Last Update01 May 25Fair value Decreased 0.79%

AnalystConsensusTarget has increased revenue growth from 40.1% to 48.0%, decreased profit margin from 27.6% to 16.4% and increased future PE multiple from 21.4x to 35.7x.

Read more...Key Takeaways

- FILSPARI's expanded approval and ongoing studies position it for increased revenue from treating renal diseases, with potential market expansion from the new sNDA submission for FSGS.

- Progress in the pegtibatinase program and possible REMS changes offer growth opportunities through new revenue streams and enhanced market penetration and retention.

- Travere Therapeutics faces competitive risks in IgAN, financial pressure from net losses, and challenges from regulatory and generic market dynamics.

Catalysts

About Travere Therapeutics- A biopharmaceutical company, identifies, develops, and delivers therapies to people living with rare kidney and metabolic diseases in the United States.

- There is significant growth potential for FILSPARI as a foundational treatment for IgA nephropathy, given the expanded approval to treat a broader patient population and the strong profile demonstrating long-term efficacy and safety. This could lead to increased revenue as it becomes a more widely adopted therapy.

- The completion and submission of the supplementary New Drug Application (sNDA) for FILSPARI for potential use in treating FSGS around the end of the first quarter of 2025 might catalyze approval as the first-ever treatment specifically for FSGS, potentially expanding the market opportunity and positively impacting revenue growth.

- The upcoming results from ongoing studies of FILSPARI, including the SPARTAN study and other kidney disease studies, may further reinforce its efficacy and broaden its application, possibly driving higher revenue and market capture in treating renal diseases.

- Progress in the pegtibatinase program offers the potential for a first-in-kind disease-modifying therapy for HCU, which could bring additional revenue streams and diversify the company’s financial portfolio.

- Potential modifications to the REMS monitoring requirements for FILSPARI, if approved for quarterly liver monitoring rather than monthly, could ease the adoption process and enhance the patient experience, potentially improving both market penetration and retention rates, thereby impacting revenue positively.

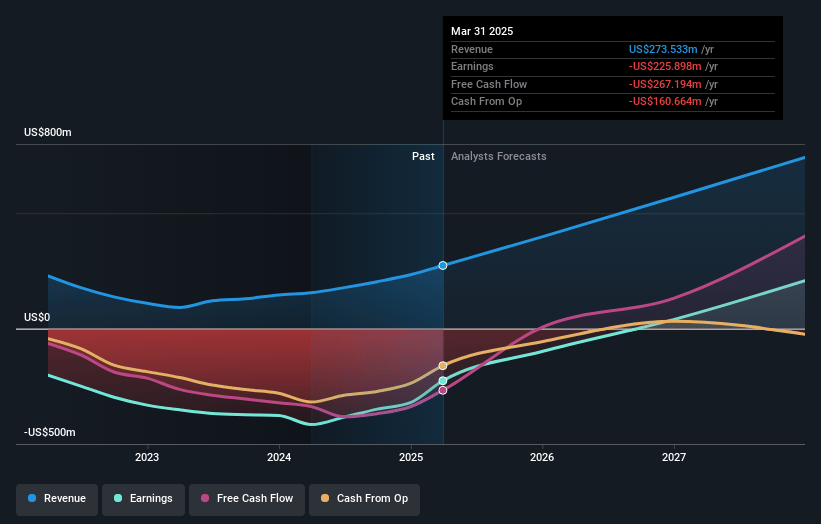

Travere Therapeutics Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Travere Therapeutics's revenue will grow by 48.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from -137.5% today to 16.4% in 3 years time.

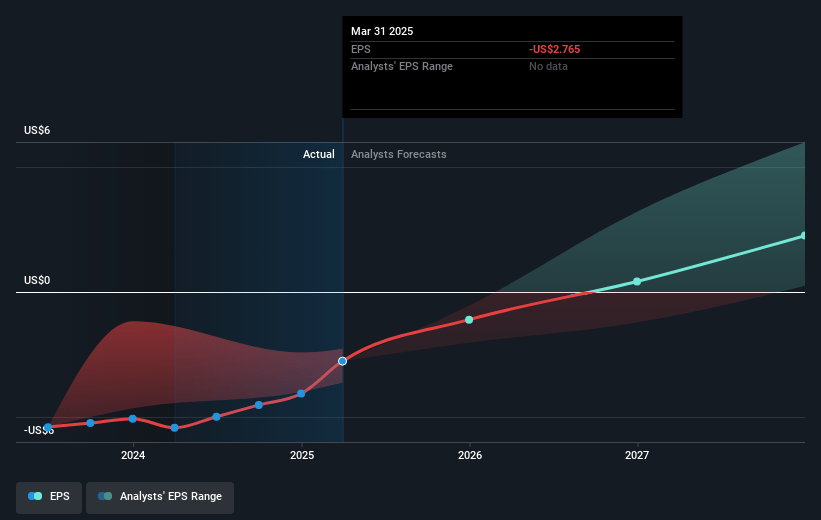

- Analysts expect earnings to reach $124.1 million (and earnings per share of $1.28) by about May 2028, up from $-320.6 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $237.5 million in earnings, and the most bearish expecting $37.7 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 35.7x on those 2028 earnings, up from -5.6x today. This future PE is greater than the current PE for the US Biotechs industry at 20.4x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.81%, as per the Simply Wall St company report.

Travere Therapeutics Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Travere Therapeutics faces the risk of new competition in the IgAN space, notably from companies like Novartis, which could affect FILSPARI's market share and impact future revenue growth.

- The net loss, despite strong sales growth, indicates financial pressure, highlighted by the reported net loss of $321.5 million for the full year 2024, which could impact net margins and earnings.

- Generic dynamics are affecting revenues from Thiola, and the company anticipates further headwinds in this area, reflecting potential declines in revenue from less diverse revenue streams.

- FILSPARI's REMS requirement, even if eased, still presents a barrier to broader adoption if not fully removed, potentially affecting revenue and limiting market opportunity.

- There is uncertainty around the future of the accelerated approval pathway in the IgAN space, as more therapies are now approved, potentially complicating future market entry and impacting revenue growth strategies.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $33.667 for Travere Therapeutics based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $47.0, and the most bearish reporting a price target of just $22.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $755.8 million, earnings will come to $124.1 million, and it would be trading on a PE ratio of 35.7x, assuming you use a discount rate of 6.8%.

- Given the current share price of $20.08, the analyst price target of $33.67 is 40.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.