Key Takeaways

- Successful ELEVIDYS launch and market penetration are key growth drivers, potentially bolstering future revenue significantly if market forecasts are achieved.

- Pipeline expansion and manufacturing innovations aim to diversify earnings and enhance net margins by improving cost efficiencies.

- Reliance on forward-looking statements, competition, and high expenses could impact revenue growth, profitability, and cash flow amid regulatory and technical challenges.

Catalysts

About Sarepta Therapeutics- A commercial-stage biopharmaceutical company, focuses on the discovery and development of RNA-targeted therapeutics, gene therapies, and other genetic therapeutic modalities for the treatment of rare diseases.

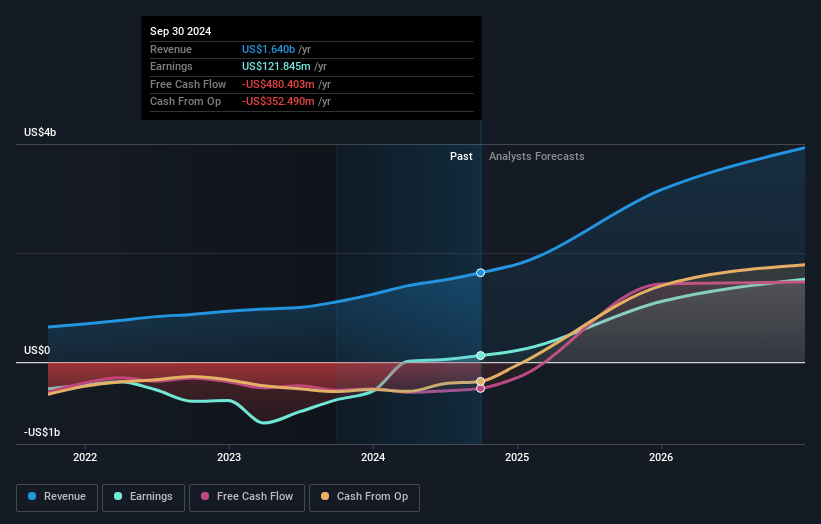

- Sarepta Therapeutics anticipates substantial revenue growth, projecting a 70% increase in total net product revenue in 2025, driven primarily by the exponential growth of their gene therapy ELEVIDYS, which is expected to see over 160% year-over-year growth. This forward-looking catalyst suggests that revenue could significantly increase if ELEVIDYS continues to perform strongly in the market.

- The successful launch and broad utilization of ELEVIDYS is seen as a key growth driver, expected to tap into less than 5% of the on-label addressable opportunity thus far. If the predicted significant market penetration unfolds, this could greatly bolster future revenue streams.

- Sarepta's collaboration with Arrowhead Pharmaceuticals expands its pipeline with siRNA programs, including several clinical and preclinical efforts across neuromuscular, CNS, cardiomyopathy, and pulmonary domains. The potential blockbuster launches before 2030 could diversify and grow earnings prospects.

- Innovations in manufacturing, such as the planned shift to suspension manufacturing, are expected to improve cost of goods sold (COGS) and thereby enhance net margins as Sarepta aims for significant yield efficiencies which could improve gross margins over 90% post-implementation.

- Anticipated approvals within the Limb-Girdle Muscular Dystrophy (LGMD) franchise, with potential LGMD launches contributing to future revenue, illustrate critical milestones that could serve as catalysts for revenue and earnings growth as these treatments gain approval and market entry over the next few years.

Sarepta Therapeutics Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Sarepta Therapeutics compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Sarepta Therapeutics's revenue will grow by 15.5% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 12.4% today to 21.1% in 3 years time.

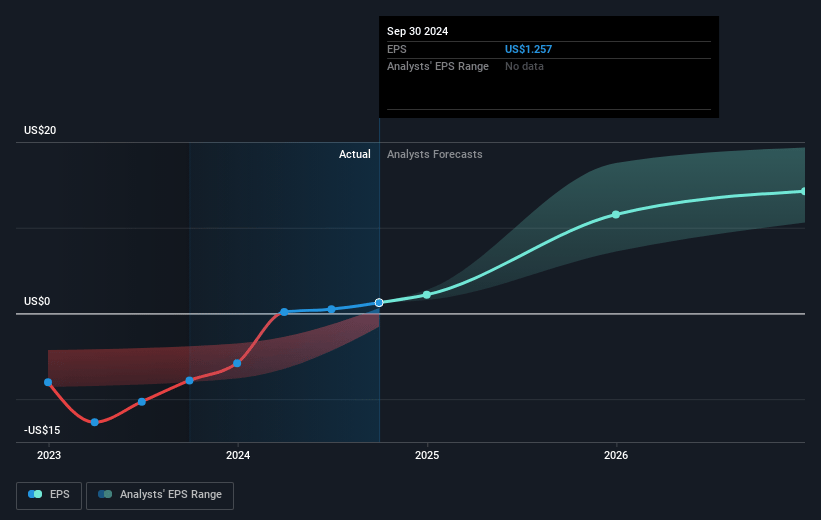

- The bearish analysts expect earnings to reach $616.4 million (and earnings per share of $5.12) by about April 2028, up from $235.2 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 21.3x on those 2028 earnings, down from 24.5x today. This future PE is greater than the current PE for the US Biotechs industry at 19.6x.

- Analysts expect the number of shares outstanding to grow by 2.65% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.77%, as per the Simply Wall St company report.

Sarepta Therapeutics Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- There are concerns over the reliance on forward-looking statements which involve many risks and uncertainties outside the company's control, potentially impacting future revenue and earnings.

- The success of ELEVIDYS and other therapies is contingent on overcoming technical and regulatory challenges, which could affect product launch timelines and ultimatley impact cash flow and operating income.

- Intense competition in gene therapy and RNA-interference spaces could limit Sarepta's market share and revenue growth.

- High R&D and SG&A expenses, particularly related to the Arrowhead transaction, could pressure net margins and decrease profitability.

- Changes in FDA policies and approval processes pose the risk of delays or denials, affecting revenue from new product approvals in the pipeline.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Sarepta Therapeutics is $103.81, which represents one standard deviation below the consensus price target of $147.33. This valuation is based on what can be assumed as the expectations of Sarepta Therapeutics's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $209.0, and the most bearish reporting a price target of just $70.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $2.9 billion, earnings will come to $616.4 million, and it would be trading on a PE ratio of 21.3x, assuming you use a discount rate of 6.8%.

- Given the current share price of $59.47, the bearish analyst price target of $103.81 is 42.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystLowTarget holds no position in NasdaqGS:SRPT. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.