Last Update01 May 25Fair value Decreased 0.96%

AnalystConsensusTarget made no meaningful changes to valuation assumptions.

Read more...Key Takeaways

- Strategic discontinuation of less promising programs and capital prioritization are expected to improve net margins and enhance commercial prospects.

- Promising therapies in Phase III studies are poised to drive revenue growth and market share capture upon expected launches between 2027 and 2030.

- Intellia Therapeutics faces uncertainties in gene-editing therapy adoption, high expenses, regulatory challenges, and competition, threatening revenue and financial stability.

Catalysts

About Intellia Therapeutics- A clinical-stage gene editing company, focuses on the development of curative genome editing treatments.

- Intellia’s focus on Phase III studies for NTLA-2002 in hereditary angioedema (HAE) and nex-z for transthyretin amyloidosis (ATTR) is expected to drive significant future revenue growth as these therapies approach commercial launch between 2027 and 2030.

- The company has optimized operational focus by discontinuing less promising programs, such as NTLA-3001, potentially improving net margins by allocating resources to high-value programs with greater commercial prospects.

- Intellia anticipates achieving a steady state of clinical expenses by 2026, with operating leverage and cost savings expected to lower overall operating expenses by 5–10% year-over-year, which should positively impact net margins.

- Strategic management of capital through prioritization and restructuring allows Intellia to invest in critical commercial infrastructure for NTLA-2002, enhancing revenue potential upon its launch in 2027.

- The promising clinical data for Intellia’s gene-editing therapies, evidenced by deep TTR reductions and potential functional cures, positions the company well to capture market share and enhance earnings as these therapies move towards regulatory submission and potential approval.

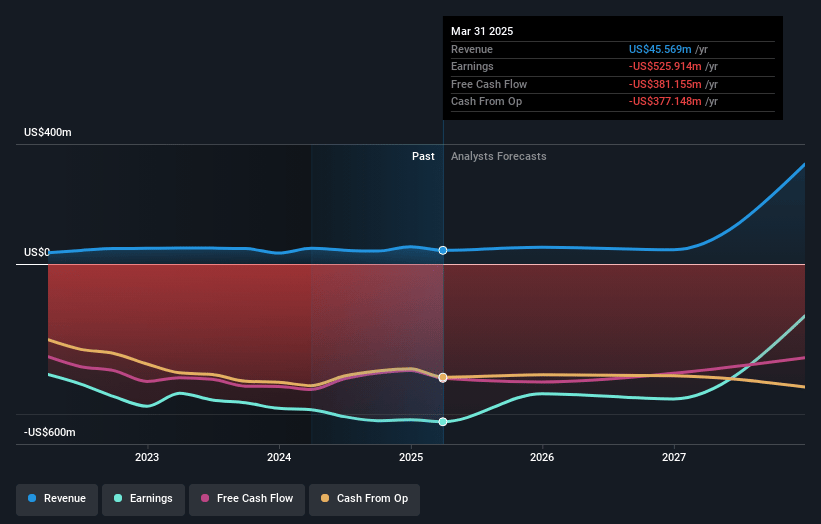

Intellia Therapeutics Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Intellia Therapeutics's revenue will grow by 78.5% annually over the next 3 years.

- Analysts are not forecasting that Intellia Therapeutics will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Intellia Therapeutics's profit margin will increase from -896.8% to the average US Biotechs industry of 15.9% in 3 years.

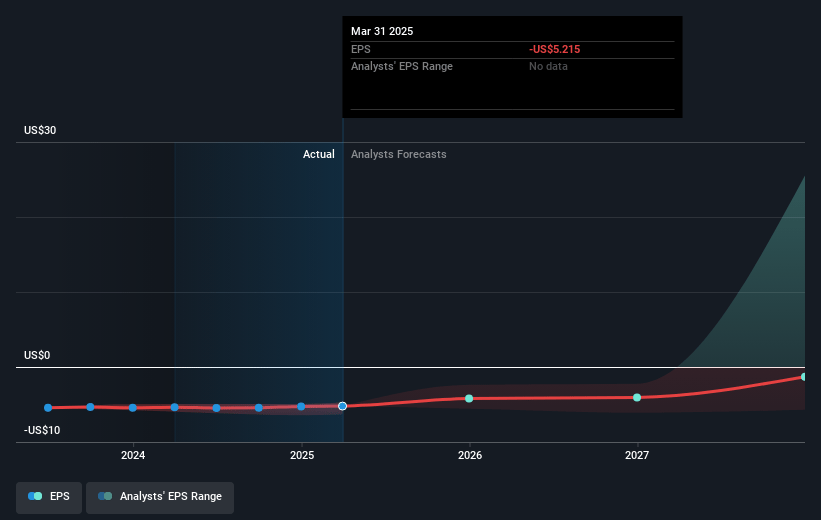

- If Intellia Therapeutics's profit margin were to converge on the industry average, you could expect earnings to reach $52.2 million (and earnings per share of $0.41) by about May 2028, up from $-519.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $2.3 billion in earnings, and the most bearish expecting $-729.0 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 122.9x on those 2028 earnings, up from -1.6x today. This future PE is greater than the current PE for the US Biotechs industry at 20.4x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.82%, as per the Simply Wall St company report.

Intellia Therapeutics Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Intellia Therapeutics faces uncertainty regarding the successful market adoption and competitive positioning of its gene-editing therapies, which could impact future revenue streams.

- The company's high operating expenses and ongoing need for significant investment in clinical trials and commercialization efforts raise concerns about potential pressure on net margins.

- Delays or failure in obtaining regulatory approvals for late-stage products, such as NTLA-2002 and nex-Z, could negatively impact projected timelines for revenue recognition.

- Intellia's reliance on a limited number of pivotal programs for future growth means any setbacks in these programs could substantially affect overall earnings and financial performance.

- Economic pressures related to restructuring costs and workforce reductions, along with potential competition from other TTR and HAE treatments, could affect the company's earnings trajectory and financial viability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $41.815 for Intellia Therapeutics based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $106.0, and the most bearish reporting a price target of just $8.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $329.2 million, earnings will come to $52.2 million, and it would be trading on a PE ratio of 122.9x, assuming you use a discount rate of 6.8%.

- Given the current share price of $8.2, the analyst price target of $41.81 is 80.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.