Narratives are currently in beta

Key Takeaways

- Brand reinvigoration and activewear expansion strategies are driving sustainable growth and boosting revenue potentials.

- Operational efficiency improvements and strategic supply chain enhancements are expected to enhance net margins and resilience.

- Dependence on weather-sensitive products and competitive pressures challenge consistent growth, while supply chain risks and strategic missteps threaten margins and balanced brand performance.

Catalysts

About Gap- Operates as an apparel retail company.

- Gap Inc. is implementing a brand reinvigoration playbook across its portfolio, leading to consistent market share gains, which is expected to drive sustainable revenue growth. This could positively impact future revenue.

- Expansion in the Activewear segment, particularly with Old Navy as a top 5 player in the active category, presents significant growth opportunities, particularly in women's activewear. This expansion is likely to boost revenues.

- Gap's improvement in gross margin and operational efficiency, with efforts to manage SG&A, provides potential for enhanced net margins in the future.

- Strategic investments are being made to improve the in-store and online customer experience, particularly through store refreshes across brands such as Gap, Banana Republic, and Athleta, which could strengthen brand loyalty and potentially boost revenue.

- Supply chain enhancements and diversification efforts, reducing reliance on China, are expected to improve operational resilience and could protect or enhance net margins going forward.

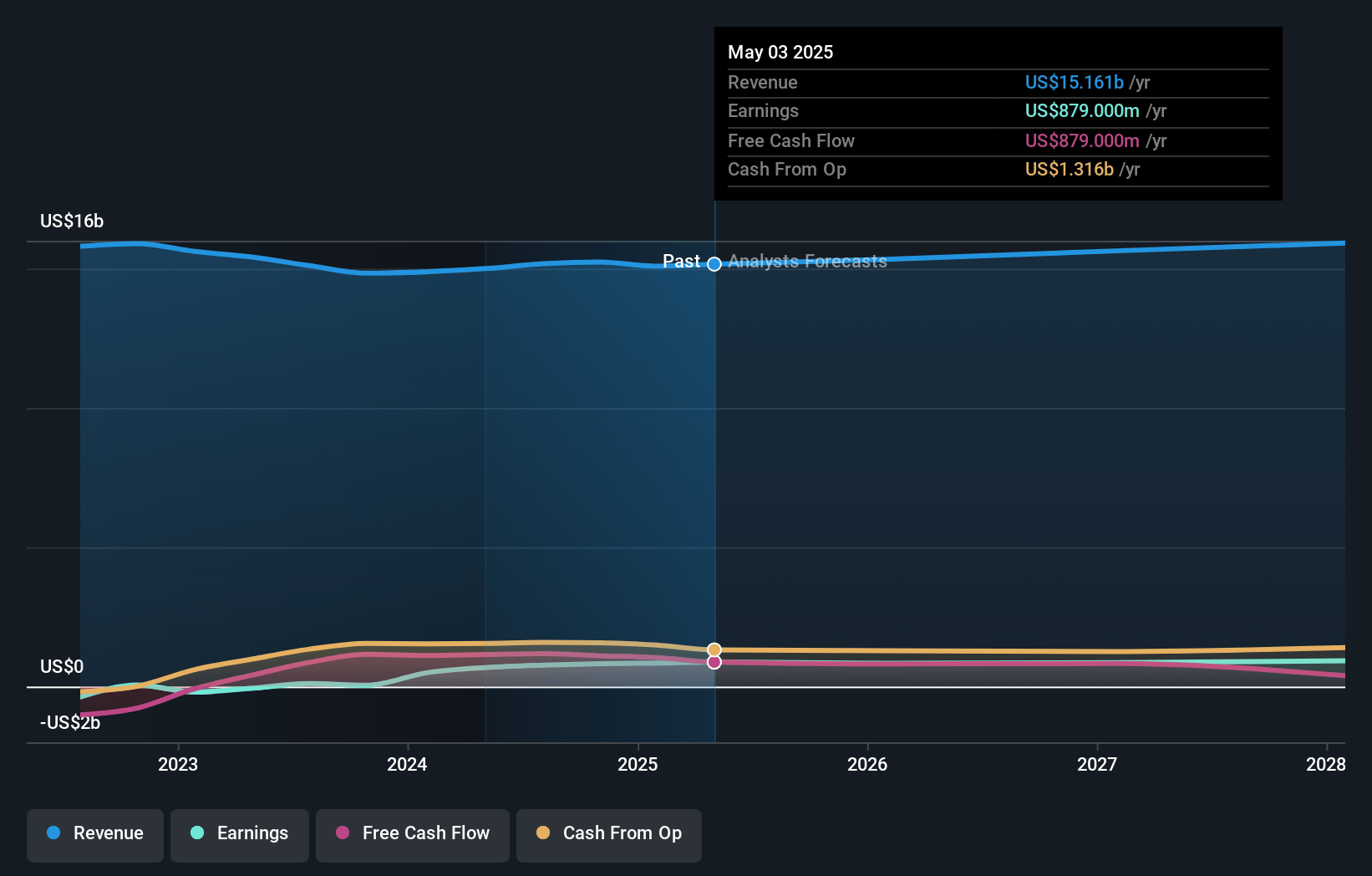

Gap Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Gap's revenue will grow by 1.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.4% today to 5.6% in 3 years time.

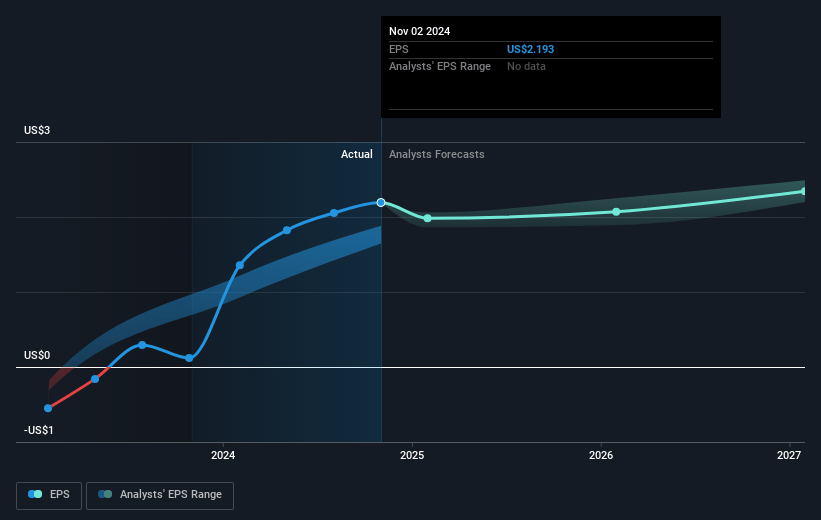

- Analysts expect earnings to reach $887.5 million (and earnings per share of $2.57) by about January 2028, up from $823.0 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 13.9x on those 2028 earnings, up from 10.9x today. This future PE is lower than the current PE for the US Specialty Retail industry at 16.5x.

- Analysts expect the number of shares outstanding to decline by 2.95% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.05%, as per the Simply Wall St company report.

Gap Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The reliance on weather-sensitive products leads to vulnerabilities in sales performance, particularly in the kids and baby categories, affecting Gap's ability to maintain consistent revenue growth.

- The company's supply chain still faces risks from natural disasters and port strikes, which could disrupt operations and impact cost management, ultimately affecting net margins.

- The competitive apparel market, particularly in categories like activewear, requires strategic expansion to maintain and grow market share; failure to do so could impact future revenue projections.

- The emphasis on promotions to compete in a crowded market could erode gross margins over time if not managed strategically, impacting overall profitability.

- While Old Navy and Athleta show strength, the slower progress in Banana Republic, particularly in women's apparel, indicates potential difficulties in achieving balanced growth across all brands, which could affect overall earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $28.36 for Gap based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $35.0, and the most bearish reporting a price target of just $16.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $15.9 billion, earnings will come to $887.5 million, and it would be trading on a PE ratio of 13.9x, assuming you use a discount rate of 8.1%.

- Given the current share price of $23.76, the analyst's price target of $28.36 is 16.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives