Key Takeaways

- Focused investments in omnichannel integration, product expansion, and modernized marketing are enhancing customer engagement, brand appeal, and revenue potential.

- Operational efficiency, inventory discipline, and agility are supporting margin resilience and sustainable long-term earnings, despite external economic pressures.

- Heavy tariff costs, dependence on discounts, rising expenses, demographic limitations, and competitive pressures threaten profitability and long-term growth in a challenging retail landscape.

Catalysts

About J.Jill- Operates as an omnichannel retailer for women’s apparel in the United States.

- J.Jill is positioned to benefit from the growth in its core demographic-women aged 40+, a segment with rising purchasing power and long-term market stability-supporting sustained demand and higher, more predictable revenues.

- The company's accelerated investments in omnichannel capabilities, including ship-from-store fulfillment, expanded POS/OMS systems, and digitized loyalty programs, are improving the seamless integration of online and in-store experiences, which should drive higher conversion rates, improved customer retention, and top-line revenue growth.

- Enhanced product assortment strategies, such as increasing the versatility and relevance of offerings and expanding into scalable categories like accessories, aim to capture greater share of customer wardrobe and broaden appeal to both loyal and new shoppers-potentially supporting both revenue growth and gross margin expansion.

- Initiatives to modernize marketing (including local TV testing, refreshed in-store merchandising, and increased focus on digital channels) directly target brand awareness and customer file expansion, which could drive sustained gains in customer acquisition, average order value, and net revenue.

- Ongoing inventory discipline, technology-enabled operational improvements, and a culture focused on agility and efficiency are likely to support strong free cash flow conversion and facilitate margin resilience-even in the face of macro headwinds like tariffs-thereby positively impacting net income and long-term earnings power.

J.Jill Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming J.Jill's revenue will grow by 1.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.1% today to 10.6% in 3 years time.

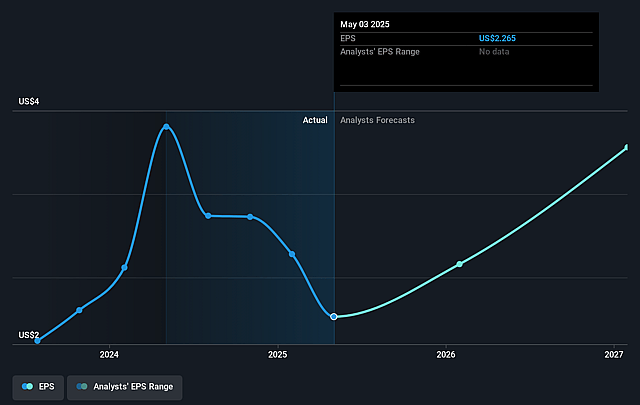

- Analysts expect earnings to reach $67.1 million (and earnings per share of $4.35) by about September 2028, up from $36.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 6.2x on those 2028 earnings, down from 6.8x today. This future PE is lower than the current PE for the US Specialty Retail industry at 19.2x.

- Analysts expect the number of shares outstanding to grow by 0.95% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.46%, as per the Simply Wall St company report.

J.Jill Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Significant and persistent tariff pressures (with rates as high as 20% on major sourcing countries and 50% on India) are expected to drive material increases in cost of goods sold for the foreseeable future, putting sustained downward pressure on gross margins and overall profitability.

- The company's heavy reliance on promotional activity and markdowns to stimulate sales and clear inventory signals underlying demand fragility and price sensitivity among its core customer base; this pattern may persist long-term and erode net margins if pricing power fails to improve.

- Increased store and occupancy costs, driven by lease renewals and net new store openings, combined with ongoing investments in physical locations, expose J.Jill to secular headwinds affecting brick-and-mortar retail-especially as e-commerce continues to gain market share-threatening long-term earnings growth.

- Slow or limited success in broadening the customer file beyond the existing core demographic, and the company's lack of brand resonance with younger shoppers, risks stagnating revenue growth and compressing lifetime customer value as demographic changes evolve.

- The continued presence of an uncertain and inflationary macroeconomic environment, combined with rising SG&A expenses and heightened competition in specialty apparel (including fast fashion and digital-native entrants), may require even greater promotional intensity and investment, adversely affecting both revenue stability and net income over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $20.667 for J.Jill based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $26.0, and the most bearish reporting a price target of just $16.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $633.7 million, earnings will come to $67.1 million, and it would be trading on a PE ratio of 6.2x, assuming you use a discount rate of 10.5%.

- Given the current share price of $16.49, the analyst price target of $20.67 is 20.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.