Key Takeaways

- Revenue pressure due to lower broadband growth and increased competition may hinder Charter's financial performance in core markets.

- High capital expenditures in network and rural expansion risk low returns if consumer uptake remains weak.

- Charter's network expansion, service improvements, and strategic bundling could drive revenue growth, improve margins, and enhance customer satisfaction, reducing churn and boosting earnings.

Catalysts

About Charter Communications- Operates as a broadband connectivity and cable operator company serving residential and commercial customers in the United States.

- Charter Communications faces revenue pressure from lower broadband subscriber growth as more consumers migrate to mobile-only or other lower-cost internet solutions, which could result in stagnant or declining revenues in core markets.

- The company’s ongoing investment in network expansion and customer service improvements may not yield proportional returns due to increasing competition, potentially compressing future net margins.

- Increases in capital expenditures, particularly those related to network evolution and rural expansion, may not translate into substantial earnings growth if consumer uptake in these areas remains below expectations.

- Slower growth in traditional video subscriptions compounded by the cost of integrating new content partnerships and digital offerings could further challenge overall revenue growth.

- The continued emphasis on promotional pricing strategies could lead to lower-than-expected average revenue per user (ARPU), impacting the company’s ability to boost earnings and achieve forecasted financial targets.

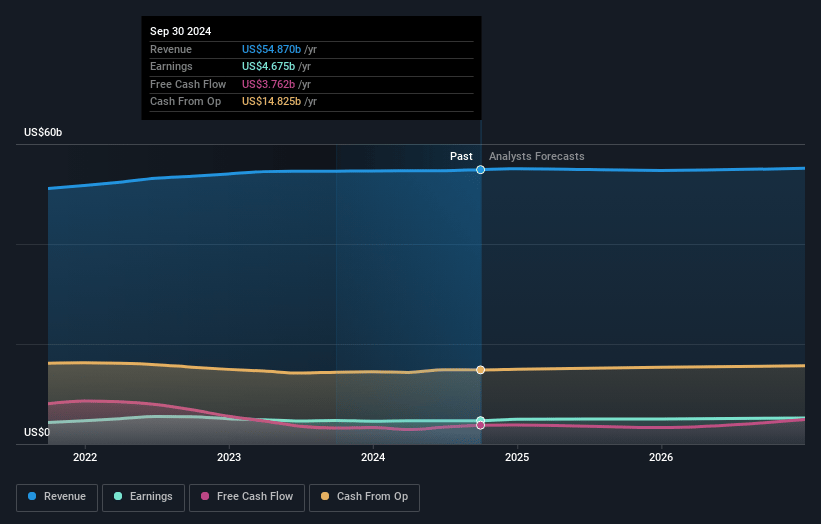

Charter Communications Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Charter Communications compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Charter Communications's revenue will decrease by 0.2% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 9.4% today to 7.3% in 3 years time.

- The bearish analysts expect earnings to reach $4.0 billion (and earnings per share of $36.17) by about July 2028, down from $5.2 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 14.9x on those 2028 earnings, up from 10.6x today. This future PE is lower than the current PE for the US Media industry at 20.2x.

- Analysts expect the number of shares outstanding to decline by 1.67% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.03%, as per the Simply Wall St company report.

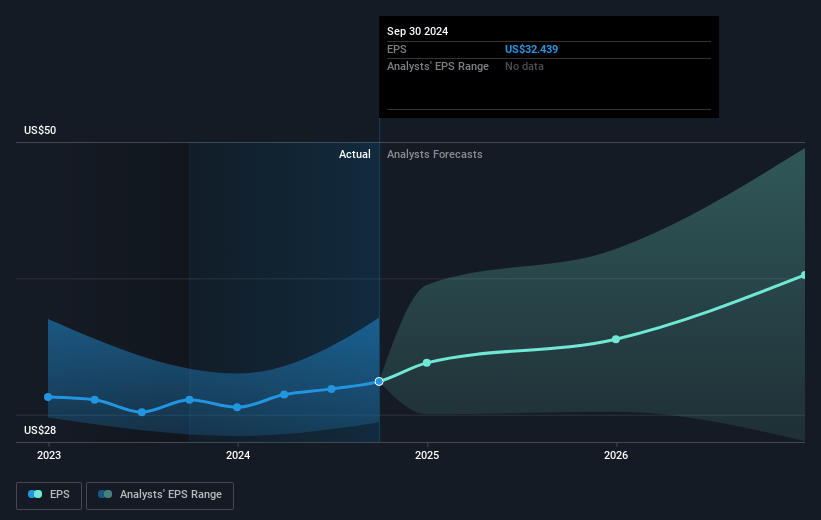

Charter Communications Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Charter's significant growth in Spectrum Mobile lines and broadening of its fiber network could lead to increased revenue and EBITDA growth if the trend continues.

- The convergence of Charter's network to handle growing data usage, alongside its investments in improving service quality and lowering costs, could maintain or improve net margins.

- The company’s expanding rural footprint and efforts in rebuilding and enhancing infrastructure, such as DOCSIS 4.0 upgrades, may positively impact future customer acquisition and revenue per home passed.

- Charter offers unmatched service by employing a fully U.S.-based workforce, along with investing in AI and machine learning to improve customer service efficiency, potentially driving higher customer satisfaction and reducing churn, impacting overall earnings.

- The strategic pricing and packaging approach, alongside the company's ability to bundle services such as mobile and video to present more value, might help increase customer acquisition and retention, potentially resulting in steady or growing net income.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Charter Communications is $315.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Charter Communications's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $600.0, and the most bearish reporting a price target of just $315.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $55.5 billion, earnings will come to $4.0 billion, and it would be trading on a PE ratio of 14.9x, assuming you use a discount rate of 9.0%.

- Given the current share price of $398.11, the bearish analyst price target of $315.0 is 26.4% lower.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.