Key Takeaways

- Focus on high-value vaccines and approvals in respiratory and combination categories could significantly boost revenue diversification and market presence.

- Strategic acquisitions and operational improvements promise enhanced net margins through significant cost efficiencies and savings in the next few years.

- Uncertain product approval, new market conditions, and declining vaccine demand challenge Moderna's revenue stability, risking earnings and future sales growth.

Catalysts

About Moderna- A biotechnology company, provides messenger RNA medicines in the United States, Europe, and internationally.

- Moderna anticipates a significant impact on revenue and diversification from its focus on ten high-value programs, including new vaccines such as respiratory, combination (flu and COVID), and RSV vaccines, with expected approvals over the next three years targeting a market of over $30 billion.

- The approval of mRESVIA and upcoming new product launches present substantial growth opportunities, potentially leading to improved earnings from increased market presence and commercial performance.

- Moderna’s strategic acquisition and operational improvements, including $2.6 billion in cost savings from 2024 and further cost efficiencies planned through 2025 and 2026, are expected to enhance net margins by reducing cash costs significantly.

- Successful late-stage trial data and ongoing regulatory filings, such as the PDUFA dates for the next-gen COVID vaccine and RSV in 2025, could boost future sales and revenue, particularly if these products achieve approval and capture market share.

- Moderna’s pipeline in oncology and rare diseases, with promising trial results, underscores potential future earnings growth as these therapies advance towards regulatory approvals and commercialization, broadening the company's product portfolio and revenue streams.

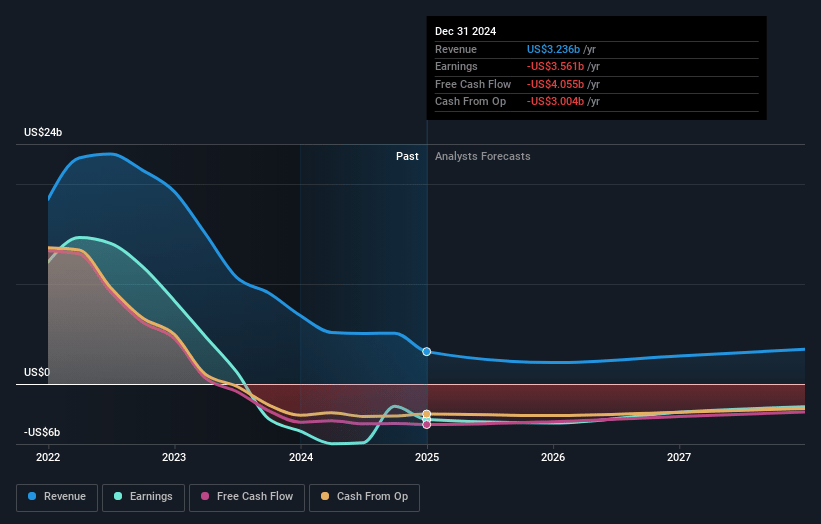

Moderna Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Moderna compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Moderna's revenue will grow by 35.3% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from -110.0% today to 6.3% in 3 years time.

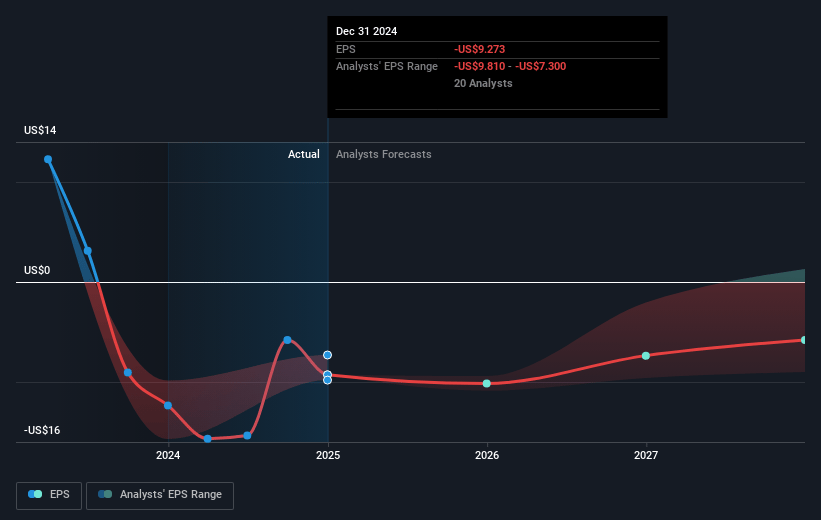

- The bullish analysts expect earnings to reach $503.1 million (and earnings per share of $1.31) by about April 2028, up from $-3.6 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 120.1x on those 2028 earnings, up from -2.8x today. This future PE is greater than the current PE for the US Biotechs industry at 19.6x.

- Analysts expect the number of shares outstanding to grow by 0.67% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.5%, as per the Simply Wall St company report.

Moderna Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Moderna has experienced a significant decline in revenue, down 53% from 2023, driven by lower product sales and decreased demand for COVID vaccines, which could impact future revenue stability and growth.

- With a reported net loss of $3.6 billion for 2024 and guidance suggesting further losses in 2025, sustaining this level of operating cost amidst uncertain product approval and market conditions poses a substantial risk to earnings.

- The competitive market environment, especially for COVID and respiratory vaccines, along with uncertainties in vaccination rates, are expected to result in a broad revenue guidance range for 2025. This unpredictability introduces risk to realizing revenues at the higher end of their expectations.

- The phaseout of advanced purchase agreements, without a strong replacement revenue stream or significant product revenue from newly approved products, could lead to sustained pressure on Moderna's topline performance, affecting revenue.

- With ongoing regulatory challenges, such as the clinical hold on the Norovirus vaccine trial due to a safety event, and potential delays in product approvals, there is significant risk to the market launch schedule, impacting future sales and cash flows.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Moderna is $127.01, which represents two standard deviations above the consensus price target of $50.92. This valuation is based on what can be assumed as the expectations of Moderna's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $212.0, and the most bearish reporting a price target of just $20.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be $8.0 billion, earnings will come to $503.1 million, and it would be trading on a PE ratio of 120.1x, assuming you use a discount rate of 6.5%.

- Given the current share price of $25.74, the bullish analyst price target of $127.01 is 79.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystHighTarget holds no position in NasdaqGS:MRNA. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.