Narratives are currently in beta

Key Takeaways

- Strategic ENHANZE expansions and new licensing agreements are poised to boost royalty revenue and long-term growth prospects.

- Approval of key partnerships, including subcutaneous formulations, underscores potential for significant future royalty revenue increases.

- Dependence on major partners for royalties, competitive market pressures, and legal risks threaten financial stability and growth opportunities for Halozyme Therapeutics.

Catalysts

About Halozyme Therapeutics- A biopharma technology platform company, researches, develops, and commercializes proprietary enzymes and devices in the United States, Switzerland, Belgium, Japan, and internationally.

- The expansion of the ENHANZE drug delivery technology with multiple new target nominations and expanded licensing agreements is a strong catalyst for future milestone payments and royalty revenue growth.

- Ongoing regulatory approvals and increasing market penetration of partnered products like TECENTRIQ and OCREVUS subcutaneous with ENHANZE suggest a significant potential for revenue growth via conversion from intravenous to subcutaneous formulations.

- The increasing adoption and expected growth of products like DARZALEX, Phesgo, and VYVGART, with projected significant sales growth, indicate a robust long-term revenue stream for Halozyme from royalty payments.

- Future potential approvals of high-revenue partnerships, such as Bristol-Myers Squibb's nivolumab subcutaneous with ENHANZE, could lead to an increase in the company’s royalty revenue.

- The strategic expansion into new intellectual property licensing opportunities, such as the MDASE patents, may offer additional revenue streams and enhance their competitive position, potentially increasing overall earnings.

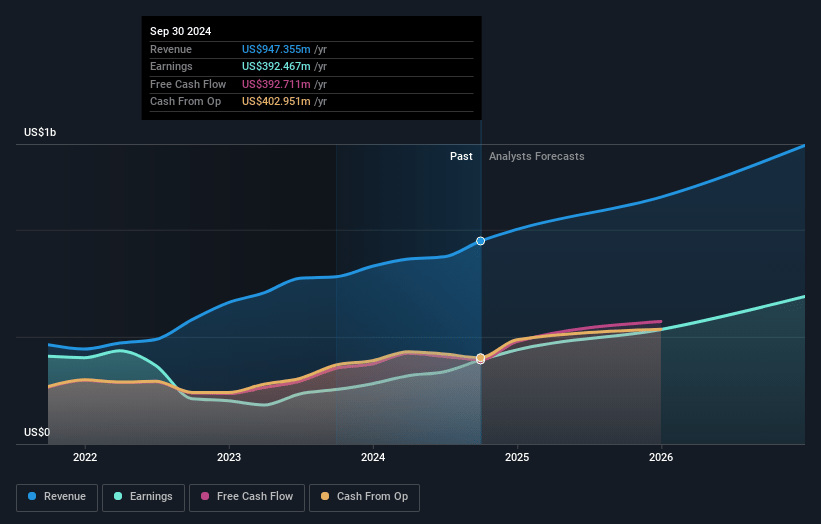

Halozyme Therapeutics Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Halozyme Therapeutics's revenue will grow by 18.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 41.4% today to 51.7% in 3 years time.

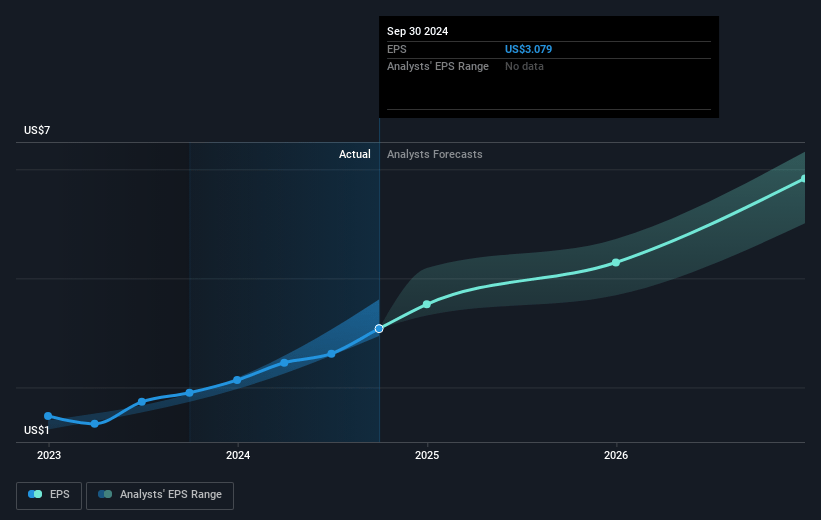

- Analysts expect earnings to reach $820.2 million (and earnings per share of $6.88) by about December 2027, up from $392.5 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 11.2x on those 2027 earnings, down from 15.8x today. This future PE is lower than the current PE for the US Biotechs industry at 16.6x.

- Analysts expect the number of shares outstanding to decline by 2.15% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.6%, as per the Simply Wall St company report.

Halozyme Therapeutics Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Dependence on key partners such as Roche and Johnson & Johnson for royalty revenues could pose a risk, as any change in partnership dynamics or performance of partner products like DARZALEX and Phesgo could negatively impact revenue streams.

- The reliance on expansion through licensing and collaboration deals implies execution risk; failure to secure new deals or successfully expand existing agreements could limit future revenue growth opportunities.

- Potential delays or denials in regulatory approvals, especially for promising products pending in new markets or for new indications, could hinder anticipated revenue and earnings growth.

- Significant portion of revenues comes from royalty streams on products in highly competitive therapeutic markets; increasing competition could pressure partner sales, thereby affecting Halozyme's royalty income.

- Legal and patent risks associated with their MDASE platform and IP licensing strategy could introduce financial uncertainty if patent claims are challenged or licensing opportunities underperform expectations.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $64.0 for Halozyme Therapeutics based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $75.0, and the most bearish reporting a price target of just $52.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $1.6 billion, earnings will come to $820.2 million, and it would be trading on a PE ratio of 11.2x, assuming you use a discount rate of 6.6%.

- Given the current share price of $48.6, the analyst's price target of $64.0 is 24.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives