Narratives are currently in beta

Key Takeaways

- Strategic focus on advanced recycling and circular polymers enhances production capabilities and capitalizes on rising demand, boosting future revenues and net margins.

- Exit from low-margin refining and balanced capital allocation prioritize high-growth investments, aiming for significant earnings growth and improved financial performance.

- Strategic shifts and market challenges could pressure revenue and margins through refinery shutdowns, price fluctuations, and execution risks in transformations.

Catalysts

About LyondellBasell Industries- Operates as a chemical company in the United States, Germany, Mexico, Italy, Poland, France, Japan, China, the Netherlands, and internationally.

- The construction of the MoReTec-1 facility in Wesseling, Germany, utilizing proprietary catalytic advanced recycling technology, is anticipated to drive future growth by increasing LyondellBasell's production capacity of high-value circular polymers. This is likely to impact future revenues positively as demand for circular and low-carbon solutions rises.

- Plans for MoReTec-2 at the Houston site, following the refinery closure, aim to expand capacity for producing low carbon CirculenRevive and CirculenRenew polymers. This strategic shift is expected to improve net margins by leveraging low-cost opportunities in recycled and renewable feedstocks.

- The exit from the low-margin Refining segment by 2025 focuses resources on high-growth areas, potentially improving net margins and enhancing sustainable earnings as resources are redirected to more profitable sectors.

- Stimulus measures in China and lower global interest rates pose potential macroeconomic tailwinds, offering upside for future cash generation, which could positively impact future earnings as macroeconomic conditions improve.

- The company's commitment to balanced capital allocation, including a focus on high-return investments aimed at unlocking $1 billion in recurring annual EBITDA by 2025, suggests a substantial impact on earnings growth and financial performance.

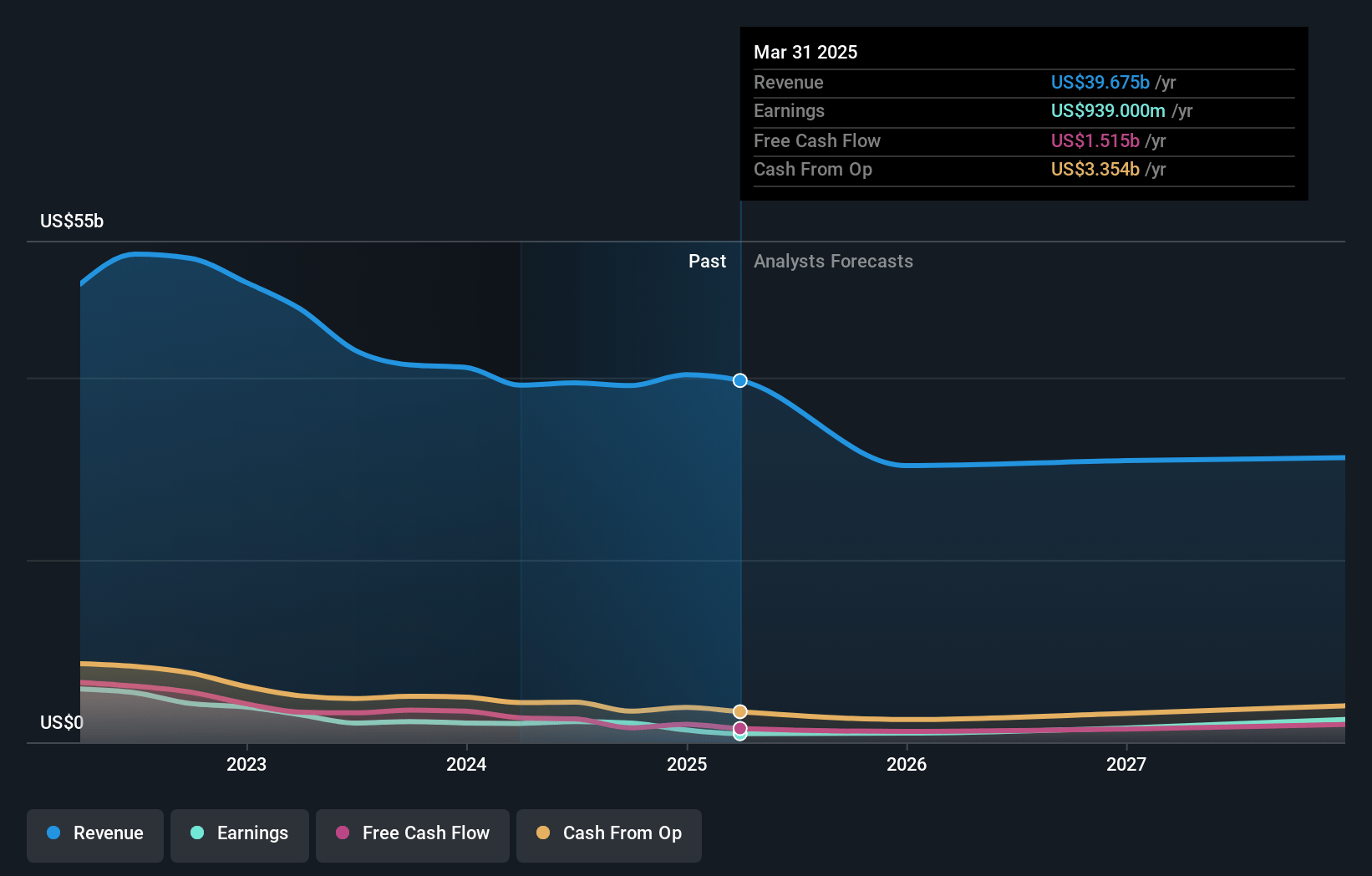

LyondellBasell Industries Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming LyondellBasell Industries's revenue will decrease by -6.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.3% today to 8.7% in 3 years time.

- Analysts expect earnings to reach $2.9 billion (and earnings per share of $8.84) by about November 2027, up from $2.1 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $3.8 billion in earnings, and the most bearish expecting $2.2 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 14.2x on those 2027 earnings, up from 12.9x today. This future PE is lower than the current PE for the US Chemicals industry at 25.5x.

- Analysts expect the number of shares outstanding to decline by 0.1% per year for the next 3 years.

- To value all of this in today's dollars, we will use a discount rate of 7.29%, as per the Simply Wall St company report.

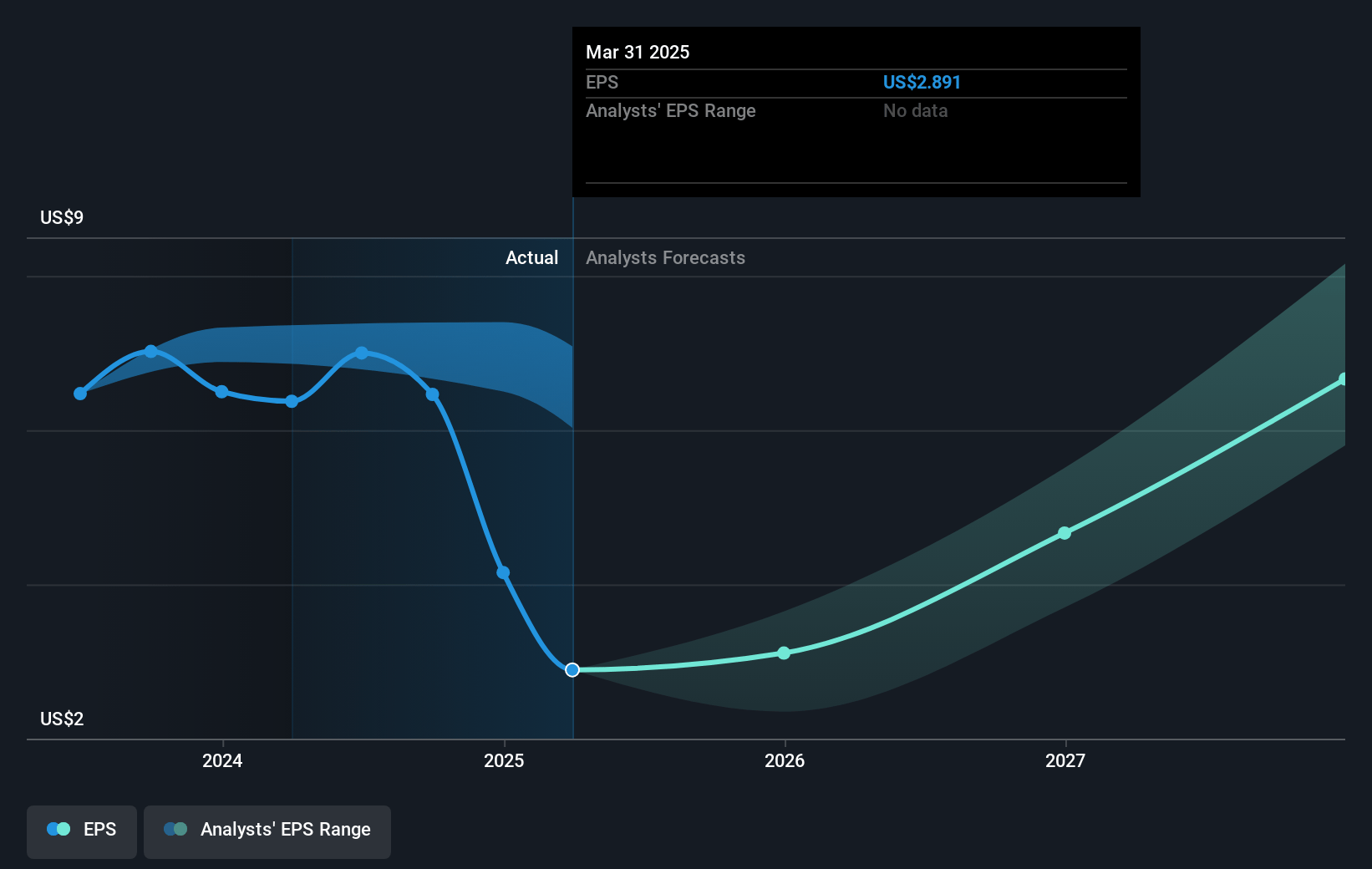

LyondellBasell Industries Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The sharp decline in gasoline crack spreads has negatively impacted LyondellBasell’s refining and oxyfuels businesses, potentially reducing revenue and EBITDA if the trend continues.

- Planned refinery shutdown by the first quarter of 2025 will lead to short-term earnings adjustment and ongoing costs, potentially impacting the company’s net margins as part of discontinued operations.

- Seasonal demand trends and increased ethane and natural gas prices are likely to pressure integrated polyethylene margins in the near term, which can affect revenue and overall earnings.

- The European olefins and polyolefins segment is operating at lower rates amidst macroeconomic instability and asset review, creating potential headwinds for revenue generation and segment profitability.

- Significant strategic transformations, including divestments and new technology investments, carry execution risks that could affect long-term revenue growth and future net margins if not managed effectively.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $101.51 for LyondellBasell Industries based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $118.21, and the most bearish reporting a price target of just $85.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $33.0 billion, earnings will come to $2.9 billion, and it would be trading on a PE ratio of 14.2x, assuming you use a discount rate of 7.3%.

- Given the current share price of $85.37, the analyst's price target of $101.51 is 15.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives