Key Takeaways

- Expansion in respiratory offerings and physician sampling programs is poised to boost revenue through enhanced market presence and demand capitalization.

- Strategic focus on high-value pipeline products and biosimilars positions Amphastar for significant future growth in advanced therapeutic areas.

- Amphastar faces challenges with competition, distribution disruptions, rising costs, and regulatory delays impacting revenue, margins, and future growth.

Catalysts

About Amphastar Pharmaceuticals- A bio-pharmaceutical company, develops, manufactures, markets, and sells generic and proprietary injectable, inhalation, and intranasal products in the United States, China, and France.

- The expansion of Amphastar's physician sampling program and sales force for Primatene MIST and BAQSIMI is expected to drive revenue growth by reaching more primary care physicians and enhancing these products' market presence.

- The launch of the albuterol MDI product is a significant expansion in Amphastar’s respiratory offerings and is likely to enhance revenue by allowing the company to capitalize on the demand for asthma management solutions.

- Amphastar's forthcoming pipeline products, such as AMP-002, teriparatide, AMP-007, and the GLP-1 ANDA, represent significant growth opportunities. These are anticipated to positively impact earnings as they potentially capture market share in high-value categories.

- The introduction of AMP-028, a new biosimilar with a $2 billion market potential, suggests a strategic focus on advanced therapeutic areas. This could lead to revenue increases and support sustainable growth by leveraging Amphastar's unique market capabilities.

- The refiling of the BLA for Insulin Aspart and priority review for the GLP-1 ANDA indicates potential future revenue streams from the diabetes portfolio. This represents a strategic move into high-demand treatment areas that can drive earnings growth.

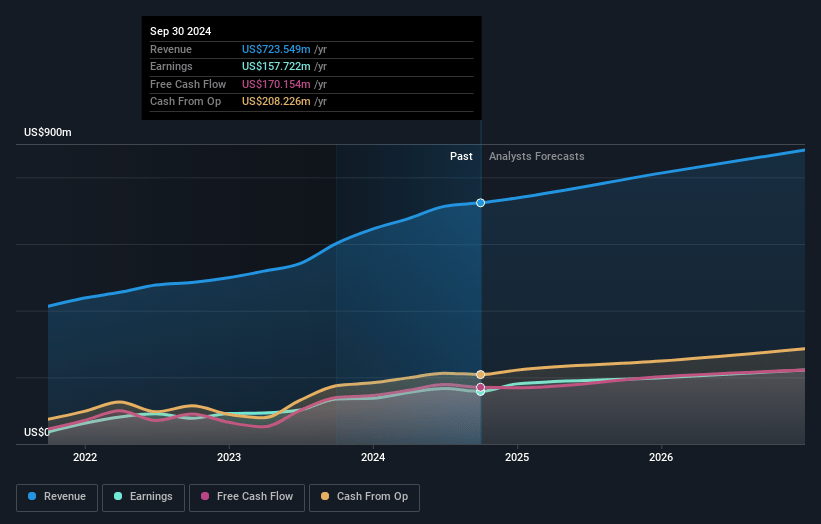

Amphastar Pharmaceuticals Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Amphastar Pharmaceuticals's revenue will grow by 9.4% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 21.8% today to 21.1% in 3 years time.

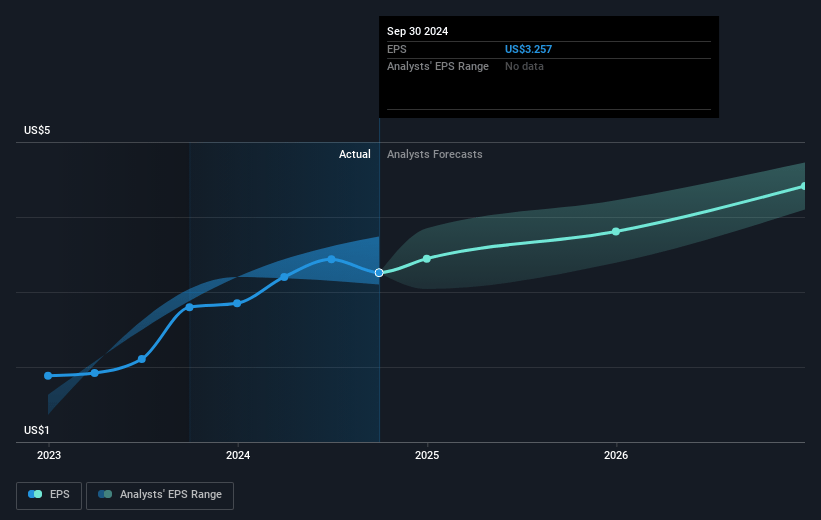

- Analysts expect earnings to reach $200.1 million (and earnings per share of $3.71) by about January 2028, up from $157.7 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $248.0 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 17.8x on those 2028 earnings, up from 11.3x today. This future PE is lower than the current PE for the US Pharmaceuticals industry at 19.0x.

- Analysts expect the number of shares outstanding to grow by 3.85% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.92%, as per the Simply Wall St company report.

Amphastar Pharmaceuticals Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The launch of Amphastar's albuterol MDI product is entering a competitive asthma management market, which could impact revenue and profit margins if they are unable to capture significant market share.

- Increased competition in the glucagon injection kit market has already led to a 9% decline in sales, which could further pressure revenues and gross margins if they cannot maintain their competitive position.

- The transition of distribution responsibilities for BAQSIMI resulted in temporary supply disruptions, notably in 14 European countries, potentially impacting revenues and earnings as they transition and grow this part of the business.

- Higher costs, including increased labor costs, component costs, and expanded selling and marketing expenses for BAQSIMI, led to a decrease in gross margins from 60% to 53%, possibly affecting net income if expenses continue to rise faster than sales.

- Regulatory challenges, including delays in the approval process for products such as AMP-002 and AMP-007, may hinder the ability to generate revenue from these products, impacting future growth and financial performance.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $56.4 for Amphastar Pharmaceuticals based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $66.0, and the most bearish reporting a price target of just $46.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $946.8 million, earnings will come to $200.1 million, and it would be trading on a PE ratio of 17.8x, assuming you use a discount rate of 5.9%.

- Given the current share price of $37.12, the analyst's price target of $56.4 is 34.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives