty and future regulatory scrutiny, with evolving global data privacy and financial compliance frameworks potentially constraining its business model and addressable markets, thereby limiting revenue growth.

- Dependence on key partnerships-such as IBM Platinum and tech integrations with Nyiax and Dolby-and references to unique patent-backed technologies heighten concentration risks; should any partnership falter or intellectual property advantages erode (e.g., due to legal challenges or industry commoditization), competitive moat and revenue streams could be compromised, negatively impacting long-term earnings.

- The narrative highlights rapid scaling ambitions and a focus on capturing new, innovative markets like NIL, political, and elements exchanges, but these early-stage, novel markets can be highly competitive and susceptible to disruption by large, established technology incumbents; failure to establish a dominant foothold amid intensifying competition could suppress future revenue and earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $3.0 for Datavault AI based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $615.2 million, earnings will come to $103.8 million, and it would be trading on a PE ratio of 41.7x, assuming you use a discount rate of 11.3%.

- Given the current share price of $0.34, the analyst price target of $3.0 is 88.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Datavault AI?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.