Narratives are currently in beta

Key Takeaways

- Acquisitions of iconic catalogs and artist deals could enhance long-term revenue through new releases and high-demand track synchronization.

- Investment in emerging markets like the Middle East and North Africa offers potential revenue growth amid US streaming saturation.

- Saturating U.S. subscriber growth and high acquisition costs may constrain future earnings, while volatile sync license revenue and declining net income indicate financial risks.

Catalysts

About Reservoir Media- Operates as a music publishing company.

- Reservoir Media's acquisition of iconic catalogs and deals with influential artists such as Snoop Dogg could enhance their long-term revenue streams due to potential for new music releases and increased synchronization revenue from high-demand tracks.

- The company's investment in emerging markets such as the Middle East and North Africa could open up significant organic growth opportunities, potentially impacting revenue positively given the saturation of US streaming subscriber growth.

- Their strategy of acquiring evergreen catalogs, which often have cyclical success (like holiday-specific tracks), could lead to a steady and predictable revenue increase, improving net margins over time.

- Reservoir Media's focus on identifying high ROI assets and maintaining a diversified portfolio across genres suggests an increase in long-term earnings potential, by stabilizing revenue streams against market shifts.

- Positive trends in music publishing, driven by investments in country and crossover hits enjoying popularity on platforms like TikTok, indicate future growth in revenue and market share in digital streaming, boosting overall earnings.

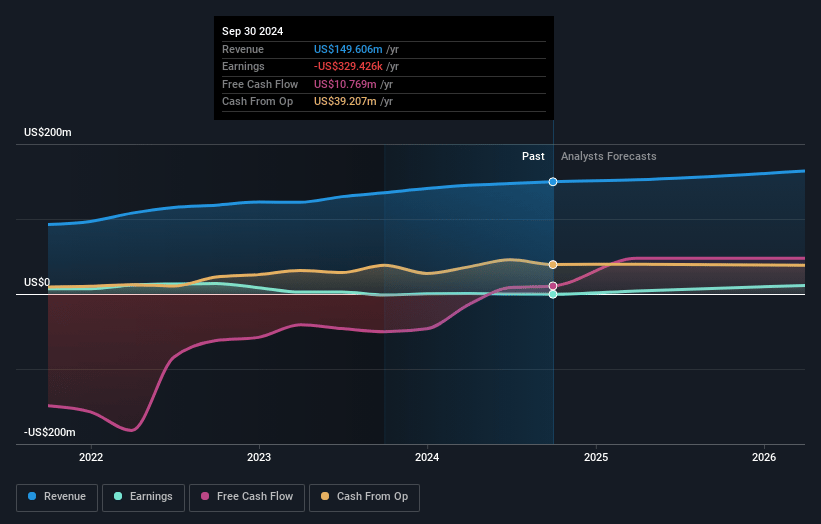

Reservoir Media Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Reservoir Media's revenue will grow by 5.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from -0.2% today to 26.7% in 3 years time.

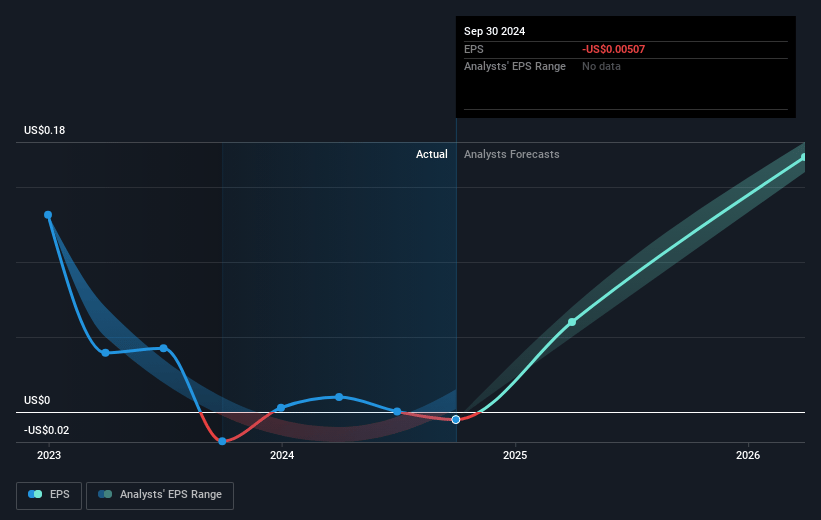

- Analysts expect earnings to reach $47.5 million (and earnings per share of $0.72) by about January 2028, up from $-329.4 thousand today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 24.3x on those 2028 earnings, up from -1603.7x today. This future PE is greater than the current PE for the US Entertainment industry at 19.6x.

- Analysts expect the number of shares outstanding to grow by 0.45% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.99%, as per the Simply Wall St company report.

Reservoir Media Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The number of paying subscribers in the U.S. is reaching a saturation point, potentially impacting future revenue growth from streaming as it becomes harder to gain new subscribers.

- The decrease in Recorded Music revenue by 1% due to previous releases reaching peak sales highlights challenges in sustaining high revenue from past successes, which could impact revenue stability.

- The timing of sync licenses can cause volatility in revenues, as the business relies heavily on unpredictable demand from media productions and advertising campaigns.

- Net income showed a decline to $200,000 from $700,000 year over year, impacted by losses in fair value swaps, which could indicate financial performance risk and affect net margins.

- High acquisition multiples in the publishing market, often in the high teens, may limit attractive investment opportunities and increase the risk of overpaying, potentially affecting future earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $13.5 for Reservoir Media based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $15.0, and the most bearish reporting a price target of just $12.5.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $177.7 million, earnings will come to $47.5 million, and it would be trading on a PE ratio of 24.3x, assuming you use a discount rate of 9.0%.

- Given the current share price of $8.1, the analyst's price target of $13.5 is 40.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives