Key Takeaways

- Competitive pressures and opt-in trials risk reducing conversion rates and subscription revenue growth, particularly among younger consumers.

- New marketing strategies and cost savings may improve margins but face challenges like increased churn and restricted subscriber growth.

- SiriusXM's strategic focus on margins, subscriber retention, and digital expansion, alongside cost efficiency, aims to sustain growth in revenue and free cash flow.

Catalysts

About Sirius XM Holdings- Operates as an audio entertainment company in North America.

- Sirius XM Holdings is expected to experience pressure on conversion rates, particularly from younger consumers and competitive streaming services, which could negatively impact future subscription revenue growth.

- The shift to opt-in trials in Tesla models may lead to lower conversion rates, affecting the overall revenue forecast in the near term.

- Limitations in subscriber growth, particularly with the anticipated negative net adds due to onetime impacts like click to cancel and reduced streaming marketing, suggest revenue and earnings may face headwinds in 2025.

- The implementation of new marketing strategies and pricing adjustments, while aimed at improving long-term margins, may initially increase churn and reduce short-term revenue growth expectations.

- Cost savings efforts, while potentially bolstering net margins, may not fully offset the impact of lower revenue projections and ongoing competitive pressures on the company's earnings.

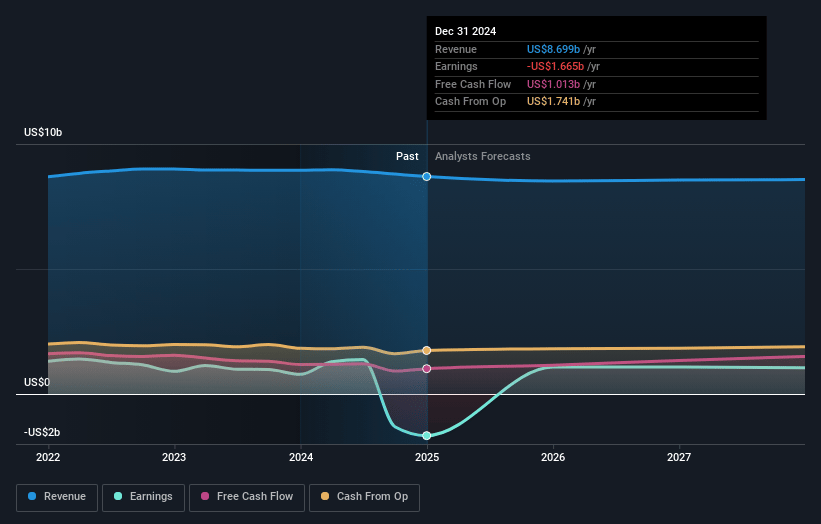

Sirius XM Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Sirius XM Holdings compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Sirius XM Holdings's revenue will decrease by 1.6% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from -19.1% today to 10.3% in 3 years time.

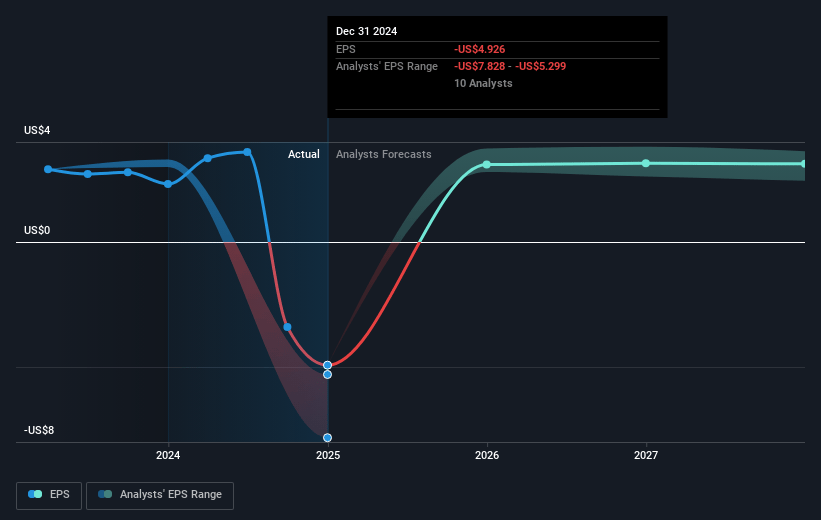

- The bearish analysts expect earnings to reach $856.1 million (and earnings per share of $2.37) by about April 2028, up from $-1.7 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 8.0x on those 2028 earnings, up from -4.1x today. This future PE is lower than the current PE for the US Media industry at 13.9x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.61%, as per the Simply Wall St company report.

Sirius XM Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- SiriusXM's strategic focus on robust margins and capital returns, reflected in their strong 60% gross margin for the year, may sustain a healthy net margin and enhance earnings.

- The company's continuous improvement in subscriber retention, driven by features like the three-year OEM subscription program and new automotive partnerships, could stabilize or even grow revenue.

- SiriusXM's expanding presence in electric vehicles, such as collaborations with Tesla and Rivian, may capture new market segments and bolster subscription revenue.

- The strategic development in digital and streaming capabilities, including a focus on podcasting and streaming platforms, supports an increase in advertising revenue that was robust at $1.8 billion in 2024.

- SiriusXM's efficiency initiatives, aiming for $200 million in annualized savings and cost optimization, have the potential to protect net margins and amplify free cash flow, targeting $1.15 billion in 2025.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Sirius XM Holdings is $19.68, which represents one standard deviation below the consensus price target of $24.1. This valuation is based on what can be assumed as the expectations of Sirius XM Holdings's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $32.0, and the most bearish reporting a price target of just $16.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $8.3 billion, earnings will come to $856.1 million, and it would be trading on a PE ratio of 8.0x, assuming you use a discount rate of 8.6%.

- Given the current share price of $20.3, the bearish analyst price target of $19.68 is 3.2% lower. The relatively low difference between the current share price and the analyst bearish price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is an employee of Simply Wall St, but has written this narrative in their capacity as an individual investor. AnalystLowTarget holds no position in NasdaqGS:SIRI. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimate's are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.