Narratives are currently in beta

Key Takeaways

- Promising pipelines and product innovations could boost future revenues significantly, addressing unmet medical needs and improving margins.

- Strategic collaborations and focused operational growth efforts aim to enhance revenue and earnings through efficiencies and market expansions.

- MannKind faces challenges in NTM product development, competition with Insmed, potential safety concerns in its pipeline, and shifts in diabetes market focus.

Catalysts

About MannKind- A biopharmaceutical company, focuses on the development and commercialization of inhaled therapeutic products for endocrine and orphan lung diseases in the United States.

- MannKind has promising pipeline opportunities, including the Phase I completion of TENA and ongoing Phase III trials for clofazimine inhalation studies, which target unmet needs in NTM lung disease. Successful outcomes here could significantly boost future revenues.

- The potential success of the pediatric approval for Afrezza could open up a market of over 300,000 children with type 1 diabetes, potentially increasing net revenues significantly if a portion of this market is captured.

- The launch and expansion of innovative products like nintedanib DPI, leveraging MannKind's Technosphere technology platform, could address issues like severe GI side effects seen with current treatments, potentially improving net margins and revenue streams.

- The Tyvaso DPI collaboration with United Therapeutics is a strong revenue driver, with royalties and manufacturing activities contributing significantly to income. Continued patient uptake and price increases could enhance earnings growth.

- Strategic alignment for more focused operational growth, including the restructuring of the sales force to concentrate on profitable expansions like Afrezza, aims to increase efficiency and net margins while driving future revenue growth.

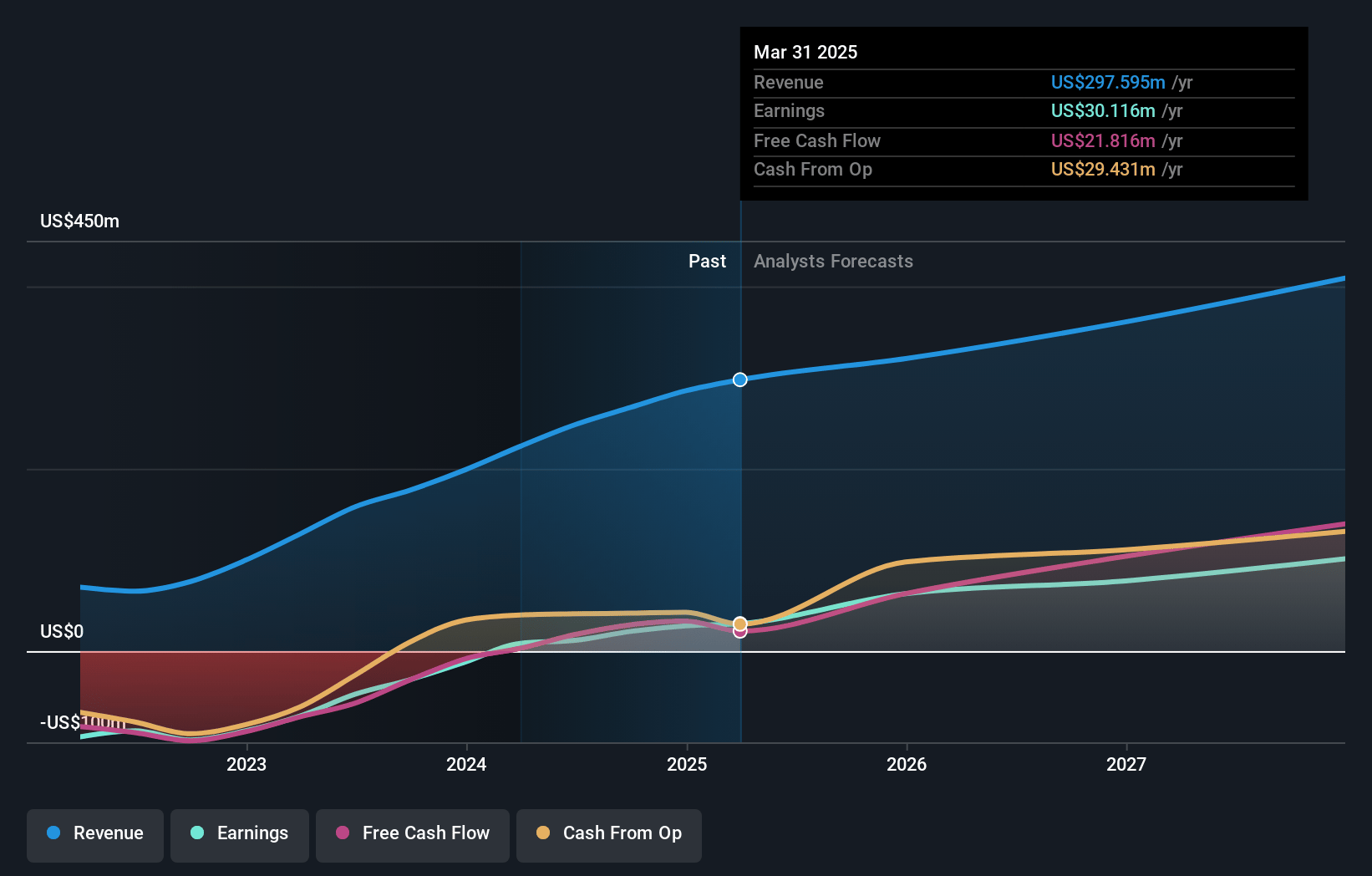

MannKind Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming MannKind's revenue will grow by 14.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 8.1% today to 28.1% in 3 years time.

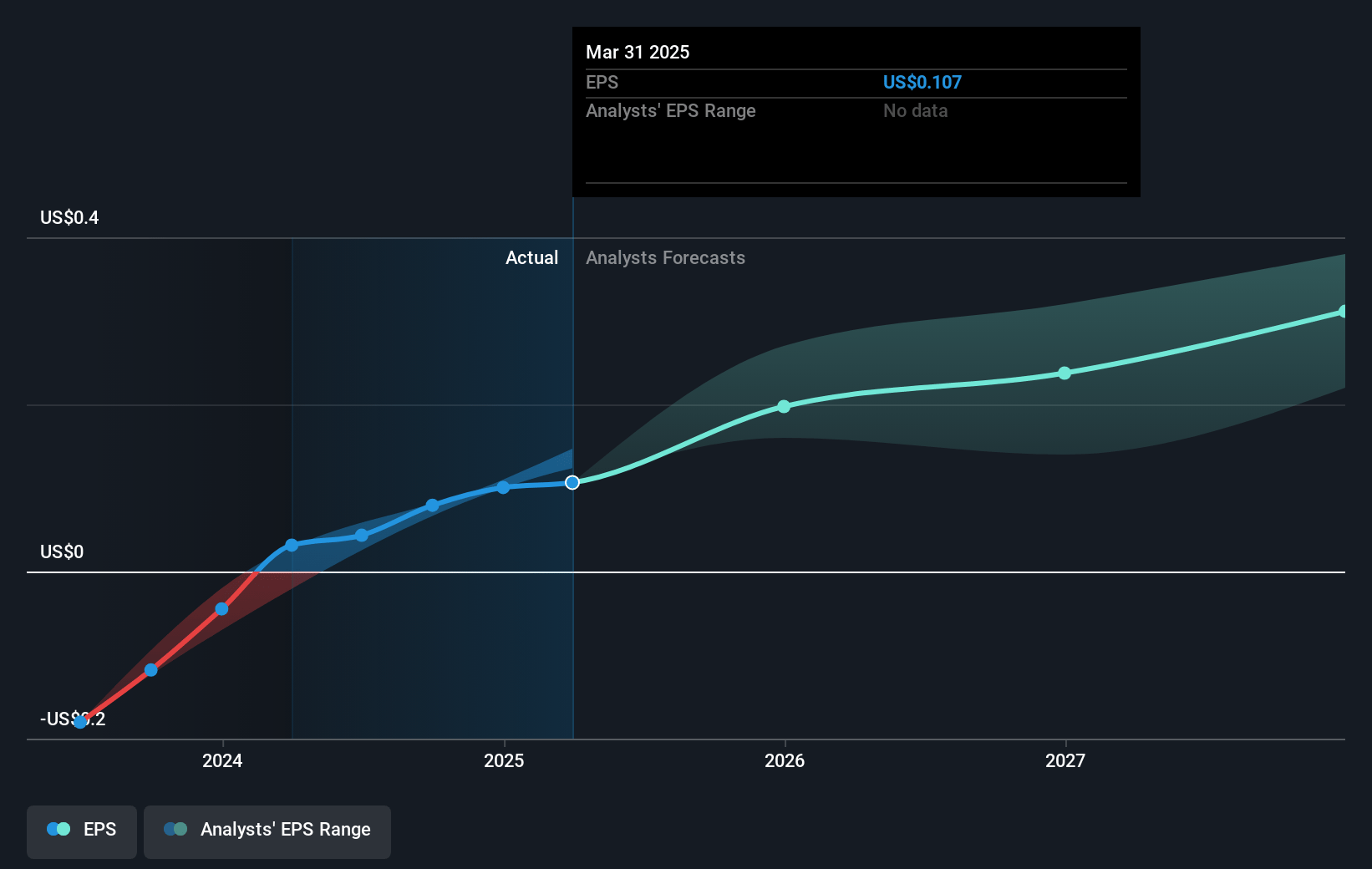

- Analysts expect earnings to reach $113.9 million (and earnings per share of $0.39) by about December 2027, up from $21.6 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $146 million in earnings, and the most bearish expecting $65.6 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 30.4x on those 2027 earnings, down from 86.2x today. This future PE is greater than the current PE for the US Biotechs industry at 15.4x.

- Analysts expect the number of shares outstanding to grow by 2.15% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.48%, as per the Simply Wall St company report.

MannKind Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- There is a risk that other companies have failed in developing treatments for NTM, which may signal potential difficulties for MannKind in successfully completing its trials, potentially impacting future revenues from unsuccessful product development.

- The company faces competition from Insmed in the NTM space, which could affect its market share and revenue growth if MannKind's offerings are not sufficiently differentiated or if Insmed captures more of the market.

- Recent changes like the sales force restructuring and adjustments made to manage V-Go for profitability have caused hiccups, which might impact Afrezza's revenue growth if similar issues arise in the future.

- Potential safety concerns or side effects related to new products like clofazimine-101 inhalation and MNKD-201 could delay or obstruct clinical approval, potentially impacting MannKind's revenue if their pipeline fails to meet regulatory or market expectations.

- The market for diabetes-related products could be affected by shifts in focus from diabetes treatments to weight loss treatments, impacting Afrezza's demand and subsequent revenue.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $9.8 for MannKind based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $12.0, and the most bearish reporting a price target of just $9.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $405.5 million, earnings will come to $113.9 million, and it would be trading on a PE ratio of 30.4x, assuming you use a discount rate of 6.5%.

- Given the current share price of $6.74, the analyst's price target of $9.8 is 31.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives