Key Takeaways

- Strategic acquisitions could lead to future margin growth despite initial EPS dilution, unlocking significant market opportunities.

- U.S. NIH funding uncertainties and reliance on backlog might suppress short-term revenue growth expectations.

- Geopolitical risks, FX challenges, and strategic acquisitions pressure Bruker's margins and profits, with cautious optimism for long-term improvements amidst current uncertainties.

Catalysts

About Bruker- Develops, manufactures, and distributes scientific instruments, and analytical and diagnostic solutions in the United States, Europe, the Asia Pacific, and internationally.

- Bruker's strategic acquisitions in spatial biology, molecular diagnostics, and lab automation are initially leading to margin and EPS dilution, but they unlock very large market opportunities and improve the margin potential, suggesting modest future revenue and margin growth.

- The company's expectation of organic revenue growth of 3% to 4%, which is slightly above market expectation, coupled with M&A contributions, might create cautious optimism about future earnings, leading to measured EPS growth forecasts given potential uncertainties.

- There is anticipated good order momentum from the China stimulus program, adding potential revenue certainty, though subdued due to its spread over several quarters rather than an immediate revenue influx.

- U.S. NIH funding and academic market uncertainties are known headwinds, woven into their guidance. Yet, declining funding could suppress Bruker's expected revenue growth and place pressure on net margins.

- The company maintains a strong backlog, which could mitigate some risk from unforeseen revenue dips. However, assumptions of flat Q1 organic growth and eventual reliance on backlog for future stability suggests tempered revenue expectations in the short term.

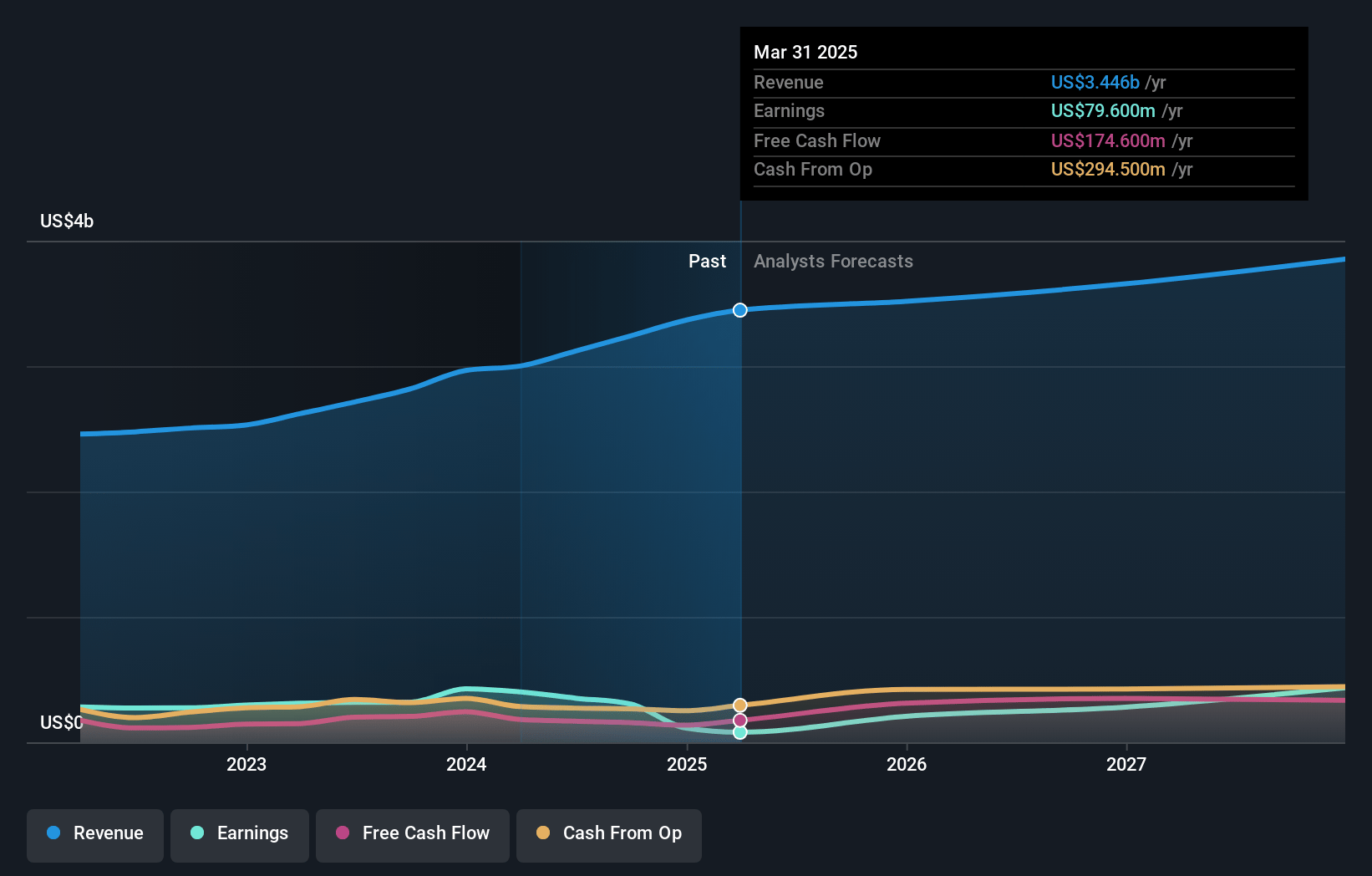

Bruker Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Bruker compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Bruker's revenue will grow by 4.7% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 3.4% today to 11.0% in 3 years time.

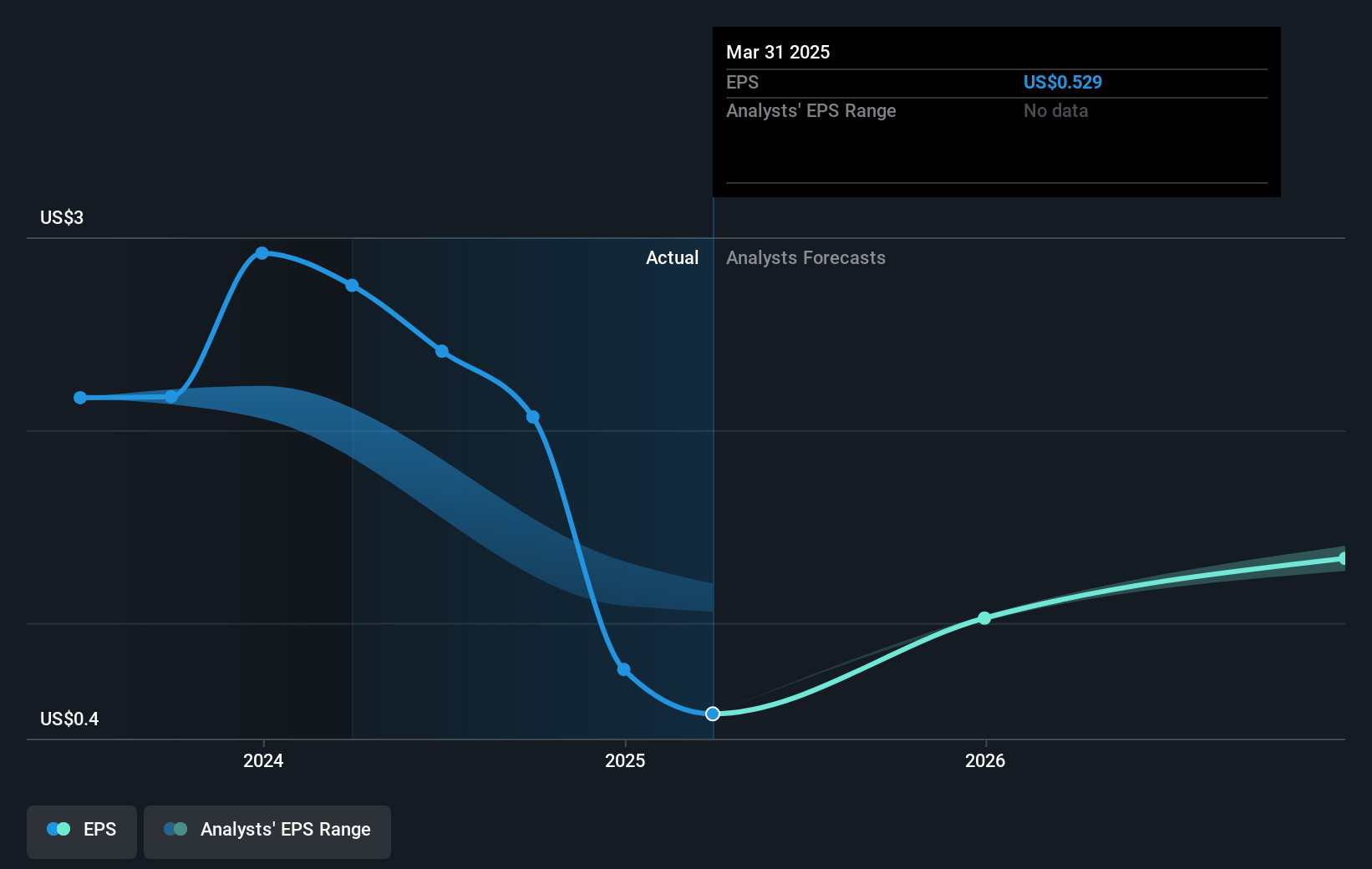

- The bearish analysts expect earnings to reach $423.1 million (and earnings per share of $3.17) by about April 2028, up from $113.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 25.4x on those 2028 earnings, down from 50.8x today. This future PE is lower than the current PE for the US Life Sciences industry at 36.5x.

- Analysts expect the number of shares outstanding to grow by 4.38% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.56%, as per the Simply Wall St company report.

Bruker Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company faces geopolitical risks and market demand uncertainties, specifically in relation to the U.S.-based NIH and academic government market, which could lead to reductions in life science research investments. This could negatively affect Bruker's revenue and profit margins if funding levels decrease or remain uncertain.

- There is a noted potential margin and EPS dilution from strategic mergers and acquisitions. Although these are aimed at unlocking new market opportunities, the initial costs could negatively impact Bruker's earnings and profitability in the short-term.

- During the conference call, the management highlighted that the fourth quarter of 2024 faced a foreign exchange headwind of 1.2%. Continued FX challenges could negatively impact Bruker's revenues and net margins by affecting the reported financial results.

- There is admitted uncertainty in the U.S. government research funding environment, particularly NIH funding, which although currently less than 5% of Bruker's revenue, could become a headwind if funding cuts occur. This could pressurize revenue growth and potentially offset gains made in other growing segments.

- Bruker has outlined an intentional step back in operating margins to reassess strategic acquisitions, potentially leading to subdued earnings growth in the near term. This limits the immediate expansion of net margins despite a commitment to long-term operating profit margin improvements.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Bruker is $50.18, which represents one standard deviation below the consensus price target of $60.13. This valuation is based on what can be assumed as the expectations of Bruker's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $80.0, and the most bearish reporting a price target of just $45.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $3.9 billion, earnings will come to $423.1 million, and it would be trading on a PE ratio of 25.4x, assuming you use a discount rate of 7.6%.

- Given the current share price of $37.89, the bearish analyst price target of $50.18 is 24.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystLowTarget holds no position in NasdaqGS:BRKR. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.