Key Takeaways

- Elevated gold prices and strategic portfolio optimization position Newmont for stronger revenue, improved efficiency, and enhanced long-term profitability.

- Advancements in key projects, responsible mining practices, and capital returns strengthen Newmont's competitive advantage and shareholder value.

- Heightened concentration, rising costs, regulatory challenges, and reliance on strong gold prices threaten Newmont's margin stability, cash flow, and long-term production certainty.

Catalysts

About Newmont- Engages in the production and exploration of gold properties.

- The company is poised to benefit from ongoing global economic volatility and elevated inflation, which have driven gold prices to near-record highs; this environment is likely to persist and support stronger revenue growth and higher realized margins for Newmont.

- Newmont's robust execution of its portfolio optimization-completing the divestment of non-core assets for $3.2 billion in after-tax proceeds-sharpens its focus on high-margin, long-life Tier 1 assets, setting the stage for improved operational efficiency and sustained increases to both free cash flow and net earnings.

- The ramp-up and expansion of key projects (Ahafo North, Tanami, Cadia, and future development at Red Chris), alongside ongoing automation and technology adoption, are expected to drive higher production volumes and lower unit costs, positively impacting future revenue and margin expansion.

- Increasing investor and regulatory preference for strong ESG credentials favors Newmont, which maintains a competitive advantage in responsible mining, enabling greater access to capital and premium pricing for sustainably sourced gold, supporting valuation multiples and long-term earnings.

- Accelerated capital returns through share buybacks, underpinned by record free cash flow and a strong balance sheet, are likely to boost earnings per share and support shareholder value, reinforcing Newmont's long-term total return potential.

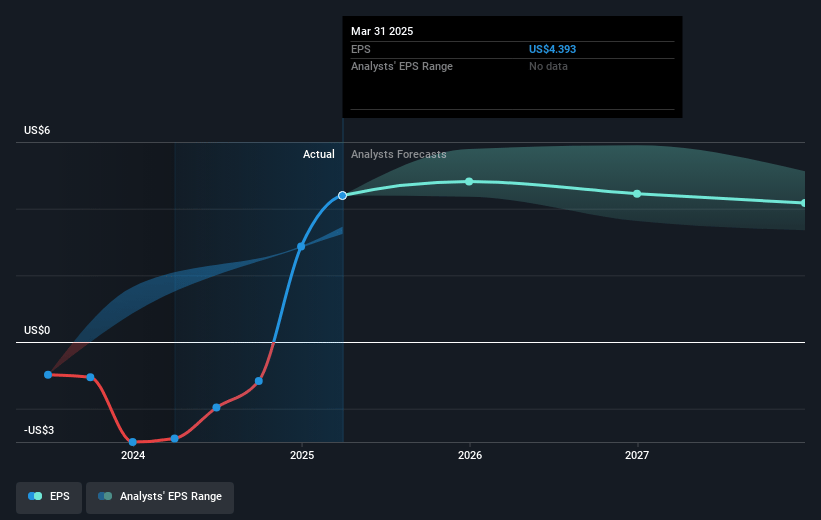

Newmont Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Newmont's revenue will grow by 1.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 25.4% today to 26.7% in 3 years time.

- Analysts expect earnings to reach $5.5 billion (and earnings per share of $5.28) by about July 2028, up from $5.0 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $7.8 billion in earnings, and the most bearish expecting $3.1 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 15.2x on those 2028 earnings, up from 12.6x today. This future PE is lower than the current PE for the US Metals and Mining industry at 22.1x.

- Analysts expect the number of shares outstanding to decline by 3.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.24%, as per the Simply Wall St company report.

Newmont Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Newmont is increasingly reliant on a smaller, more concentrated portfolio after divestitures, which may expose the company to heightened operational or geopolitical risks at individual mines and jurisdictions-potentially increasing revenue volatility and threatening long-term production stability.

- The company faces significant capital expenditure requirements in the next several years due to ongoing mine expansions, tailings remediation, and development of new projects (e.g., Ahafo North, Tanami Expansion, Cadia block caves), which could constrain free cash flow and earnings, especially if project execution risks or cost overruns materialize.

- Lower-grade ore processing at key assets such as Cadia and Lihir over the next few years, as explicitly acknowledged, will likely result in higher per-ounce extraction costs and possible margin compression, which could negatively impact net margins and profitability if gold prices retrace from current highs.

- Intensifying regulatory scrutiny-including environmental (tailings management, water treatment) and government negotiations (royalties, mineral development contracts at Wafi-Golpu)-presents risks for rising compliance and operating costs, delays in project approvals, and uncertainty over tax/regulatory regimes, all of which could affect future earnings and return on capital.

- Elevated free cash flow and shareholder returns are currently buoyed by high gold prices, but any sustained decline in gold demand due to increased competition from digital assets or synthetic gold, or a downturn in macroeconomic drivers, would undermined Newmont's revenues and could put dividend and buyback programs at risk.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $67.224 for Newmont based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $88.59, and the most bearish reporting a price target of just $56.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $20.5 billion, earnings will come to $5.5 billion, and it would be trading on a PE ratio of 15.2x, assuming you use a discount rate of 7.2%.

- Given the current share price of $57.35, the analyst price target of $67.22 is 14.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.