Key Takeaways

- Growth in Connected TV, strategic partnerships, and AI initiatives are key drivers for revenue and margin improvement moving forward.

- Investments in tech, agency marketplaces, and sports broadcasting aim to increase efficiency, expand audience reach, and create new revenue streams.

- The company's growth is threatened by demand volatility, execution risk, concentration risk, rising costs, and competitive technology investments impacting profitability and revenue streams.

Catalysts

About Magnite- Operates an independent omni-channel sell-side advertising platform in the United States and internationally.

- Magnite is experiencing significant growth in its Connected TV (CTV) segment, with CTV contribution ex-TAC (excluding traffic acquisition costs) increasing 23% year-over-year in Q4 2024, driven by partnerships with major streaming platforms like Netflix, Disney, and Roku. This is anticipated to positively impact revenue growth moving forward as these partnerships expand.

- The company plans to leverage AI initiatives, which include the development of tools that optimize ad targeting and yield management in their CTV and display businesses. By optimizing operations, this is expected to improve efficiency and net margins.

- Magnite's strategic investments in agency marketplaces and their ClearLine platform are projected to drive additional revenue streams by enhancing agency relationships and increasing client ad spend through these platforms.

- Their focus on technology improvements, such as reducing per-unit cloud costs and transitioning some operations on-premises, is expected to contribute to margin expansion and cost efficiency, positively affecting net earnings in the future.

- Magnite’s efforts to expand their footprint in live sports and international sports broadcasting, partnering with entities like Disney, NCAA, FIFA, and Sky New Zealand, are expected to broaden their audience reach and drive revenue growth.

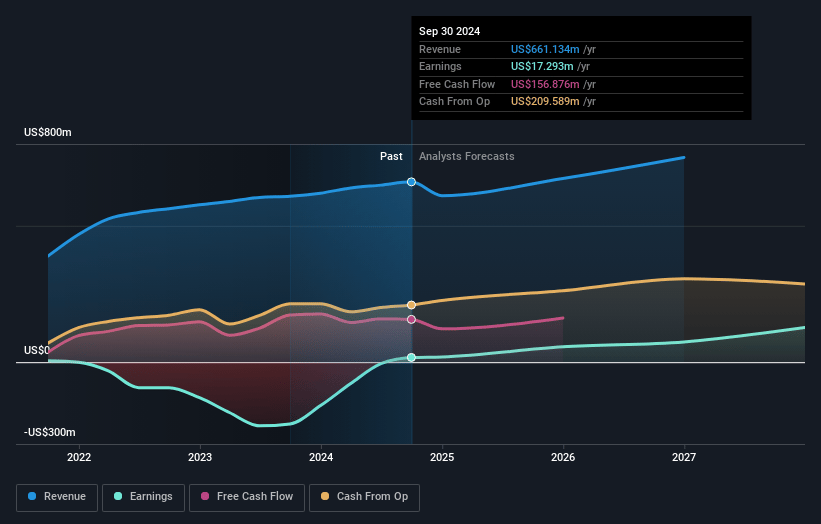

Magnite Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Magnite's revenue will grow by 9.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.4% today to 10.8% in 3 years time.

- Analysts expect earnings to reach $93.7 million (and earnings per share of $0.57) by about March 2028, up from $22.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 40.9x on those 2028 earnings, down from 79.7x today. This future PE is greater than the current PE for the US Media industry at 13.5x.

- Analysts expect the number of shares outstanding to grow by 2.09% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.91%, as per the Simply Wall St company report.

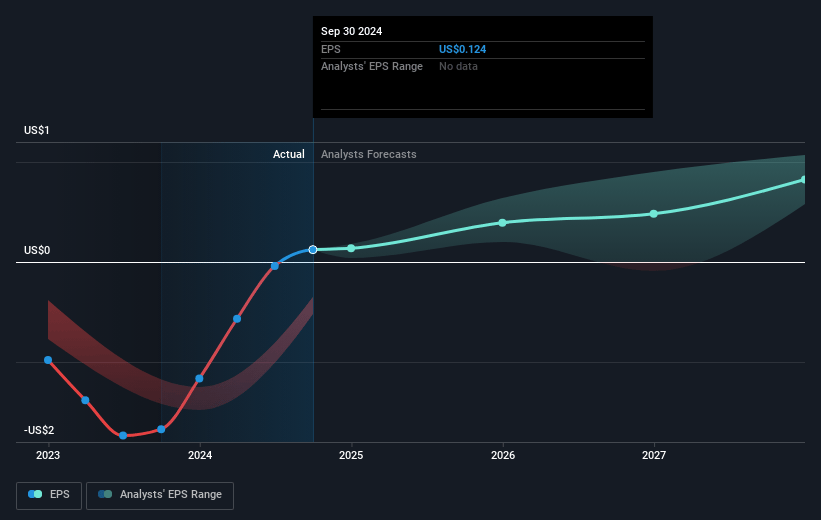

Magnite Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The drop in demand and CPMs in the DV+ business post-election in Q4 2024 resulted in only 1% growth, impacting overall quarterly results. This demand volatility presents a risk to future revenue stability.

- The internal transition to a hybrid cloud and on-prem model to manage costs is complex and carries execution risk, which could affect profitability and net margins if not managed efficiently.

- The partnership with OpenPath and its implications could lead to increased fees without a corresponding improvement in efficiency, potentially impacting net margins if publishers incur higher costs.

- The heavy reliance on key partners like Netflix and large streaming platforms for CTV momentum introduces concentration risk. Any disruptions or changes in these partnerships could affect revenue streams.

- The company's strategy to introduce generative AI and other new technologies involves upfront investment and competition risk with other players in the market, which could impact earnings if these initiatives do not yield expected returns.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $20.625 for Magnite based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $25.0, and the most bearish reporting a price target of just $15.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $866.1 million, earnings will come to $93.7 million, and it would be trading on a PE ratio of 40.9x, assuming you use a discount rate of 6.9%.

- Given the current share price of $12.7, the analyst price target of $20.62 is 38.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.