Key Takeaways

- Strategic partnerships and tech collaborations are anticipated to boost revenue streams, improve net margins, and enhance operational efficiency.

- Relocation to Austin and a focus on AI-driven platforms aim to streamline operations, increase profitability, and access new growth opportunities.

- Capital constraints, increased expenses, and risks in partnerships and divestitures could challenge IPA's revenue growth and operational efficiency.

Catalysts

About ImmunoPrecise Antibodies- A techbio company, engages in the development of therapeutic antibodies.

- The strategic partnership valued at USD 8 million to USD 10 million utilizing proprietary B Cell Select technology and AI-driven capabilities is anticipated to significantly boost recurring commercial revenue, positively impacting future revenue streams.

- Collaborations with technology partners like Vultr and AMD aim to enhance the lab-in-a-loop drug discovery capabilities, driving cost effectiveness and competitiveness, which may improve net margins by lowering operational costs and boosting efficiency.

- The 131.8% year-over-year revenue increase in BioStrand, with a gross profit margin of 97%, indicates strong potential for high profitability, thus likely having a significant positive impact on future earnings.

- The relocation of headquarters to Austin, Texas—a burgeoning AI and biotech hub—positions the company to capitalize on an expanding ecosystem, potentially leading to increased revenue through better access to partnerships and talent.

- The planned divestiture of EU operations, coupled with a focus on AI-driven platforms, seeks to streamline operations and reduce costs, which could improve net margins and enhance profitability.

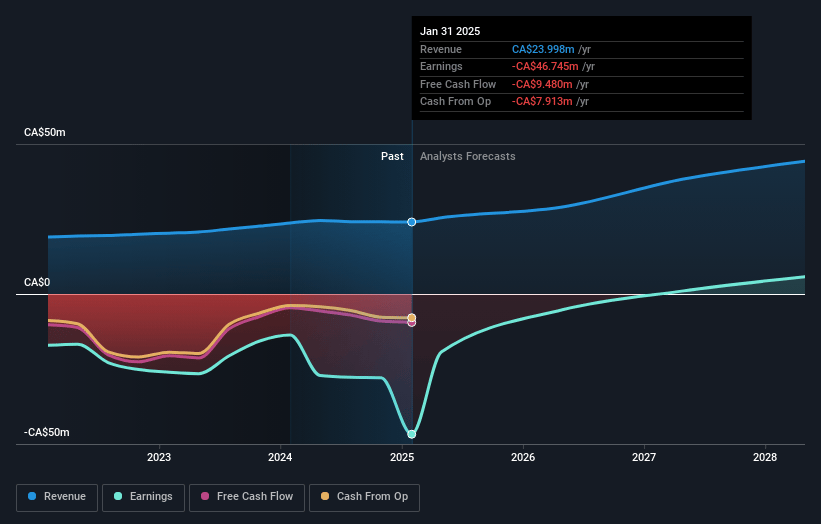

ImmunoPrecise Antibodies Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming ImmunoPrecise Antibodies's revenue will grow by 21.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from -194.8% today to 10.8% in 3 years time.

- Analysts expect earnings to reach CA$4.6 million (and earnings per share of CA$0.1) by about July 2028, up from CA$-46.7 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 81.5x on those 2028 earnings, up from -2.4x today. This future PE is greater than the current PE for the CA Life Sciences industry at 35.3x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.0%, as per the Simply Wall St company report.

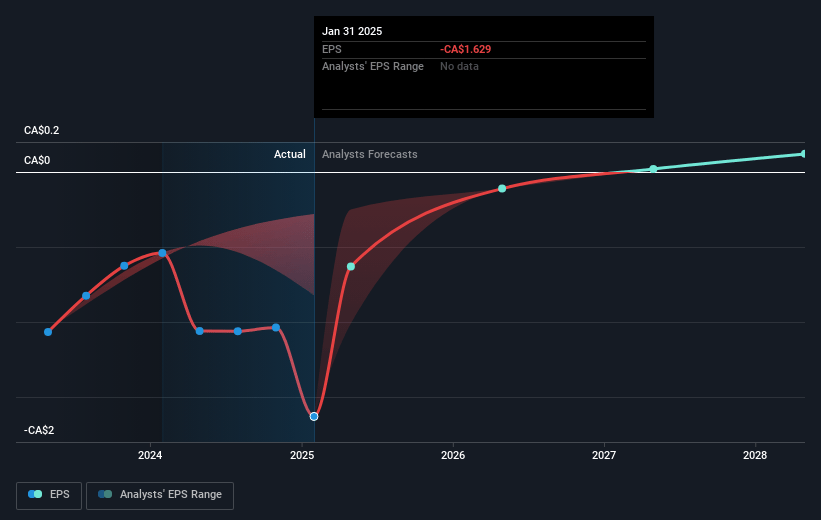

ImmunoPrecise Antibodies Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The biotech industry has recently faced significant capital constraints, with many companies, including larger ones, filing for bankruptcy, which could hinder IPA's ability to secure funding and impact revenue growth.

- IPA has experienced an operating expense increase, with a noncash impairment charge on BioStrand's intangible assets, which could negatively affect net margins and profitability.

- The successful financial execution of strategic partnerships and AI initiatives relies heavily on technical and operational integration, posing risks if these integrations do not result in anticipated revenue increases or cost savings.

- External collaborations and partnerships, while beneficial, introduce risks related to dependency on other companies' technologies and market conditions, which can impact IPA's revenue and earnings if these partnerships do not perform as expected.

- The company is undergoing a divestiture of its European operations, which could temporarily impact revenues and operational capacity, and the anticipated cost savings or reinvestment returns might not materialize as planned.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $4.0 for ImmunoPrecise Antibodies based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $5.0, and the most bearish reporting a price target of just $3.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CA$42.8 million, earnings will come to CA$4.6 million, and it would be trading on a PE ratio of 81.5x, assuming you use a discount rate of 7.0%.

- Given the current share price of $1.82, the analyst price target of $4.0 is 54.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.