Key Takeaways

- Focus on high-growth segments and strategic divestitures is expected to enhance revenue and profitability in core operations.

- Strategic expansions and investments in new technologies and geographies are aimed at improving margins and supporting long-term revenue growth.

- Macroeconomic challenges and weakened automotive demand threaten Element Solutions' revenue and margins, requiring strategic management to mitigate industrial sector risks.

Catalysts

About Element Solutions- Operates as a specialty chemicals company in the United States, China, and internationally.

- Element Solutions' focus on the highest value, fastest-growing segments of the electronic supply chain, such as advanced packaging in semiconductors and power electronics for electric vehicles, is expected to drive revenue growth.

- The divestiture of the Graphic Solutions business, which is not aligned with ESI's core operations, is projected to be accretive to both margins and return on capital, enhancing future profitability and earnings.

- Strategic capacity expansions and investments in application development in growth geographies such as Southeast and subcontinental Asia could support long-term revenue and margin improvements.

- Ongoing procurement optimization, facility rationalization, and pricing actions are expected to improve margins and drive earnings growth, even in softer industrial markets, positioning the company for better financial performance when demand rebounds.

- Increased investments in new technologies such as advanced packaging and nanocopper, along with the development of new applications, align with growth opportunities, suggesting potential revenue and earnings expansion as these investments mature.

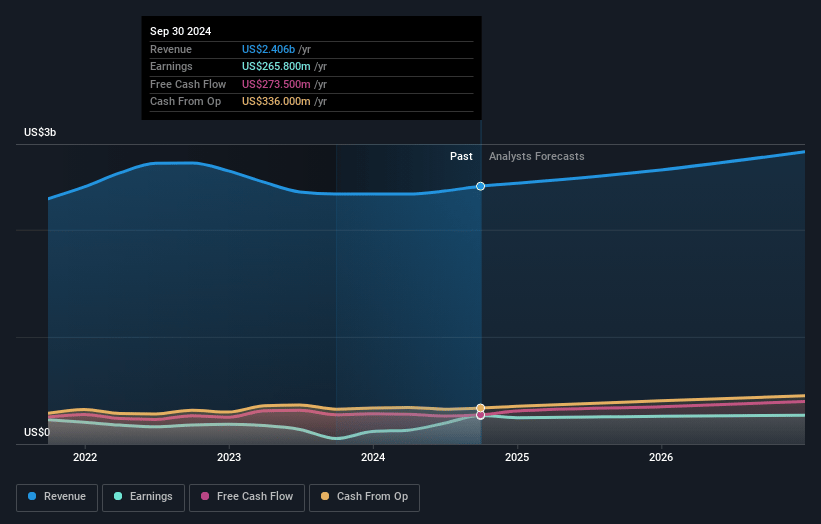

Element Solutions Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Element Solutions's revenue will grow by 3.1% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 11.0% today to 10.7% in 3 years time.

- Analysts expect earnings to reach $282.9 million (and earnings per share of $1.13) by about January 2028, up from $265.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 33.6x on those 2028 earnings, up from 23.2x today. This future PE is greater than the current PE for the US Chemicals industry at 22.6x.

- Analysts expect the number of shares outstanding to grow by 1.2% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.1%, as per the Simply Wall St company report.

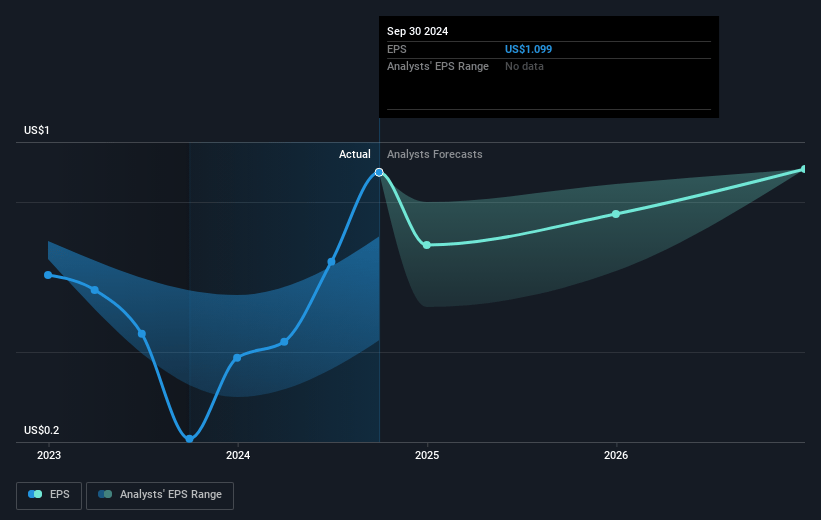

Element Solutions Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The softening demand in Europe and lower revenue from metal price surcharges in the company's core industrial portfolio have been identified as headwinds, which could negatively impact future revenues and net margins.

- The electronics segment, while experiencing standout volume growth, is still facing challenges in certain parts, like smartphones and industrial applications, which did not accelerate as expected. This could affect revenue and earnings if these areas do not recover.

- The divestiture of the Graphic Solutions business, though financially strategic, may introduce a short-term reduction in revenue until the capital is redeployed effectively.

- There is macroeconomic uncertainty, as broader industrial end markets are weaker than expected and the impact of potential interest rate cuts or Chinese stimulus is unclear, potentially affecting overall market conditions and impacting future earnings.

- Automotive demand has weakened, which, along with reductions in surcharges for commodity metals, impacted segments reliant on those markets, posing risk to revenue and margin stability in the industrial sector.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $30.95 for Element Solutions based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $2.6 billion, earnings will come to $282.9 million, and it would be trading on a PE ratio of 33.6x, assuming you use a discount rate of 7.1%.

- Given the current share price of $25.41, the analyst's price target of $30.95 is 17.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives