Narratives are currently in beta

Key Takeaways

- The acquisition of SuperPlay is anticipated to boost Playtika's revenue potential through high-growth game integration and scaling.

- Focus on direct-to-consumer channels and efficient cost management could enhance margins and stabilize EBITDA growth.

- Heavy reliance on M&A for growth introduces execution risk, while declining revenues and rising marketing costs pressure net margins and affect future earnings.

Catalysts

About Playtika Holding- Develops mobile games in the United States, Europe, Middle East, Africa, Asia pacific, and internationally.

- The proposed acquisition of SuperPlay could significantly enhance Playtika's portfolio, bringing new high-growth titles and increasing revenue potential as SuperPlay's successful games are integrated and scaled. This is expected to positively impact future revenue growth.

- Playtika's disciplined financial strategy, using a mix of upfront payments and performance-based earnouts for acquisitions, aligns incentives and could lead to sustainable EBITDA growth. This structure supports future earnings growth while limiting downside risks.

- The strategic focus on enhancing the product and feature roadmap for established games like Slotomania, including integrating historic IP and modifying in-game experiences, aims to boost user engagement and monetization, which could improve future revenue and net margins.

- Continued investments in direct-to-consumer (DTC) channels, which already show percent increases year-over-year, should drive higher-margin revenues, thereby potentially improving net margins as the DTC revenue mix grows.

- Efficient cost management and strategic marketing investments targeting the highest ROI opportunities may stabilize EBITDA margins and enhance free cash flow, contributing to stronger net margins and earnings in the future.

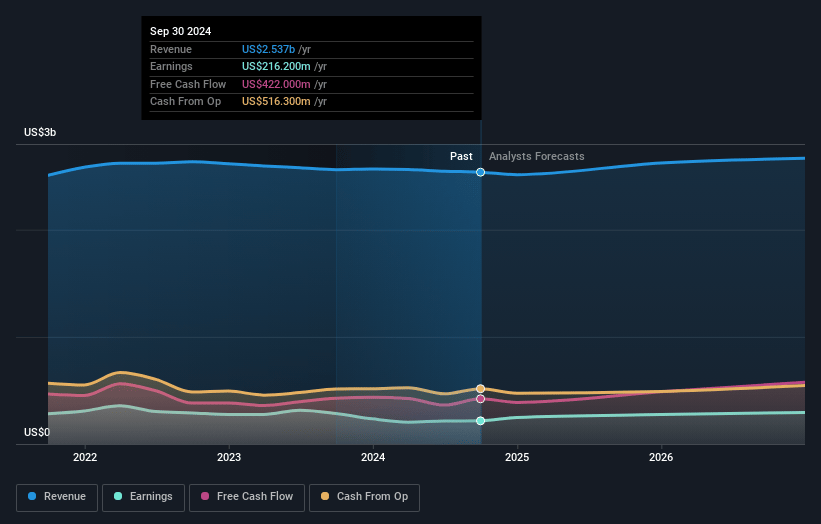

Playtika Holding Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Playtika Holding's revenue will grow by 3.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 8.5% today to 11.7% in 3 years time.

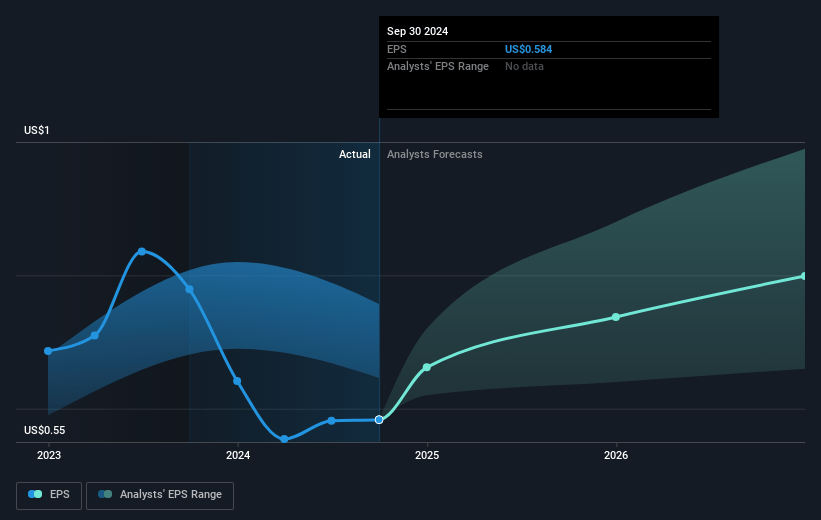

- Analysts expect earnings to reach $328.7 million (and earnings per share of $0.88) by about January 2028, up from $216.2 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 15.4x on those 2028 earnings, up from 12.6x today. This future PE is lower than the current PE for the US Entertainment industry at 19.0x.

- Analysts expect the number of shares outstanding to grow by 0.16% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.52%, as per the Simply Wall St company report.

Playtika Holding Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's revenue declined by 1% sequentially and 1.5% year-over-year, which could signal challenges in maintaining growth and impact future revenue projections.

- Slotomania, one of the key titles, did not meet expectations despite increased user acquisition spending, indicating potential challenges in driving significant user engagement and retention, affecting overall revenue.

- Average Daily Active Users (DAU) decreased by 6.2% sequentially and 9.5% year-over-year, reflecting potential difficulties in user acquisition and retention, which could impact revenue and long-term growth potential.

- There is a heavy reliance on M&A for growth, as demonstrated by the SuperPlay acquisition, which introduces execution risk and the potential for misalignment or unsuccessful integration, possibly affecting net margins and earnings.

- The decline in cost of revenue does not fully offset declining revenues, while increases in sales and marketing expenses may pressure net margins and earnings if these investments do not yield higher returns.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $9.73 for Playtika Holding based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $20.0, and the most bearish reporting a price target of just $7.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.8 billion, earnings will come to $328.7 million, and it would be trading on a PE ratio of 15.4x, assuming you use a discount rate of 11.5%.

- Given the current share price of $7.33, the analyst's price target of $9.73 is 24.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives