Key Takeaways

- Appointing a new CEO with drug launch expertise may enhance strategic execution and sales growth, strengthening revenue and net margins.

- Expanding drug pipeline and international reach can significantly boost revenue, supported by strategic branding efforts and market introductions.

- Execution risks and underinvestment in R&D could hinder pipeline growth, while increased SG&A and strategic alliances carry financial and margin impact concerns.

Catalysts

About ACADIA Pharmaceuticals- A biopharmaceutical company, focuses on the development and commercialization innovative medicines that address unmet medical needs in central nervous system (CNS) disorders and rare diseases in the United States.

- The recent appointment of Catherine Owen Adams as CEO, with her extensive experience in drug launches, is seen as a potential catalyst for strategic execution and growth in sales, including those of rare disease therapies, which could positively impact revenue and potentially net margins.

- DAYBUE's ongoing expansion outside the U.S., including recent approval in Canada and potential launches in Europe and Japan, is expected to drive significant revenue growth in the medium term.

- Advances in ACADIA’s pipeline, particularly ACP-101 for Prader-Willi syndrome and ACP-204 for Alzheimer’s psychosis, represent opportunities for expanding market presence and increasing long-term revenue and earnings through new drug approvals and market introductions.

- The launch of consumer awareness and branded campaigns, notably involving celebrities, aims to increase NUPLAZID adoption, potentially leading to an increase in annual revenue and earnings as patient numbers grow.

- Strategic business development efforts to expand the pipeline further could lead to new high-value assets, strengthening future revenue streams and overall earnings potential by broadening the company’s product offering.

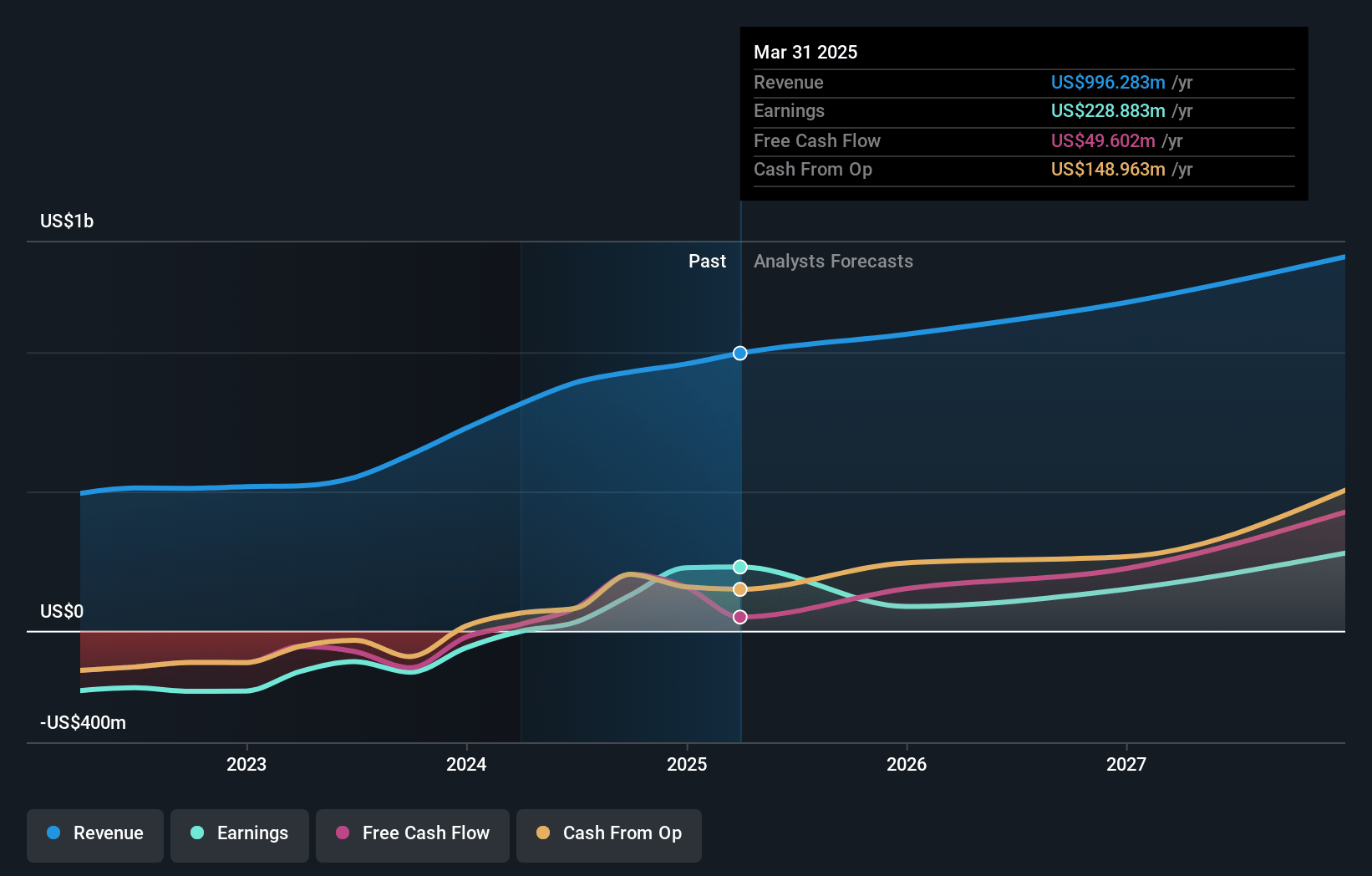

ACADIA Pharmaceuticals Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming ACADIA Pharmaceuticals's revenue will grow by 10.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 13.8% today to 21.3% in 3 years time.

- Analysts expect earnings to reach $265.3 million (and earnings per share of $1.42) by about January 2028, up from $128.5 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $391.2 million in earnings, and the most bearish expecting $74.1 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 21.1x on those 2028 earnings, down from 23.8x today. This future PE is greater than the current PE for the US Biotechs industry at 17.5x.

- Analysts expect the number of shares outstanding to grow by 4.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.23%, as per the Simply Wall St company report.

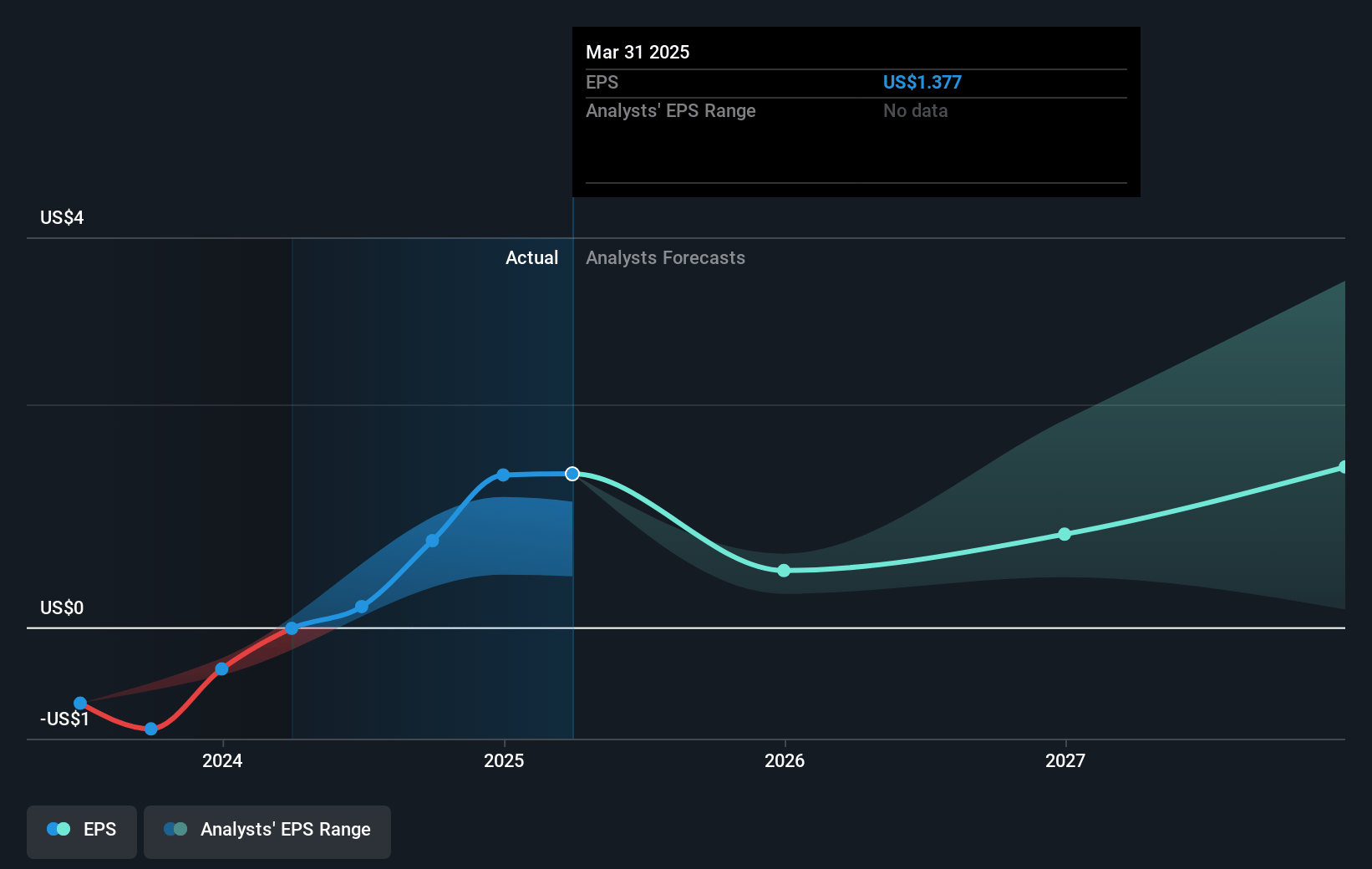

ACADIA Pharmaceuticals Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The execution risk associated with DAYBUE involves complex launches that require coordination in multiple countries, which poses a challenge and could hinder revenue growth if the process doesn't go smoothly.

- Despite increasing sales for DAYBUE, 70% of Rett patients are treated outside centers of excellence, which could limit market penetration and affect revenue growth if not addressed effectively.

- R&D expenses have decreased significantly, which could imply potential underinvestment in future product development, impacting long-term earnings by limiting pipeline growth.

- The increase in SG&A expenses due to campaigns and CEO transitions might reduce net margins if sales growth does not offset these higher costs quickly enough.

- There are significant financial and strategic risks associated with business development activities, particularly if future acquisitions or partnerships, like the one with Neuren for trofinetide, do not perform as expected, potentially impacting earnings and net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $24.95 for ACADIA Pharmaceuticals based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $39.0, and the most bearish reporting a price target of just $11.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.2 billion, earnings will come to $265.3 million, and it would be trading on a PE ratio of 21.1x, assuming you use a discount rate of 6.2%.

- Given the current share price of $18.4, the analyst's price target of $24.95 is 26.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives