Narratives are currently in beta

Key Takeaways

- FDA approvals and new product expansions position Vericel for sustained revenue and profit growth, with potential benefits from larger patient populations.

- Growing adoption of MACI and NexoBrid, along with strategic manufacturing and market expansion, signals promising future revenue and margin improvements.

- Rising operating expenses and reliance on surgeon adoption present risks to revenue growth and investor confidence amidst ongoing net losses.

Catalysts

About Vericel- A commercial-stage biopharmaceutical company, engages in the research, development, manufacture, and distribution of cellular therapies for sports medicine and severe burn care markets in North America.

- FDA approval of MACI Arthro and NexoBrid pediatric indication positions Vericel for sustained high revenue and profit growth, as new products may expand utilization and serve larger patient populations, impacting future revenue and earnings positively.

- Record third-quarter MACI revenue growth driven by a significant increase in both biopsy surgeons and biopsies per surgeon, coupled with peer-to-peer program expansion, suggests sustained momentum that could boost future revenues substantially.

- Strong initial surgeon interest and engagement in MACI Arthro, particularly among high-volume arthroscopy surgeons, could lead to a significant improvement in overall MACI utilization, strengthening future revenue prospects.

- NexoBrid's increasing adoption, with a growing number of burn centers completing P&T Committee submissions and placing orders, indicates potential for robust Burn Care revenue growth, enhancing overall revenue trajectory.

- The completion of Vericel’s new manufacturing facility by early 2025 and potential international market exploration for MACI provide strategic flexibility, potentially spurring future revenue growth and enhancing net margins due to efficiencies in production and scale.

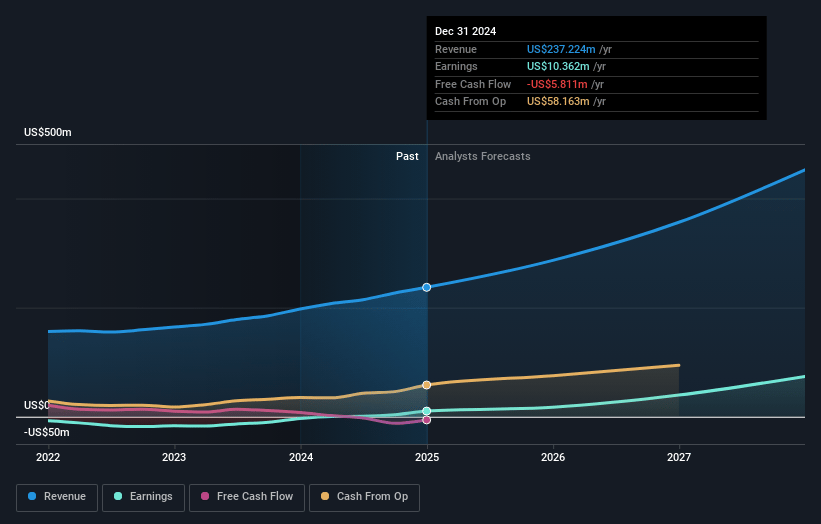

Vericel Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Vericel's revenue will grow by 24.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.6% today to 14.6% in 3 years time.

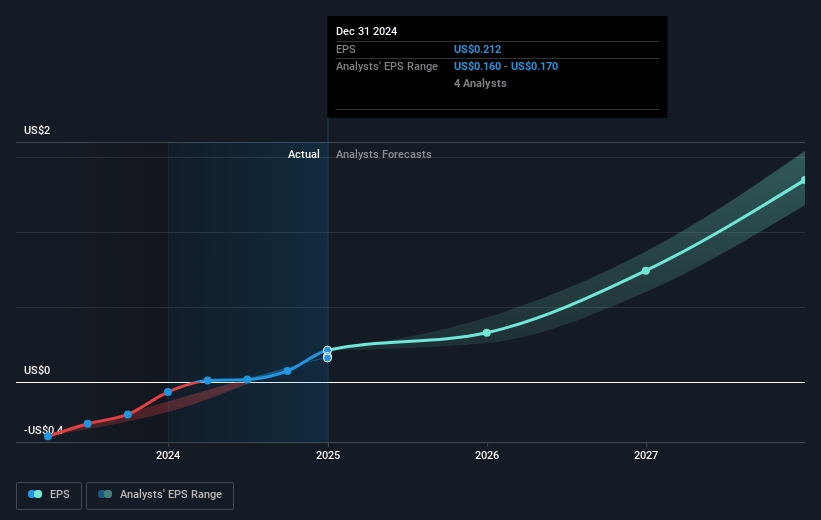

- Analysts expect earnings to reach $64.5 million (and earnings per share of $1.19) by about January 2028, up from $3.5 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 65.7x on those 2028 earnings, down from 836.2x today. This future PE is greater than the current PE for the US Biotechs industry at 17.5x.

- Analysts expect the number of shares outstanding to grow by 3.21% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.26%, as per the Simply Wall St company report.

Vericel Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Although Vericel has seen strong revenue growth, it is still experiencing net losses, with a net loss of $0.9 million in the latest quarter despite increased revenue, which could impact investor confidence and the company's overall profitability.

- Operating expenses are on the rise due to investments in MACI Arthro's development and marketing initiatives, which could affect net margins if revenue growth does not continue to outpace these expenses.

- Vericel's reliance on ongoing surgeon engagement and adoption in expanded target markets, such as arthroscopic surgeons, presents execution risks that could impact future revenue growth if these initiatives do not meet expectations.

- The unpredictable nature of Epicel's contribution to revenues, along with high quarterly variability, could lead to inconsistent financial performance and potential challenges in sustaining revenue growth.

- Macroeconomic factors, such as potential IV fluid shortages impacting hospital procedures, represent operational risks that could affect the adoption of Vericel's products and potentially impact revenues if hospitals prioritize other surgical procedures.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $65.43 for Vericel based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $72.0, and the most bearish reporting a price target of just $60.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $440.9 million, earnings will come to $64.5 million, and it would be trading on a PE ratio of 65.7x, assuming you use a discount rate of 6.3%.

- Given the current share price of $60.11, the analyst's price target of $65.43 is 8.1% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives