Narratives are currently in beta

Key Takeaways

- Strategic projects and digital initiatives could bolster revenue and earnings, enhancing both physical and digital retail experiences.

- Financial stability, highlighted by efficient debt management, supports sustainable growth in dividends and earnings per share.

- Strong demand and increased leasing, combined with operational excellence and robust international performance, suggest potential for revenue growth and financial stability.

Catalysts

About Simon Property Group- Simon Property Group, Inc. (NYSE:SPG) is a self-administered and self-managed real estate investment trust (“REIT”).

- Simon Property Group's increasing development and redevelopment pipeline, with a commitment to projects worth about $1.5 billion annually, suggests a strategic push towards future growth. This focus could bolster revenue and earnings as new properties come online and generate income.

- Continued leasing momentum, demonstrated by a high occupancy rate and active redevelopment, suggests Simon Property Group is poised to sustain strong revenue growth. Improving merchandising mix and bringing in high-demand tenants can also enhance net margins.

- The introduction and expected impact of Shop Simon's digital initiatives may provide an omnichannel retail experience, potentially increasing both physical and digital traffic. This innovation could lead to incremental revenue, positively impacting earnings.

- The company's stated intention to improve its bottom-tier mall performance indicates untapped potential for growth. By enhancing underperforming assets that currently contribute less, Simon Property Group aims to improve net operating income and expand net margins over time.

- Strong financial positioning, exemplified by refinance operations and a $1.3 billion property mortgage refinancing at an average rate of 6.13%, suggests that the company can manage its debt efficiently. This financial stability supports sustainable dividend growth and earnings per share.

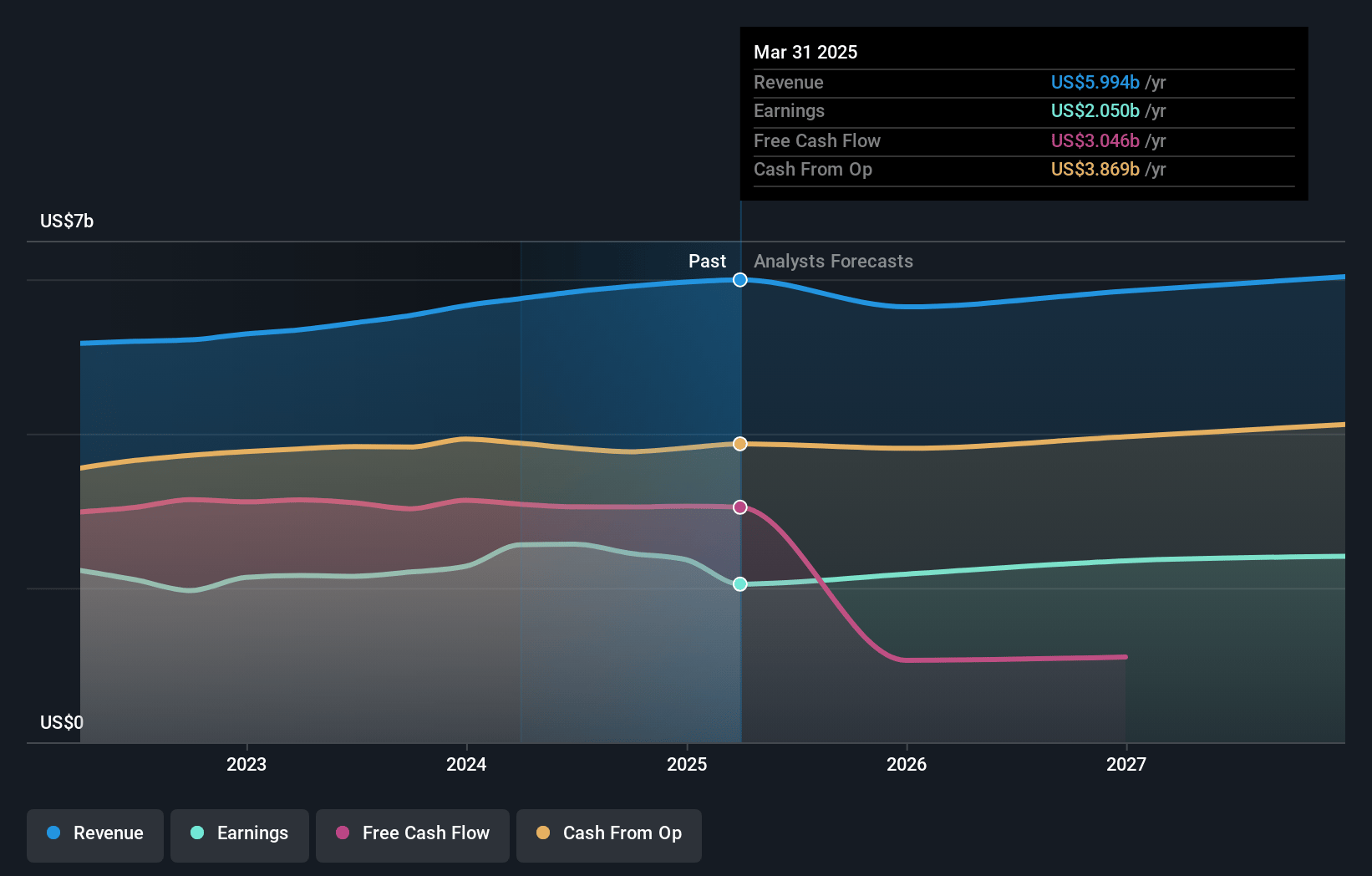

Simon Property Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Simon Property Group's revenue will decrease by 0.3% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 41.4% today to 39.8% in 3 years time.

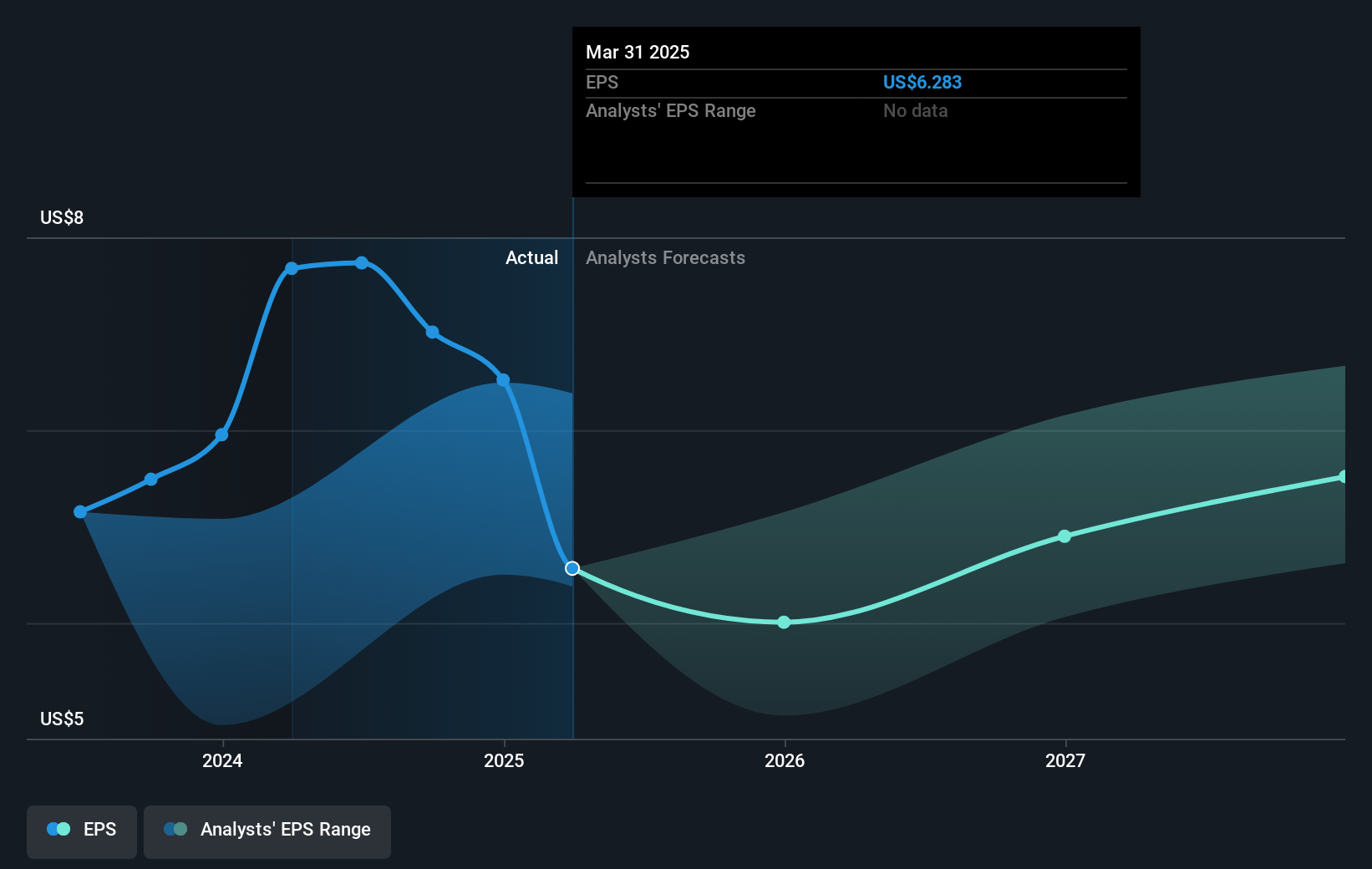

- Analysts expect earnings to remain at the same level they are now, that being $2.4 billion (with an earnings per share of $6.8). The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 33.7x on those 2027 earnings, up from 24.0x today. This future PE is lower than the current PE for the US Retail REITs industry at 35.8x.

- Analysts expect the number of shares outstanding to decline by 2.39% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.46%, as per the Simply Wall St company report.

Simon Property Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Strong demand for Simon Property Group's retail spaces, increased leasing volumes, and occupancy gains suggest potential for revenue stability or growth, which could positively impact earnings.

- A-rated balance sheet and low dividend payout ratio indicate financial strength and stability, potentially supporting future profit margins and net margins.

- Continued operational excellence and leasing momentum shown by a 5.4% increase in domestic NOI suggest that earnings and revenue projections could exceed expectations.

- The development and redevelopment pipeline, combined with a focus on improving merchandising mix and new projects, could increase revenue and stabilize net margins over the long term.

- The strong financial performance of international operations, contributing significantly to growth, could enhance overall earnings and profit margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $184.69 for Simon Property Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $220.0, and the most bearish reporting a price target of just $150.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $6.0 billion, earnings will come to $2.4 billion, and it would be trading on a PE ratio of 33.7x, assuming you use a discount rate of 7.5%.

- Given the current share price of $179.96, the analyst's price target of $184.69 is 2.6% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives