Narratives are currently in beta

Key Takeaways

- Extreme weather events and reliance on favorable conditions could impact shipment volumes and revenue stability.

- Acquisitions and infrastructure spending may enhance growth, but integration challenges and sector delays risk impacting profits and earnings.

- Strategic acquisitions, infrastructure spending benefits, and a robust balance sheet position Martin Marietta for long-term revenue growth and earnings stability despite disruptions.

Catalysts

About Martin Marietta Materials- A natural resource-based building materials company, supplies aggregates and heavy-side building materials to the construction industry in the United States and internationally.

- Extreme weather events in 2024, including hurricanes and significant precipitation, have led to project delays and inefficiencies, impacting shipment volumes. This disruption could affect future revenue recovery if adverse weather patterns persist.

- Despite a decrease in shipments, the company plans to expand aggregate shipments by low single digits and increase aggregate pricing by mid to high single digits in 2025. However, over-reliance on favorable weather conditions for recovery might influence revenue stability.

- Recent acquisitions of aggregate assets in South Florida and Southern California are expected to enhance future gross profit contribution. Still, the successful integration and realization of profit growth potential remain uncertain and might impact net margins if not achieved.

- Enhanced federal and state infrastructure spending through the IIJA is expected to support long-term volume stability. Nonetheless, if funding and project execution are slower than anticipated, revenue growth projections for the public sector might fall short.

- Improvements in private sectors such as warehousing and artificial intelligence-related construction are anticipated to support aggregates demand. Any potential delay or downturn in these sectors could adversely affect earnings growth.

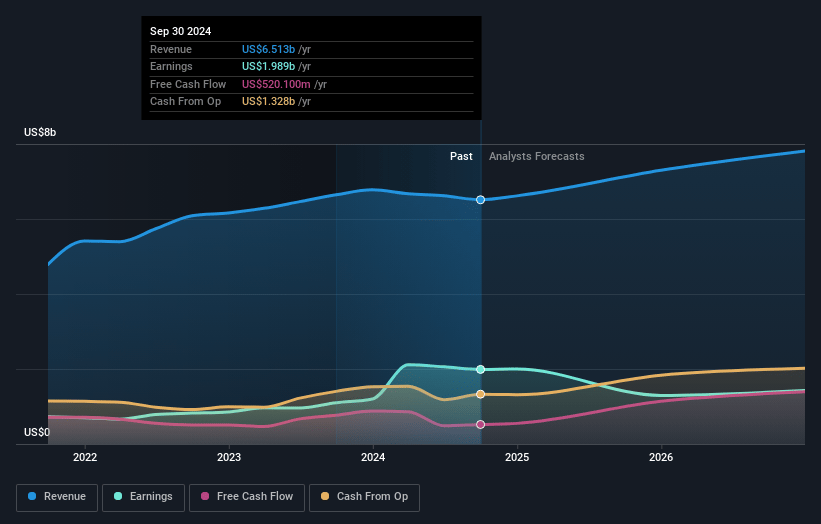

Martin Marietta Materials Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Martin Marietta Materials's revenue will grow by 7.7% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 30.5% today to 18.4% in 3 years time.

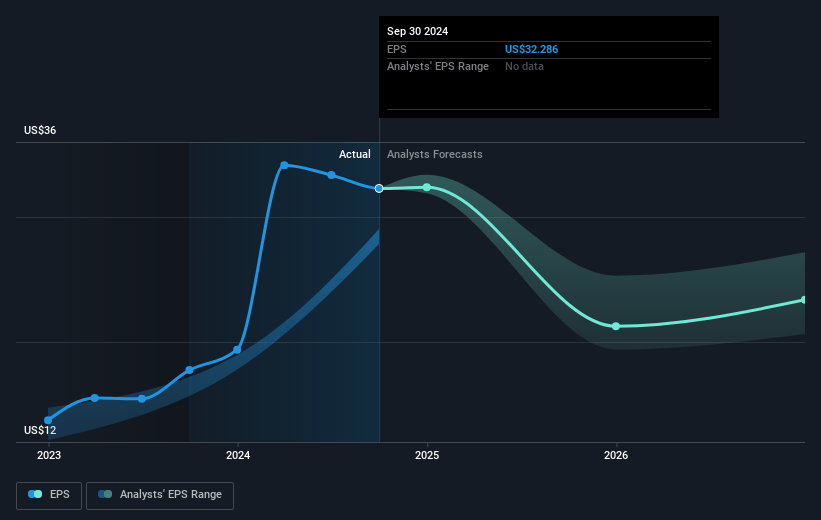

- Analysts expect earnings to reach $1.5 billion (and earnings per share of $24.77) by about December 2027, down from $2.0 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $1.3 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 31.7x on those 2027 earnings, up from 17.2x today. This future PE is greater than the current PE for the US Basic Materials industry at 26.1x.

- Analysts expect the number of shares outstanding to decline by 0.43% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.91%, as per the Simply Wall St company report.

Martin Marietta Materials Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Despite weather-related disruptions, Martin Marietta reported record third-quarter cash flows from operations and expects future shipments and profitability to improve as planned deliveries rebound following weather delays, which could bolster future revenues and earnings.

- The company has expanded its aggregates presence through strategic acquisitions in South Florida and Southern California, targeting regions with significant reserve shortages, which could contribute positively to revenue growth and profitability in the long term.

- Martin Marietta anticipates benefits from increased infrastructure spending through the Infrastructure Investment and Jobs Act, supporting a stable demand environment and pricing power, which could enhance long-term revenue and earnings.

- The company is positioned to capitalize on growth in infrastructure related to artificial intelligence and warehouse construction, particularly in strategic markets like Dallas-Fort Worth, which may present opportunities for future revenue growth.

- Martin Marietta maintains a robust balance sheet and sound capital allocation strategies, including a steady dividend growth, which may sustain investor confidence and support earnings stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $646.12 for Martin Marietta Materials based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $730.0, and the most bearish reporting a price target of just $370.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $8.1 billion, earnings will come to $1.5 billion, and it would be trading on a PE ratio of 31.7x, assuming you use a discount rate of 6.9%.

- Given the current share price of $560.18, the analyst's price target of $646.12 is 13.3% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives