Key Takeaways

- Expansion of in-store services, digital engagement, and premium product focus aims to boost recurring revenues, customer loyalty, and market share.

- Operational efficiencies, proprietary brands, and cost discipline are expected to improve margins and earnings resilience despite competitive and economic pressures.

- Persistent revenue declines, store closures, financial constraints, and sluggish services growth underscore ongoing challenges that threaten future performance and limit turnaround prospects.

Catalysts

About Petco Health and Wellness Company- Operates as a health and wellness company, focuses on enhancing the lives of pets, pet parents, and its Petco partners in the United States, Mexico, and Puerto Rico.

- Petco's emphasis on expanding and optimizing its in-store veterinary and grooming services, including software upgrades and operational improvements, sets the stage for higher-margin, recurring revenue streams and improved customer loyalty-positively impacting both gross margins and long-term earnings.

- The company's accelerated product assortment resets (cat and dog food) and data-driven SKU rationalization are aimed at better aligning inventory with growing consumer trends toward premium and needs-based pet care, which should drive basket size, transaction growth, and support top-line revenue recovery later in the year.

- Strategic investment in digital appointment scheduling, test-and-learn customer engagement initiatives, and an upcoming membership program are designed to meet rising consumer expectations for omnichannel and personalized experiences, setting up Petco for improved retention, higher customer lifetime value, and market share gains-all leading to more stable recurring revenues.

- Enhanced cost discipline, SG&A leverage, and operational efficiencies-driven by a company-wide mindset shift and centralized best practices-are expected to expand operating margins, support sustained EBITDA growth, and improve cash flow, even in a challenging macro environment.

- Ongoing efforts to strengthen supplier partnerships and proprietary brand development (especially in the face of tariffs) will help drive product innovation, higher-margin sales, and brand differentiation, boosting gross margins and earnings resilience amid intensifying competition and input cost pressures.

Petco Health and Wellness Company Future Earnings and Revenue Growth

Assumptions

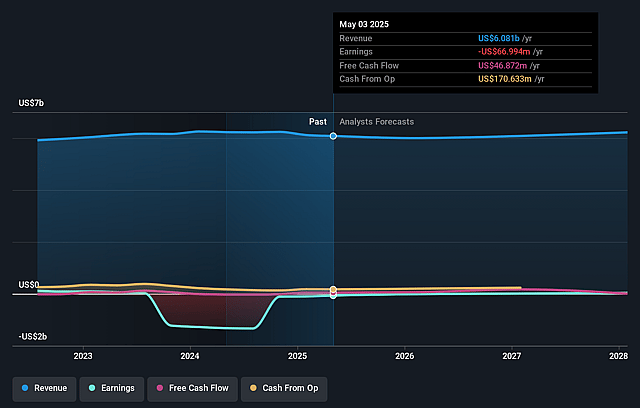

How have these above catalysts been quantified?- Analysts are assuming Petco Health and Wellness Company's revenue will decrease by 0.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from -1.1% today to 0.6% in 3 years time.

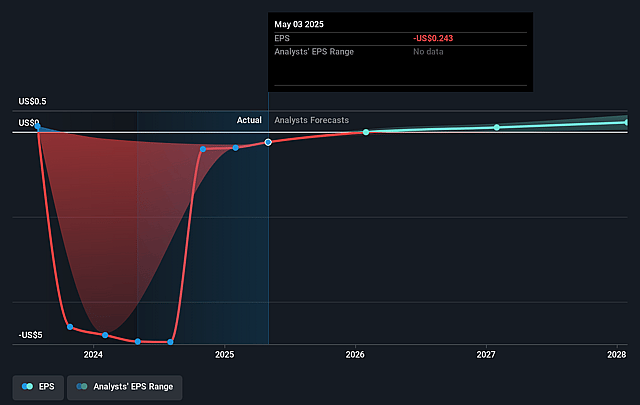

- Analysts expect earnings to reach $37.0 million (and earnings per share of $0.19) by about August 2028, up from $-67.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $112.0 million in earnings, and the most bearish expecting $-18 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 41.3x on those 2028 earnings, up from -14.2x today. This future PE is greater than the current PE for the US Specialty Retail industry at 19.2x.

- Analysts expect the number of shares outstanding to grow by 1.69% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.32%, as per the Simply Wall St company report.

Petco Health and Wellness Company Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Comparable sales were down 1.3% and net sales declined 2.3% year-over-year in Q1 2025, with management guiding for overall net sales to be down low single digits for the full year. This negative top-line trend indicates ongoing revenue headwinds and suggests that demand challenges persist, which could weigh on future revenue growth and impede share price appreciation.

- The company is closing 20 to 30 stores in 2025 after shutting 25 in 2024, highlighting structural pressure on its brick-and-mortar footprint as more consumer spending shifts online. Long-term secular growth of e-commerce and direct-to-consumer models poses a risk to brick-and-mortar-centric companies like Petco, potentially dragging down revenue and margins.

- Petco's free cash flow was negative $44 million in Q1 2025, and the balance sheet remains burdened by high debt and lease obligations, with meaningful net interest expense (~$130 million annualized). These factors constrain financial flexibility and could limit the company's ability to invest in digital transformation, store upgrades, or growth initiatives crucial to net margin and earnings expansion.

- The company's services segment, while still growing, saw net services growth slow to just +1% year-over-year and the core Vital Care membership offering has been deemphasized ahead of a relaunch, acting as a drag within services. Lackluster growth or execution missteps in high-margin recurring services represent a risk to both revenue growth and future margin expansion.

- Management acknowledges improvement plans (e.g., merchandising resets, new loyalty programs, cost discipline) are still in early phases and growth initiatives will not materialize until late 2025 or beyond. Continued weak transaction trends (noted as the biggest drag on comps) and delays or underperformance in these efforts could drive continued stagnation or contraction in revenue and earnings, limiting upside for the share price over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $3.679 for Petco Health and Wellness Company based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $4.67, and the most bearish reporting a price target of just $2.5.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $6.2 billion, earnings will come to $37.0 million, and it would be trading on a PE ratio of 41.3x, assuming you use a discount rate of 12.3%.

- Given the current share price of $3.42, the analyst price target of $3.68 is 7.0% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.